For those who may have been off mountain climbing in the Grand Tetons, the long-awaited Jackson Hole[i] Economic Symposium, sponsored by the Federal Reserve Bank of Kansas City, kicks off today. Coming near the end of summer, it usually becomes a focus for investors during a slow news cycle. This year, however, it is consequential not only because of timing, but also because markets are craving a crucial dose of clarity from the Federal Reserve – particularly from its Chair, Jerome Powell.

The conference is meant to be an economic confab. The official them of this year’s gathering is “Reassessing Constraints on the Economy and Policy,” and while I have no doubt that there will be a wealth of worthy research on that on that important economic topic, the KC Fed’s press release knows not to bury the lead: “On Friday, Aug. 26 at 9 a.m. CT, Federal Reserve Chairman Jerome Powell’s remarks will be streamed on the Kansas City Fed’s YouTube channel, youtube.com/kansascityfed.” The media assemblage is not in Wyoming to hear a series of economic presentations. If that were the case, there must be scores of other conferences for them to cover. No, they are here hoping for a small dose of monetary clarity from the Fed Chair.

I have often referred to Chair Powell as “Goldilocks in a Suit.” The Goldilocks reference may be even more apt when he is a delivering a key speech in an area known to have a significant bear population. While the local tourism website warns about the massive, furry kind, many more are hunched around computers worldwide, wondering if the Chairman’s speech will allow them to pounce or send them back into hibernation.

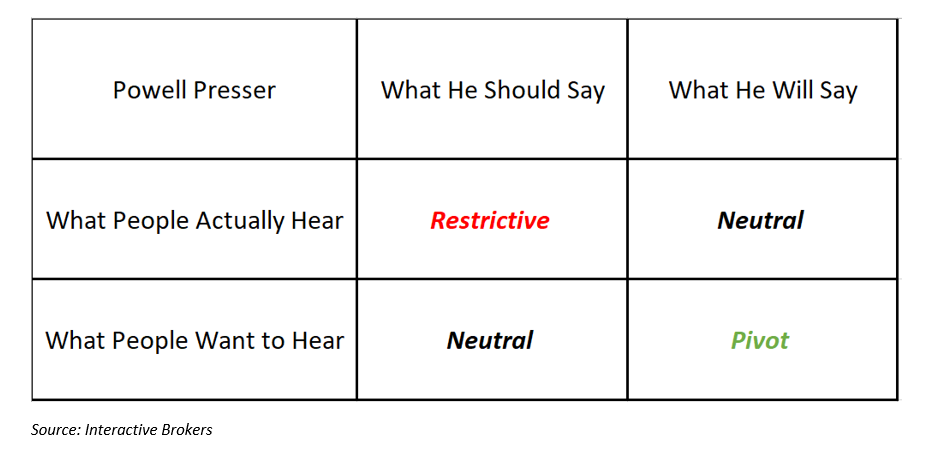

The problem with predictively analyzing any of Powell’s public addresses is that either he has a way of saying things that people want to hear, or that listeners have a knack of hearing what they want, no matter what he says. During the last post-FOMC press conference, bullish investors seized upon Powell’s assertion that monetary policy was currently at a neutral level of monetary policy. Never mind that his answer to the same question continued with an acknowledgement that further tightening was required, nor did it matter at first that a steady parade of Fed talking heads pushed back on that notion almost immediately. We questioned whether it was selective hearing on the market’s part, or a clever game of “good cop, bad cop” by the Fed.

Thus, I look at the range of probable outcomes for tomorrow to be structured this way:

If the parade of economists interviewed in the media are any indication, Chair Powell should come out forcefully with a discussion about further rate hikes and quantitative tightening. Markets seem to be pricing in a cessation of rate hikes and a potential cut down the road. From whom did they get idea, pray tell? It is also entirely possible that he gives a sobering speech but with enough thin reeds for the hopeful to cling to. We saw that just a month ago, which is why my simplistic hunches for what people want to hear is consistently more optimistic than what is actually said.

Before this morning’s bounce I was ready to assert that a dour response was already priced into both the stock and bond markets. Now I am less certain about the former. If traders interpret the speech as conciliatory we can see another Friday when traders feast on at-money and just out-of-the-money expiring calls in SPY. If they interpret the speech in a negative manner, the 100-day moving average for SPX at 4,057 could come into play.

Grab some popcorn, or maybe a pot of honey, and listen closely to tomorrow’s speech.

—

[i] A quick aside – why are these hugely important economic conferences held at ritzy ski resorts (Davos, Jackson Hole)? For example, I can’t imagine that the facilities used by Berkshire Hathaway are booked solid. Omaha is also in the KC Fed’s district.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. Multiple leg strategies, including spreads, will incur multiple commission charges. For more information read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD) or visit ibkr.com/occ