Throughout the course of the current Federal Reserve rate hike cycle, and the attendant increase in the U.S. Treasury (UST) 10-Year yield, I periodically get asked whether it is time to go long on duration. My answer has been a very consistent one: I’d rather be late than early to the duration party. With the UST 10-Year yield once again passing the 4% threshold, I thought it would be a good idea to revisit this topic. And, alas, my answer still hasn’t changed.

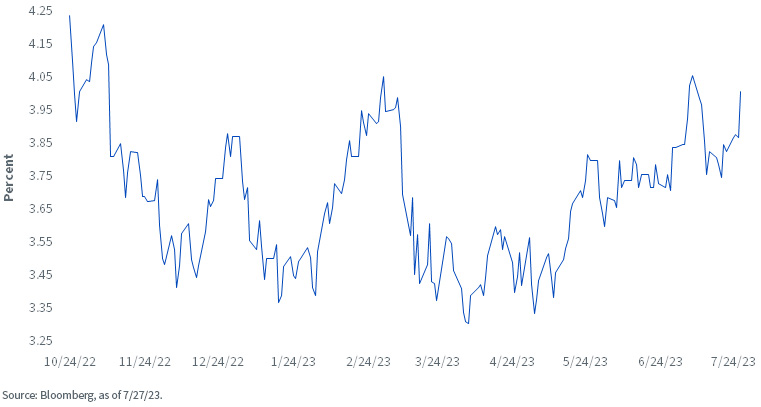

U.S. Treasury 10-Year Yield

In answering the duration question, I think it is useful to show the pattern of the UST 10-Year yield since it hit its most recent peak of roughly 4.25% (4.33% in intra-day trading) in October of last year. Yes, after reaching this high-water mark in the fall, the 10-Year yield did decline in a rather startling fashion, falling by 80 basis points (bps) to a little over 3.40% in December. However, just as quickly, this decline was reversed and another upward move occurred heading into the year-end. In fact, if you look closely at the enclosed graph, it becomes clear how this “up and down, then up again” trend has played out over the last nine months.

The most recent episode occurred beginning in early March. As the reader will recall, Fed Chairman Powell gave rather hawkish testimony to Congress in early March and yields all along the Treasury yield curve rose considerably as a result. In fact, the UST 2-Year yield rose above 5% and the 10-Year yield eclipsed the 4% mark yet again. Then the regional bank turmoil hit, and all bets were off as UST yields plummeted. In fact, the 10-Year ultimately fell to 3.31% in early April, another sizeable decline of 70 bps.

However, let’s fast-forward to the present, where that 70-bps plunge in yield has once again been completely reversed. Indeed, as of this writing, the UST 10-Year yield has retraced all the way back over 4% one more time, posting a 4.01% reading.

Conclusion

With the Fed in “higher for longer” mode, a reasonable outcome for the 10-Year could be to remain in a range-bound pattern, with the yield skewed toward the upper limit. In fact, another run at the aforementioned high point of 4.25% should not be ruled out either. This type of trading pattern would not be conducive to going long on duration in a bond portfolio.

In addition, the historical inversion of the Treasury yield curve offers no incentive, or urgency, to take on such positioning. Against this backdrop, investors should consider Treasury floating rate notes, which provide income without the volatility that has been witnessed in the 10-Year sector.

—

Originally Posted August 2, 2023 – Still Want to Be Late to the Duration Party?

Important Risks Related to this ArticleThere are risks associated with investing, including the possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Disclosure: WisdomTree U.S.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Funds before investing. U.S. investors only: To obtain a prospectus containing this and other important information, please call 866.909.WISE (9473) or click here to view or download a prospectus online. Read the prospectus carefully before you invest. There are risks involved with investing, including the possible loss of principal. Past performance does not guarantee future results.

You cannot invest directly in an index.

Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, real estate, currency, fixed income and alternative investments include additional risks. Due to the investment strategy of certain Funds, they may make higher capital gain distributions than other ETFs. Please see prospectus for discussion of risks.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

Interactive Advisors offers two portfolios powered by WisdomTree: the WisdomTree Aggressive and WisdomTree Moderately Aggressive with Alts portfolios.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree U.S. and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree U.S. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.