By: Dr. Martin Kuehle, Cedric Spiegel

Why the Asian convertible bond market could offer investors a chance to build up exposure to one of the world’s fastest growing regions.

As the era of ultra-low interest rates ends, equity-linked financing is becoming more attractive for companies facing higher borrowing costs. For companies looking for cheaper funding tools, convertible bonds are an increasingly popular option.

The traditional relationship between bond prices and bond yields of convertible bonds offers opportunities for investors looking for a steady income with an option of benefitting if stock prices rally.

The hybrid nature of convertible bonds makes them unique as they combine features of both debt and equity. They are issued by companies and offer investors the option to convert the bond into a predetermined number of shares of the issuer’s common stock. Although convertible bonds typically offer a lower nominal yield, or a coupon rate, than traditional bonds, they provide investors with the potential for capital growth if the issuer’s stock price rises.

Asian convertible bonds are particularly popular among investors wanting to participate in China’s economic reopening without having to take on unwarranted risk in the volatile equity markets. And rightfully so. In fact, the average downside participation in Asian convertible bonds has been well under 50%. In other words, Asian convertible bonds have protected investors from more than half of the equity market losses.

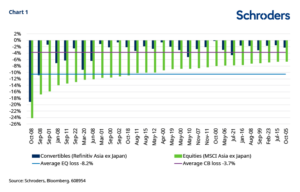

CHART 1: Worst MSCI Asia ex Japan (and Hang Seng) month compared to Refinitv Asia ex Japan

The chart above, which looks at the worst performing month of the MSCI Asia ex Japan stock index, shows that convertibles have performed better due to their in-built stabilisers. This not only shows that downside protection does work, but also presents a reasonable idea for the scale of protection. On average, convertibles show a loss of -3.7% compared to -8.2% for equities.

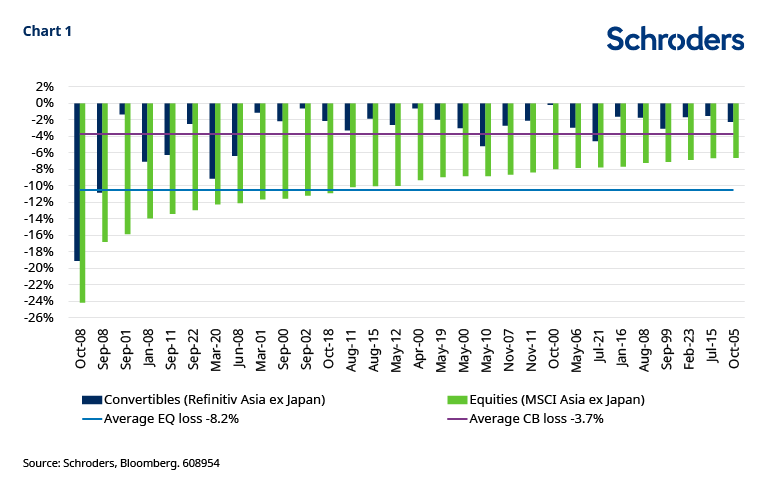

Convertible bonds are particularly attractive in volatile markets, as they can provide investors with exposure to the potential upside of an issuer’s stock price while limiting their downside risk. Additionally, convertible bonds can provide diversification benefits for investors, granting access to a range of different issuers and industries. The effective downside protection and significant upside participation can result in a much smoother performance. Over the past decade, investors have been able to generate equity-like performance with Asian convertible bonds.

CHART 2: Asian convertibles vs equities

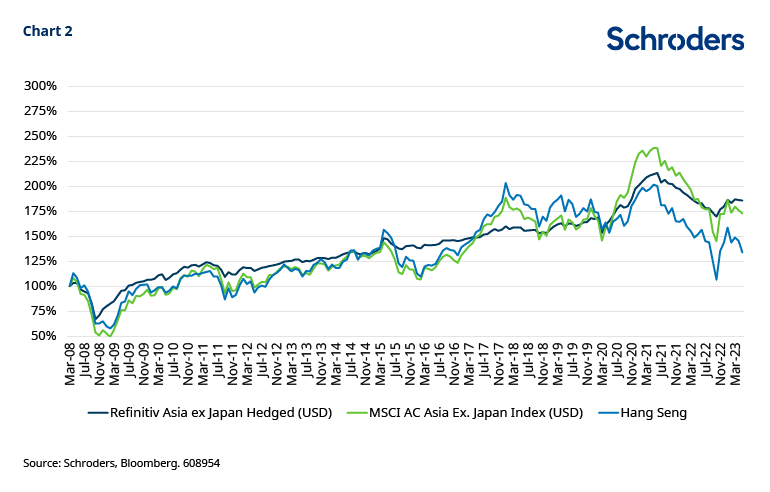

But why choose Asian convertibles now? The region’s convertible bonds offer attractive valuations compared to other markets, particularly bonds from the US and Europe. This reflects the fact that Asian convertible bonds are still underrepresented in global portfolios.

Chart 3: Current convertible valuations

From a macroeconomic point of view, Asia is home to some of the world’s fastest-growing economies, including China. These economies are expected to continue expanding at a rapid pace, driven by factors such as a larger middle class, urbanisation, and government policies aimed at supporting economic growth. This presents opportunities for companies serving this market, home to some of the world’s most innovative companies particularly in the technology sector. These companies are driving growth and disruption in industries ranging from e-commerce to fintech. As a refinancing tool for growth companies, convertibles could benefit from this trend.

But there is also much more to Asia than just China, which may have lost its low-cost comparative advantage. This sets the stage for Southeast Asia and India to become the region’s new high-flying economies, unlocking their full growth potential. Trade between North and South Asia has substantially risen over the past two decades, with a marked acceleration in the last two years led by China. India and Southeast Asia are well positioned to attract increased trade and investment from North Asia and the rest of the world, with an increasing geopolitical push from multinational companies diversifying their global value chains away from China.

This shift in supply chains, due to rising labour costs in China, has accelerated because of the US-China trade tensions and the Covid-19 pandemic, with Asian economies being the largest beneficiaries. Foreign investment flows and export market share suggest a gradual shift, with Vietnam, Taiwan, India, and Malaysia as the biggest gainers.

The full impact of rising foreign investments, new production facilities and a rise in export market shares is likely to materialise over the next three to five years. India and the Association of Southeast Asian Nations (ASEAN) are likely to benefit the most, with all ASEAN economies ranked within the top 10 in the Towards a Foreign Direct Investment (FDI) attractiveness scorecard. Greater supply chain diversification should be positive for India and ASEAN nations via the trade channel, promoting more economic integration and lower non-tariff barriers.

In addition, when it comes to the energy transition there are a lot of opportunities emerging in China as the country’s car manufacturing capability lags major industrialised countries due to historical reasons. This had led to China focusing on electric vehicle manufacturing, which does not require sophisticated mechanical engineering. National security reasons also play a role, as China’s high crude oil import dependence poses potential security concerns.

China is also a global leader in renewable energy technologies, with Neighbourhood EVs (NEVs) making up 27.5% of the total auto production. NEVs are electric vehicles which have a top speed of 25 to 35 mph. China delivers much cheaper electricity, resulting in an average 85% discount for NEV consumers on charging costs compared to traditional internal combustion engine cars. The government’s policies to incentivise charging station infrastructure installations have contributed to the rapid growth of the country’s NEV market.

This offers opportunities for convertible bond investors. With electronic vehicles and battery providers already on the convertible bond market, there could be easy access for capital in this sector. Battery growth installations were soft at 28% in Q1 2023, compared to the same period a year earlier. However, battery makers are slightly more confident about utilisation rates in Q2 2023. Potential supportive policies and alleviation of EV price competition should lead to a demand recovery for EV batteries in the second half of 2023. Market leaders with better economies of scale and bargaining power are the ones to favour to achieve profitability in the batteries space.

To support the transition, there is also a significant demand for lithium. While Australia and South America possess upstream lithium mining resources, China accounted for around 63% of global lithium refinery capacity in 2022. Lithium supplies are expected to grow at a faster rate than demand over the next three years, with average lithium carbonate prices set to decline. However, lithium producers with higher self-sufficiency rates can sustain better profitability due to lower production costs.

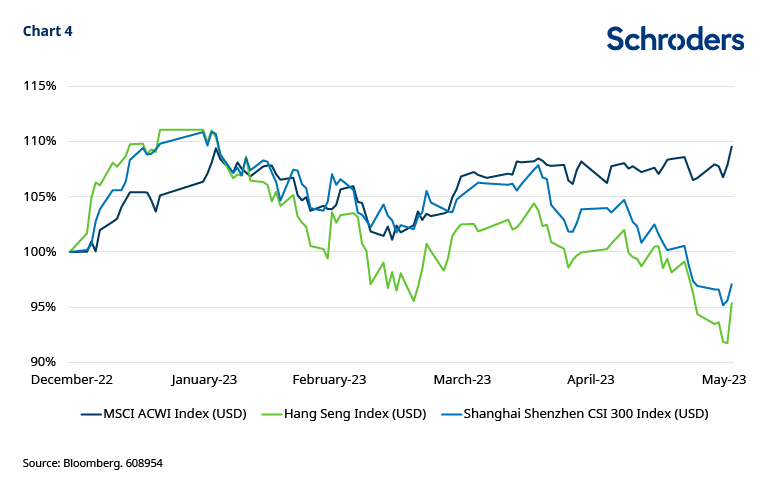

Currently, Asian stocks and Asian convertibles have fallen out of fashion. Hence, there is a strong counter-cyclical case for investing in this region now. It’s time for Asia to close that gap

Chart 4: Hang Seng and CSI 300 vs global MSCI World

The argument is especially strong in times of positive yield. The Refinitiv Asia ex Japan convertible bond index yields 4.6% (Yield to Maturity as of 31 May 2023). Hence, investors are getting paid to wait until equity markets close that gap.

In conclusion, convertibles offer an attractive way to build exposure to Asia and investing in Asian convertible bonds can provide additional diversification benefits for investors.

—

Originally Posted June 21, 2023 – The new opportunities in Asian convertible bonds

e views and opinions contained herein are those of Schroders’ investment teams and/or Economics Group, and do not necessarily represent Schroder Investment Management North America Inc.’s house views. These views are subject to change. This information is intended to be for information purposes only and it is not intended as promotional material in any respect.

Disclosure: Schroders

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realized. These views and opinions may change. Schroder Investment Management North America Inc. is a SEC registered adviser and indirect wholly owned subsidiary of Schroders plc providing asset management products and services to clients in the US and Canada. Interactive Brokers and Schroders are not affiliated entities. Further information about Schroders can be found at www.schroders.com/us. Schroder Investment Management North America Inc. 7 Bryant Park, New York, NY, 10018-3706, (212) 641-3800.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Schroders and is being posted with its permission. The views expressed in this material are solely those of the author and/or Schroders and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.