This is a special issue of BMO GAM’s Monthly House View. Our usual format will return in January.

From higher interest rates to near-record inflation, 2023 tested investors’ mettle. On the geopolitical front, conflict in the Middle East has joined the ongoing Russia-Ukraine war as a source of uncertainty and potential instability, while in the United States, a significant presidential election is on the horizon. Meanwhile, for markets, 2023 may be best remembered as the year developments in artificial intelligence (AI) took the world by storm, propelling the stock prices of the ‘Magnificent Seven’ tech companies—Apple, Alphabet, Microsoft, Amazon, Meta, Tesla, and Nvidia—into the stratosphere.

From higher interest rates to near-record inflation, 2023 tested investors’ mettle.

As we look ahead to 2024, questions on these and other issues remain, and new questions will surely present themselves. What forces will shape markets and economies over the next 12 months? And how will they affect investors’ portfolios?

This special issue of BMO GAM’s Monthly House View represents our best insights into what the coming year may hold—based on extensive research, hard data, and our team’s experience and expertise. With topics ranging from fiscal policy and corporate leverage to the emergence of Alternative investments and the state of the traditional 60% equity/40% bonds portfolio, these are 10 big investment trends to watch in 2024.

#1: RECESSION

How Bad is the Economic Consensus?

Predictions of a recession date back more than a year, and many analysts—including us—still see a mild downturn as the most likely scenario; Canada, in fact, may already be rolling into a technical recession. It’s important, however, for investors not to pay too much attention to the economic consensus when making long-term investment decisions. 2024 is likely to see the peak effects of monetary policy tightening and reveal a weaker economy, which is no surprise. For investors, that just means that 2024 could turn out to be the year for fixed income to shine.

Source: Bloomberg, BMO GAM, as of October 31, 2023.

#2: INFLATION

Are Rising Prices Transitory After All?

Inflation fears dominated 2023, with echoes of the double-digit inflation of the 1970s reverberating in investors’ minds. The good news is that over the past several months, rising prices have largely normalized, calming some of those concerns. Our expectation is that slowing economic growth should reinforce low and stable inflation into 2025—and that this normalization is likely to serve as a tailwind for equities and bonds.

Source: Bloomberg, BMO GAM, as of September 30, 2023.

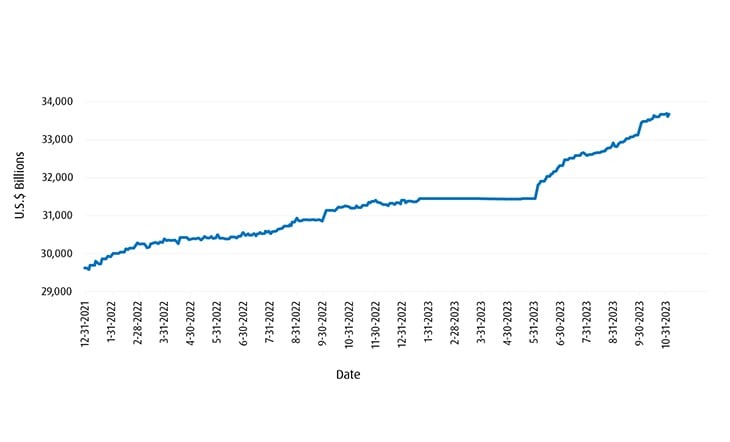

#3: FISCAL POLICY

Will Higher Interest Rates Revive Fiscal Hawks?

Needless to say, higher-for-longer interest rates do not mix well with governments’ rising debt burden. In the United States, net interest outlays for 2023 surged past $1 trillion and are continuing to rise. At the same time, public opinion seems to be shifting, with voters indicating increasing unhappiness with the ongoing policy mix. Is austerity the answer? Unlikely—history tells us that fiscal austerity virtually guarantees a recession. In our view, the path of least resistance for policy-makers is lower interest rates, and perhaps tolerance for an inflation rate of 3% rather than the traditional 2% target.

Source: Bloomberg, BMO GAM, as of October 31, 2023.

Source: Bloomberg, BMO GAM, as of October 31, 2023.

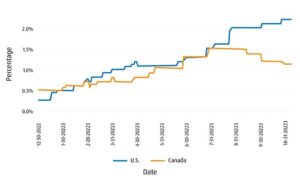

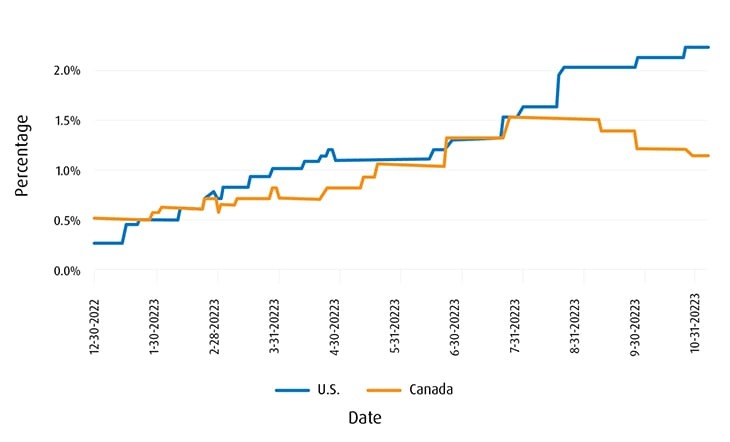

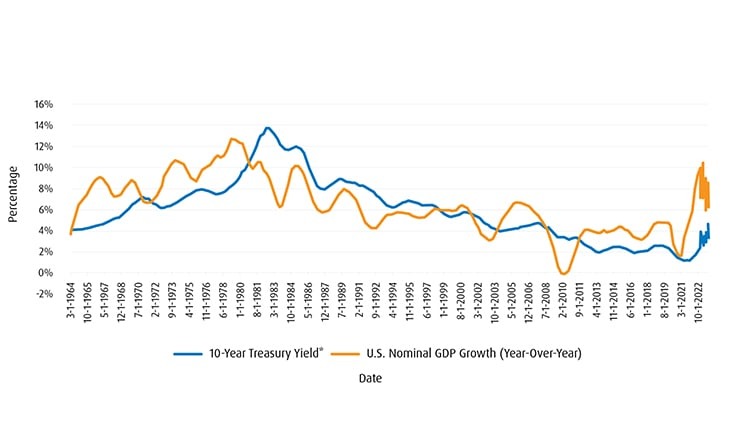

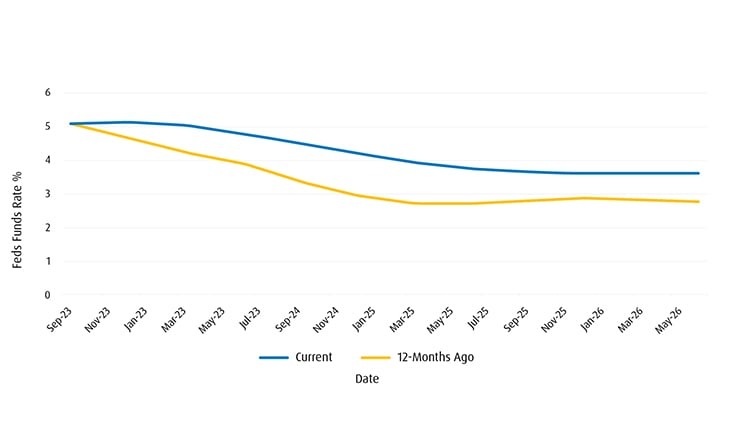

#4: MONETARY POLICY

Higher-for-Longer Interest Rates Will Be Tested

As the debt burden grows, real economic growth and inflation are poised to continue cooling into 2024. Fixed income markets see higher-for-longer as the most likely scenario, but we think even a soft landing could mean much lower interest rates—albeit perhaps not a return to a zero-interest rate policy (ZIRP) of the 2010s.

Source: Bloomberg, BMO GAM, as of November 8, 2023. *Note: 8-quarter moving average.

Source: Bloomberg, BMO GAM, as of November 8, 2023.

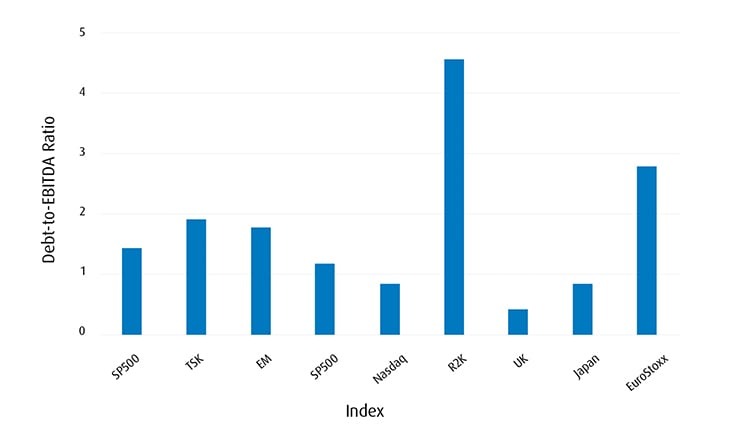

#5: CORPORATE LEVERAGE

Watch for the Rise of the Zombies

High interest rates mean big problems for European equities and U.S. small caps. This stands in contrast to large U.S. Technology firms (like those listed on the Nasdaq) and U.K. and Japanese equities, which are less exposed to interest rates. In general, there is also more debt exposure in Canada than in the U.S. These differences create a bifurcation across major global equity markets—meaning that the timing and magnitude of rate cuts in 2024 could be an important driver of relative performance across regions and sectors.

Source: Bloomberg, BMO GAM, as of November 8, 2023. EBITDA: Earnings before interest, taxes, depreciation, and amortization.

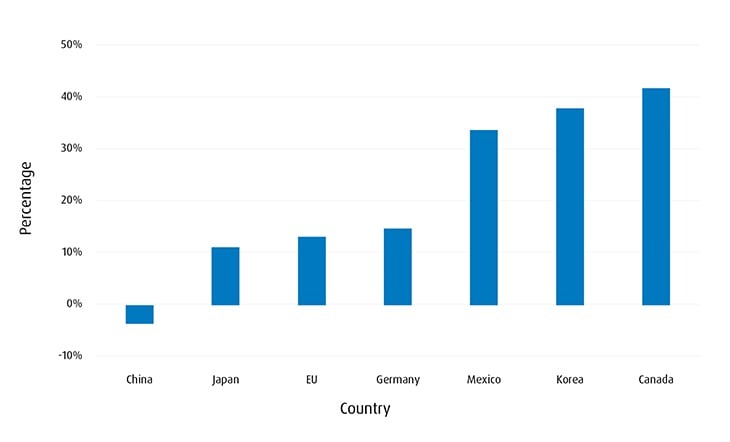

#6: GEOPOLITICS

Deglobalization or Regionalization?

Tensions between the United States and China ratcheted up in 2023, and that may continue into 2024. But do not confuse the deglobalization trend with regional, “friendly” shifts in global trade. So-called ‘nearshoring’ or ‘friend-shoring’ means that for countries aligned with the U.S., like Canada, trade opportunities are likely to grow.

Source: Bloomberg, BMO GAM, as of September 30, 2023.

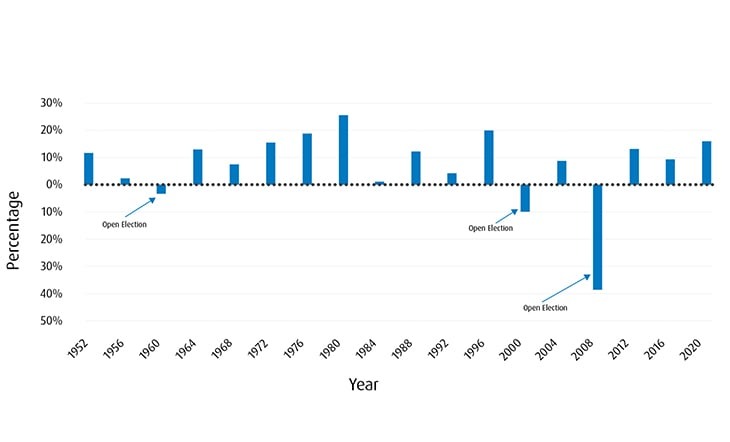

#7: U.S. POLITICS

U.S. Presidential Election Years Are Usually Good for Stocks

Here’s a compelling statistic: since 1952, the S&P 500 has not declined in a year in which an incumbent president was running for re-election. Yes, stocks have occasionally declined in election years, but in each of those three cases—1960, 2000, and 2008—it was an open election with no incumbent running. Why is this the case? In short, presidents tend to use whatever policy levers are needed to boost the economy, shore up their support, and maximize their chances of being re-elected.

Source: Strategas Research Partners.

#8: ARTIFICIAL INTELLIGENCE

Join the Revolution

Technology companies, including the ‘Magnificent Seven,’ are finding new ways to expand their already-dominant businesses. In 2023, we witnessed the increasing footprint of transformative technologies like A.I. across all aspects of economy activity, including the old economy—industries like manufacturing and agriculture. Don’t be surprised if Big Tech continues to lead in 2024.

Tech Platforms: Time to Reach 100 Million Users

| Rank | Platform | Launch | Time to 100M Users |

|---|---|---|---|

| 1 | Threads | 2023 | 5 days |

| 2 | ChatGPT | 2022 | 2 months |

| 3 | TikTok | 2017 | 9 months |

| 4 | 2011 | 1 year; 2 months | |

| 5 | 2010 | 2 years; 6 months | |

| 6 | Myspace | 2003 | 3 years |

| 7 | 2009 | 3 years; 6 months | |

| 8 | Snapchat | 2011 | 3 years; 8 months |

| 9 | YouTube | 2005 | 4 years; 1 month |

| 10 | 2004 | 4 years; 6 months |

Source: Visual Capitalist.

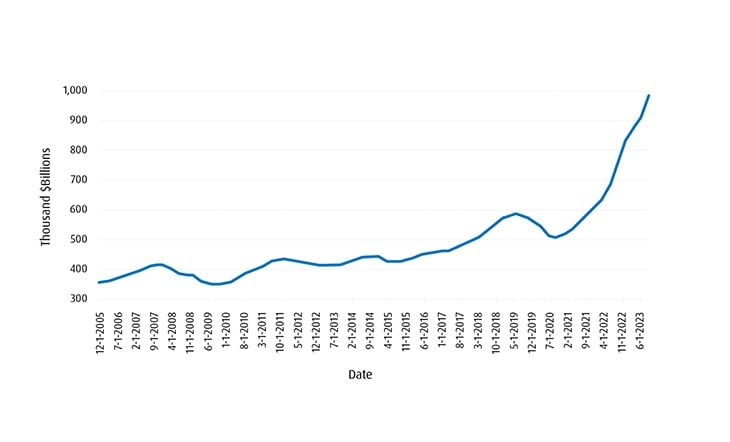

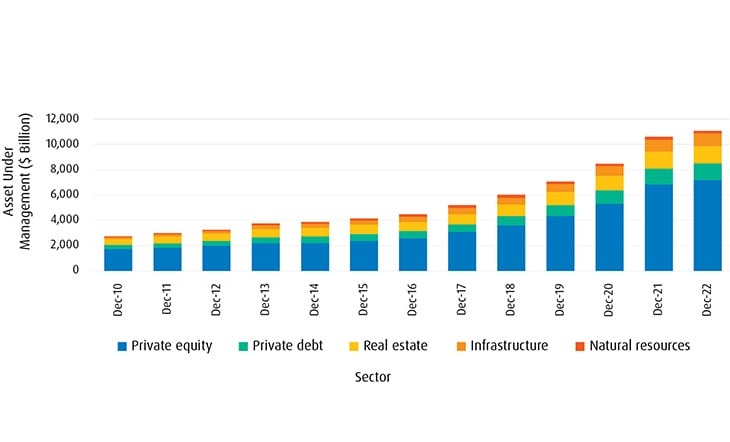

#9: ALTERNATIVES

The Quest for Diversification Will Accelerate

Retail investors increasingly seek to invest like large institutions, gaining exposure to non-traditional asset classes and investment styles for greater portfolio diversification. While interest rates have normalized from the low levels of the past decade, elevated market volatility has provided yet another reason for investors to diversify with alternative investments like private equity, private debt, real estate, and infrastructure.

The Growth of Alternative Investments (2010-2022)

Source: Preqin Pro, as of January 18, 2023.

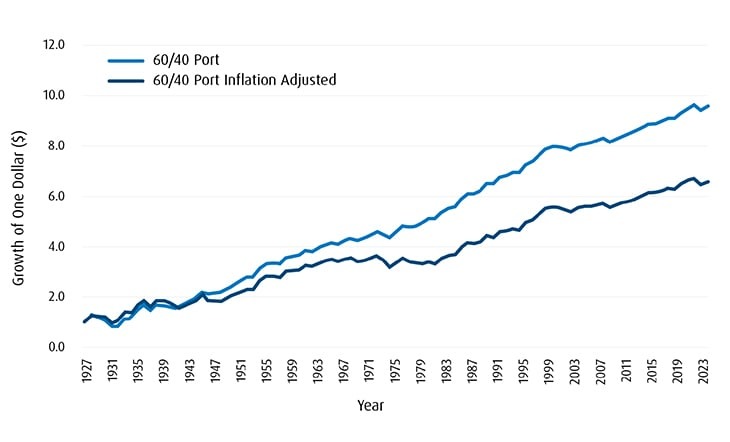

#10: REBOOTING THE 60/40 PORTFOLIO

Time to Embrace the Ballast of Higher Interest Rates

It might not make for news-grabbing headlines, but the traditional 60% equities/40% bonds portfolio has delivered over the years. In the 2010s, low interest rates left the burden of expected returns on equities. But more recently, bond yields at levels not seen since before the Global Financial Crisis of 2007–2008 have helped to rejuvenate the 60/40 portfolio and justified its fixed income allocation.

Source: Bloomberg, BMO GAM, as of October 31, 2023.

CLOSING REMARKS

2023 has delivered several positive surprises to investors as the economy navigated through a challenging environment dominated by elevated inflation and interest rates. In many ways, we think investors should feel more confident heading into the new year as the worst of the storm is largely behind us. We expect 2024 to be more about the long-and-variable lags of monetary policy. In contrast to 2023, this should help limit the scope for meaningful upside economic surprises and potentially reveal recession scars, most notably in Canada, but also in Europe. In this context, 2024 should see central banks normalize their policy stance and cut interest rates. While we think there is a wider set of macroeconomic paths for fixed income to shine in 2024, the performance of equities might ultimately depend on how successful central banks will be at delivering a soft landing, especially in the U.S. The continuation of ‘immaculate disinflation’ would likely be a moderate tailwind for risk assets, but we also recognize that history has generally not been kind to equities when global economic activity rolls into a recession.

In many ways, we think investors should feel more confident heading into the new year as the worst of the storm is largely behind us.

What recent history has proven is that it’s crucial for investors to be nimble when navigating turbulent financial markets. While investors might find such environments nerve-racking, they generally prove ideal for more tactical opportunities in portfolio solutions as markets can often switch from exuberance and mania to excessive pessimism and fear.

—

Originally Posted December 2023 – 10 Big Investment Trends for 2024

Disclosure: BMO Exchange Traded Funds

Commissions, management fees and expenses all may be associated with investments in exchange traded funds. Please read the ETF Facts or prospectus of the BMO ETFs before investing. Exchange traded funds are not guaranteed, their values change frequently and past performance may not be repeated.

For a summary of the risks of an investment in the BMO ETFs, please see the specific risks set out in the BMO ETF’s prospectus. BMO ETFs trade like stocks, fluctuate in market value and may trade at a discount to their net asset value, which may increase the risk of loss. Distributions are not guaranteed and are subject to change and/or elimination.

BMO ETFs are managed by BMO Asset Management Inc., which is an investment fund manager and a portfolio manager, and a separate legal entity from Bank of Montreal.

®/™Registered trade-marks/trade-mark of Bank of Montreal, used under licence.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from BMO Exchange Traded Funds and is being posted with its permission. The views expressed in this material are solely those of the author and/or BMO Exchange Traded Funds and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.