")

Key takeaways

It’s time once again to give thanks

There’s never a bad time to list reasons for being thankful. But this year, our annual Thanksgiving exercise feels like it takes on even greater significance.

There’s much for investors to celebrate

While we still face challenges ahead, this year I celebrate the global vaccine rollout, the booming US job market, and much more.

There’s never a bad time to list reasons for being thankful. But this year, our annual exercise feels like it takes on even greater significance. It was only a year ago that COVID cases were rising at catastrophic rates, and hospitalization and fatality rates were following in tow. Vaccines trial results were promising but still pending approval. The economic recovery had commenced but was still tenuous. What a difference a year makes.

As we approach Thanksgiving 2021, we recognize that challenges remain. The effects of the pandemic are still with us. COVID cases have come down meaningfully but are elevated.1 The prices of goods, including the cost of Thanksgiving turkeys, have risen as consumers unleashed pent-up demand on an economy struggling to rebuild supply.2 Many American families are still wary about gathering for yet another holiday. Nonetheless, substantial progress has been made in the past year and is worth celebrating. Instead of lamenting the fact that our lives are not yet back to “normal,” let’s instead focus on the true spirit of the holiday and remind ourselves of what we’re thankful for.

Below is a list of 10 items that investors can be thankful for this year.

1. Vaccines have been rolled out globally

At last year’s Thanksgiving tables (many of which were outside or in garages), many families spoke longingly of a vaccine rollout at some future point. Since then, 194 million Americans have been fully vaccinated with another 31 million receiving at least one jab.3 Vaccines are also now available to 28 million US children ages 5 to 11.4 It’s not just a US story. Countries such as South Korea, Canada, Japan, and Italy have inoculated over 75% of their populations.5 For their part, emerging market countries such as Vietnam and Thailand, which as of April of this year had not embarked on an immunization process, have now partially vaccinated over 60% of their populations.5

2. A semblance of normal life is returning

Many Americans are emerging from their homes. Airline travel has returned to near-2019 levels with roughly 1.5 to 2.0 million Americans going through TSA checkpoints each day.6 Restaurant reservations are only 4% below 2019 levels.7 Broadway is back. Stadiums are full.

3. US households are generally in good shape

US household net worth stands at $142 trillion, an all-time high and up 28% from the depths of the 2020 recession, driven in part by rising equity and home prices.8

4. The US job market is booming

Last Thanksgiving, the unemployment rate stood at 6.9%. Since then, 5.8 million Americans have joined the ranks of the employed. Wages are rising as employers compete to find workers.9 While some may view higher wages as an ominous sign for corporate profitability and future inflation, it’s important to remember that wages as a percent of gross domestic product had previously fallen to its lowest level in the post-WWII period and is still well below the historical average.10 Higher wages tend to drive demand.

5. Business investment is robust

Businesses are flush with cash and are investing at a rapid rate,11 which ultimately will help to rebuild the nation’s supply of goods and potentially improve future productivity.

6. Inflation is elevated, but there may be early signs of supply-chain challenges easing

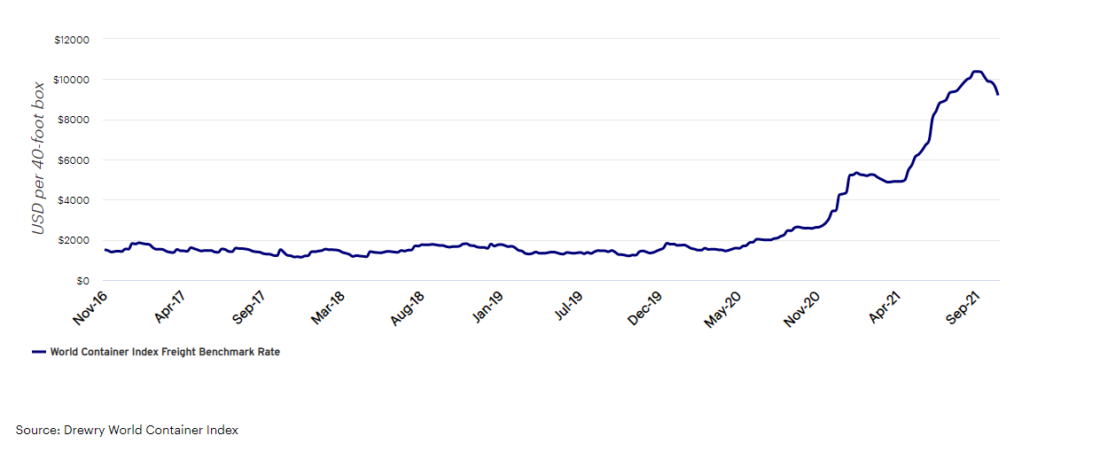

Higher prices are a concern but there may be initial signs that the worst of the problems could be abating. For example, Chinese exports increased 27.1% last month, as the nation’s exports through October have already surpassed all of 2020.12 Goods such as household appliances, lightings, and furniture saw the fastest export growth in October. In addition, shipping costs (shown below) may be showing signs of having peaked. Further, there are signs that the semiconductor industry could move closer to balance in the coming months, particularly as factories in Asia come back online.

Have shipping costs peaked?

7. The market didn’t taper tantrum this time

For all the hand wringing over the US Federal Reserve tapering its asset purchases, this time, unlike in 2013, the market took it largely in stride. It’s a testament to the current strength of the global economy compared to 2013 and highlights the markets’ embrace of tighter policy at a time when inflation is elevated.

8. Companies are growing into their valuations

Corporate earnings have been so strong that the price-to-earnings ratio of the US equity market has declined meaningfully this year — from 30.8x at the end of February to 25.4x at the end of September — even as stocks have staged a strong advance.13

9. The backdrop for equities remains strong

I expect the global economy to continue to expand in 2022 albeit at a slower pace. A moderation in growth should help to ease inflationary pressures and provide cover for the US Federal Reserve to remain relatively accommodative for the foreseeable future. There is still a substantial amount of money on the sidelines,14 and we would expect that money to continue to find its way into the equity market. Market cycles tend to end with excessive investor optimism and a prolonged monetary policy tightening cycle. Seen from that lens, one could surmise that the business and market cycles have room to run.

10. Human ingenuity continues to solve our most challenging problems

Last year I wrote that investors betting against the economic and market recovery were betting against medicine, science, and the nation’s policymakers. A year later, US markets are near all-time highs. The past year, while incredibly challenging and heartbreaking, has steeled my optimism for the future, knowing that while we always face challenges, we always come back stronger.

Happy Thanksgiving! Be safe and be well.

Footnotes

- 1 Source: World Health Organization, 11/8/21

- 2 Source: US Bureau of Labor Statistics, 10/31/21

- 3 Source: US Centers for Disease Control and Prevention, 11/10/21

- 4 Source: US Centers for Disease Control and Prevention, 11/2/21

- 5 Source: World Health Organization, 11/8/21

- 6 Source: US Transportation Security Administration, 11/8/21

- 7 Source: OpenTable, 11/8/21

- 8 Source: US Federal Reserve, 6/30/21, latest data available.

- 9 Source: US Bureau of Labor Statistics, 10/31/21

- 10 Source: St. Louis Fed, 9/30/21

- 11 Source: US Census Bureau, 9/30/21. As represented by Capital Goods New Orders Nondefense Excluding Aircraft.

- 12 Source: Customs General Administration People’s Republic of China, 10/31/21

- 13 Source: Bloomberg, Standard & Poor’s. As represented by the S&P 500 Index. Indices cannot be purchased directly by investors. Past performance does not guarantee future results.

- 14 Source: Investment Company Institute, 11/8/21. As represented by ICI Money Market Funds Assets.

—

Originally Posted on November 18, 2021

10 Reasons for Investors to Give Thanks BY Invesco US

Important information

NA1918539

Past performance is not a guarantee of future results.

All investing involves risk, including the risk of loss. This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

The World Container Index, produced by Drewry, is a composite of container freight rates on eight major routes shipping routes to and from the US, Europe, and Asia.

The price-to-earnings (P/E) ratio measures a stock’s valuation by dividing its share price by its earnings per share.

The opinions referenced above are those of the author as of Nov. 18, 2021. These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

Disclosure: Invesco US

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED

MAY LOSE VALUE

NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s Retail Products and Collective Trust Funds. Institutional Separate Accounts and Separately Managed Accounts are offered by affiliated investment advisers, which provide investment advisory services and do not sell securities. These firms, like Invesco Distributors, Inc., are indirect, wholly owned subsidiaries of Invesco Ltd.

©2024 Invesco Ltd. All rights reserved.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Invesco US and is being posted with its permission. The views expressed in this material are solely those of the author and/or Invesco US and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.