By: Jon Maier, Michelle Cluver

Artificial Intelligence (AI), Taylor Swift, and the Federal Reserve (Fed) had an oversized impact on either the economy or the market during 2023. Excitement surrounding AI helped the S&P 500 and Nasdaq 100 recoup a majority of their 2022 pullback.1 This exceptionally strong market rebound dominated the first half of 2023, boosting sentiment and helping markets navigate the regional banking crisis and recession expectations. Optimism surrounding AI’s potential future economic impact powered markets higher while Taylor Swift’s Eras tour boosted U.S. economic activity. Labor market tightness and the consumer’s continued willingness to spend increased the possibility of a soft landing, shifting the market’s focus back to interest rates. While “higher for longer” interest rate expectations temporarily took the shine off growthier market segments, the Fed’s actions may finally be starting to have an impact on underlying economic activity.

For investors, the task in the new year is to navigate what we expect to be a transition from robust economic growth and high interest rates to an environment of more subdued economic growth and declining yields. We believe we’re at an inflection point, with the Fed and key central banks likely already at their terminal interest rates, S&P 500 earnings returning to growth, onshoring a growing trend, and looming geopolitical risks. All these factors impact portfolio positioning for the year ahead. Overall, we believe diversification and quality core positioning remain important, but portfolios should also include select exposure to key growth areas and market segments that stand to benefit from fiscal support.

Key Takeaways

- Interest rates likely already being at their peak puts greater importance on portfolio diversification and the balance between key growthier areas and a resilient core.

- A quality and low volatility tilted core is likely to be beneficial as economic growth slows.

- The adoption of AI technology and its monetization is likely to play out over multiple years, having a lasting impact on both markets and the economy.

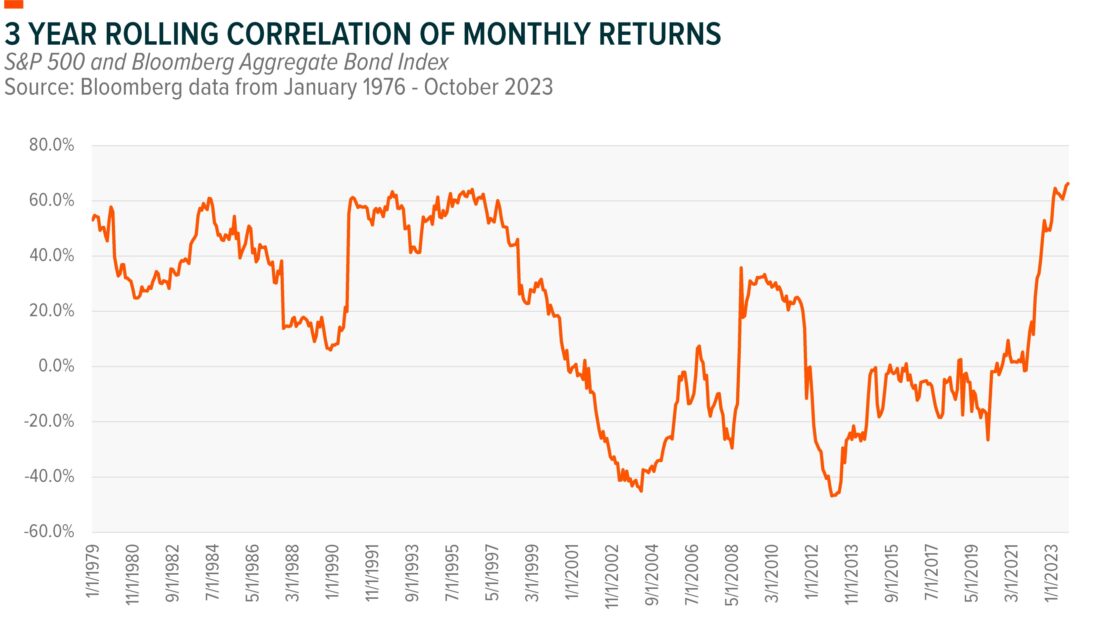

Importance of Portfolio Diversification Grows

The tough times for fixed income may be coming to an end

The last two years were a challenge for multi-asset portfolios. Equity and fixed income markets grappled with red-hot inflation and a rapid rise in policy rates. These factors increased the correlation between asset classes to multi-decade highs. But the 60-40 portfolio isn’t dead, it just needed yields to return to normalized levels.

We believe that markets may be at a turning point. As inflation subsides, there is opportunity for the Fed to eventually reduce policy interest rates while maintaining restrictive real interest rates. However, we view current market expectations for more than 100 basis points (bps) in cuts by the end of 2024 as potentially too extreme.2

Historically, high-quality fixed income has positive returns in the 12 months following the peak in the Fed’s rate-hiking cycle. Peak interest rates, declining interest rate volatility, and moderating economic growth are all factors supporting a favorable backdrop for fixed income that may also help restore fixed income’s diversification benefits. With US$8 trillion currently in money market funds, we could soon start seeing net flows into equity and fixed income as nominal money market yields decrease.3

Balance between risk, quality, and low volatility as economic growth slows

We believe the U.S. economy is at a transition point that has important implications for portfolio positioning. U.S. economic growth surprised to the upside in 2023 as the long and variable lag of monetary policy was longer than initially expected. But Q3 2023 economic growth was likely the peak. The tight labor market and a large cost of living adjustment supported a one-time bump in spending, but consumer balance sheet strength deteriorated over the summer and credit card and auto loan delinquencies are rising.4,5 Softer economic releases during November and December have put GDP Now on a downward trajectory for Q4, reducing inflation and interest rate risks.6 Current economic data remains resilient, walking the fine line between being inflationary and recessionary – and hopefully keeping the economy on track to achieve a soft landing.

While a soft landing is our base case scenario for the U.S. economy, downside risks to economic growth remain—after all, there’s minimal difference between a soft landing and shallow recession. Quality remains a relevant factor exposure moving into the next economic cycle. Although quality is likely to lag in the near term as reduced interest rate risk boosts risk assets, healthy balance sheets and strong cash flows are likely to take the lead as concerns about economic growth gain prominence. As a factor, quality historically outperforms in the slowdown and the contraction phases of the economic cycle.7

The low volatility factor has been out of favor with the market; however, given the drawn-out nature of the slowdown and interest rates likely being at their peak, low volatility may help provide more support as economic growth slows.8 Additionally, low volatility could provide benefits should equity market volatility rise on any potential shock factors.

We believe quality and low volatility are important factors for core exposure, but if we achieve that elusive soft landing, risk assets may have much to celebrate. Historically, slowing economic growth with rising earnings per shares (EPS) has been one of the best environments for equities since the 1950s, and in our view, this is the most likely economic environment for 2024.9 This environment is also favorable for risk assets, with lower interest rates and economic growth expectations supporting growthier and more thematic areas of the market. S&P 500 earnings growth already went through its recession, returning to positive territory in Q3 2023 with a 4.7% y/y increase.10 As the balance between goods and services demand normalizes, S&P 500 earnings are likely to improve. Typically, manufacturing is more sensitive to tightening financial conditions, which may assist with some convergence between services and manufacturing in 2024.11

Selective exposure to international

A soft landing is likely to come with a period of subdued global economic growth, particularly for developed markets. Estimates for 2024 global economic growth vary widely, from around 1.9% to 2.8% real GDP growth.12,13 European economic growth lost momentum in 2023, with stagnant Q3 GDP reducing 2023 GDP growth expectations to 0.6%. But economic activity is expected to improve into 2024 as inflation and policy tightening ease.14 The European Central Bank (ECB) is expected to lead the developed market in reducing policy interest rates, potentially starting rate cuts in Q1 2024.15

Global equities typically sell off in the three months leading up to a new round of monetary easing as markets price in expectations of slower economic growth. As a result, 2024 may be a tale of two halves, with slower global economic growth driving weaker first-half market performance and improving global economic growth leading to stronger performance in the second half.16

The 2024 international story is likely to diverge between developed and emerging markets (EM), as EM typically performs well in the 12 months following the final Fed interest rate hike. The softening U.S. dollar is already fostering a more favorable environment for EM. Additionally, while the U.S. and Europe are late cycle, China and Japan remain earlier in the cycle.17 This dynamic could create regional opportunities, especially when paired with a better balance between demand for goods and services, which could improve the Asian export cycle.18

AI Disruption Changing Commercial Paradigms

AI adoption is accelerating, and increased data use is likely to infiltrate all industries. While ChatGPT and the early forms of generative AI took the world by storm, the real opportunity is in commercial applications of AI models and the industries positioned to benefit from their adoption over the coming decades.

The computer and cell phone technology revolutions featured three distinct phases of adoption and market beneficiaries, and we expect AI to follow a similar path as it integrates into everyday technology.

- Phase 1: Computing power builds out using AI-compatible semiconductor chips.

- Phase 2: Digital infrastructure ramps up with cloud computing players.

- Phase 3: Interface and software companies capitalize by building or integrating AI models.

From a market perspective, 2023 was an excellent year for semiconductors, with the first phase of AI adoption focusing on building out compute resources. While compute power remains important, we believe the key beneficiaries of AI adoption are likely to broaden as AI monetization improves along the value chain.

Cloud Computing is a key theme that can benefit from generative AI’s growth. One emerging opportunity for cloud computing companies is AI-as-a-Service (AaaS), which is a way for them to monetize their offerings.19 The opportunity includes two key new business models, Model-as-a-Service (MaaS) and application programming interface (API), that can make it more affordable for companies to engage with AI without needing to build their own models.20

Fiscal Support Provides Multiyear Thematic Benefits

Expansionary fiscal policy supported U.S. economic resilience in 2023. Fiscal support is also encouraging U.S.-centric investment in areas that are likely to support long-term development of strategically important technology, benefitting themes such as AI and Automation. Despite increased scrutiny on budgetary and inflation concerns, reshoring critical manufacturing remains an area with bipartisan support.

Also, increased infrastructure spending and policies encouraged private sector investment into the manufacturing sector.21 While fiscal impulse provided about a 1 percentage point boost to GDP growth in 2023, given the higher base, this support is expected to fade in 2024. However, investment in U.S. infrastructure will continue over the decade and companies across its value chain can benefit.22

While the Fed may be Done, AI Adoption Has Only Just Begun

In a world that is continually evolving, innovation and change are inevitable – but we believe the rate of that change has been accelerating. We look forward to seeing how the AI story unfolds in the coming year and the decades ahead.

We wish you all the best this holiday season and a happy and healthy new year!

—

Originally Posted December 14, 2023 – 2024 Outlook: Done or More to Come?

Footnotes

- Bloomberg data as of 11 December 2023

- Bloomberg data as of 30 November 2023

- Goldman Sachs, Outlook for 2024: Time for Balance – Modest Returns, Better Diversification, November 21, 2023

- BofA Securities, US Viewpoint: Fiscal Impulse: Running Out of Steam, November 16, 2023

- New York Fed, Household Debt and Credit Q3 2023, November 2023

- Federal Reserve Bank of Atlanta, GDPNow, December 7, 2023

- Bloomberg data as of 16 November 2023. MSCI Indices used for factors (quality, growth, value) vs. MSCI USA Index. Business cycle dates are via NBER going back to 1979

- Goldman Sachs, Outlook for 2024: Time for Balance – Modest Returns, Better Diversification, November 21, 2023

- BofA Securities, Thematic Investing: 10 Themes for 2024 – Breadth in Rate Cuts and Markets, November 27, 2023

- Factset, Earnings Insight Infographic: Q3 2023 by the Numbers, November 30, 2023

- Goldman Sachs, Outlook for 2024: Time for Balance – Modest Returns, Better Diversification, November 21, 2023

- Morgan Stanley, 2024 Global Macroeconomic Outlook: Central Banks Look ‘Just Right’ on Rates, November 22, 2023

- Citi, Global Economic Outlook & Strategy – Prospects for 2024: Still Not Out of the Woods, December 1, 2023

- European Commission, Autumn 2023 Economic Forecast: A Modest Recovery Ahead After a Challenging Year, November 15, 2023

- Bloomberg data as of December 5, 2023

- Morgan Stanley, 2024 Investment Outlook: Threading the Needle, November 22, 2023

- Goldman Sachs, Outlook for 2024: Time for Balance – Modest Returns, Better Diversification, November 21, 2023

- BofA Securities, Thematic Investing: 10 Themes for 2024 – Breadth in Rate Cuts and Markets, November 27, 2023

- Global X, Generative AI Delivers a Boost to Cloud Computing, October 13, 2023

- Global X, ChatGPT’s One-Year Anniversary: Generative AI’s Breakout Year, November 27, 2023

- BofA Securities, US Viewpoint: Fiscal Impulse: Running Out of Steam, November 16, 2023

- BofA Securities, Global Economics Year Ahead 2024: Growing Apart, Cutting Together, November 19, 2023

Glossary

Bloomberg Aggregate Bond Index: The Bloomberg Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-through), ABS and SMBS (agency and non-agency).

Earnings per share (EPS): A measurement of a company’s profitability, total net income divided by the number of shares outstanding.

NASDAQ 100: The NASDAQ 100 index includes 100 of the largest non-financial companies listed on its stock market.

S&P 500 Total Return Index: The index includes 500 leading U.S. companies and captures approximately 80% coverage of available market capitalization.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.

Leave a Reply

Disclosure: Global X ETFs

Carefully consider the Fund’s investment objectives, risk factors, charges and expenses before investing. This and additional information can be found in the Fund’s full or summary prospectus, which may be obtained by calling 1-888-GX-FUND-1 (1.888.493.8631), or by visiting globalxfunds.com. Read the prospectus carefully before investing.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Global X ETFs and is being posted with its permission. The views expressed in this material are solely those of the author and/or Global X ETFs and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Good stuff, thanks.

Thanks for engaging!