")

ZINGER KEY POINTS

- The annual inflation rate was 3% in June, down from 4% in April and below the 3.1% predicted.

- The core inflation rate was broadly in line with estimates, as shelter continues to move higher.

The U.S. consumer price index (CPI) inflation decelerated more than predicted in June, increasing investor conviction that the Fed may decide for only one more rate hike and then halt its tightening cycle.

The annual inflation rate in the United States dropped from 4% in May to 3% in June, according to data released by the Bureau of Labor Statistics on Wednesday.

The long-awaited inflation report is just below the the average economist prediction of 3.1%, and marked the twelfth consecutive month of declining inflation and the lowest reading since March 2021.

Inflation Falls In June: Key Highlights

- The annual increase in the U.S. CPI was 3% last month, down from the 4% recorded in May and coming in below the 3.1% estimate.

- On a monthly basis, the CPI inflation increased by 0.2% in June, accelerating from the 0.1% increase in May. The figure was below the 0.3% forecast.

- Energy prices rose 0.6% in June after a 3.6% monthly drop in May, and were down 16.7% compared to a year ago.

- Food prices ticked 0.1% higher on a monthly basis, and were 5.7% higher than a year ago.

- Core inflation, which excludes volatile food and energy goods from the CPI basket, increased 4.8% year-on-year, well below May’s 5.3% reading and missing the 5% expected.

- Core inflation rose 0.2% month-over-month in June, below both the 0.4% gain seen in May and the 0.3% increase economists predicted. It marks the the smallest monthly increase in core inflation since August 2021.

- Services were the main contributor to overall CPI inflation, with shelter rising 0.4% on the month and 7.8% year-on-year.

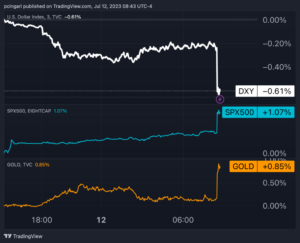

Market Reactions: Dollar Tumbles, Stocks Rally

Trader estimates for the Fed’s July meeting are unchanged, with probabilities a 0.25% rate hike remaining at 92%. The chances of another rate hike in September increased from 18.5% prior to the release to 15% after the print. The market assigns a 31% probability of two Fed rate hikes by November, down from 33% prior to the CPI release.

The dollar, as closely tracked by the Invesco DB USD Index Bullish Fund ETF (ARCA: UUP), tumbled 0.6% in the minutes following the June CPI data. The U.S. dollar gauge fell to the lowest since early May.

Treasury yields sharply declined, with the 10-year yield down 8 basis points to 3.88% and the two-year yield down 13 basis points to 4.75%.

S&P 500 futures rose 1%, while Nasdaq 100 futures were 1.2% higher, ahead of the Wall Street opening bell. The SPDR S&P 500 ETF Trust finished the last two sessions in the green.

Gold, as closely tracked by the SPDR Gold Trust ETF rose 0.8%, buoyed by a lower U.S. dollar and declining Treasury yields

Chart: Asset Reactions To June CPI Report

—

Originally Posted July 12, 2023 – CPI Inflation Falls To Lowest Level Since March 2021: Traders Rethink Fed’s Policy Outlook

Disclosure: Benzinga

© 2022 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Benzinga and is being posted with its permission. The views expressed in this material are solely those of the author and/or Benzinga and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.