By Bluford Putnam and Erik Norland

The appetite for risk management is likely to grow strongly in the coming years.

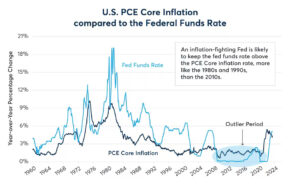

Of the many factors that influence the appetite for risk management, the one primary factor that has undergone a major change is the shift in the Federal Reserve (Fed) and European Central Bank’s policy focus during 2022 and 2023 towards fighting inflation and potentially keeping short-term interest rates above prevailing expectations for inflation for sustained periods of time, except possibly during serious recessions.

This policy shift reversed a decade or more of the zero-interest-rate policy (ZIRP) that created incentives for risk-taking and dramatically suppressed the appetite for risk management. The persistence of the ZIRP culture encouraged the view among asset market participants that the “central bank had your back,” and among equity traders, the environment of zero-rates led to popular maxims such as “buy the dips” and “there is no alternative (to equities)” or “TINA”.

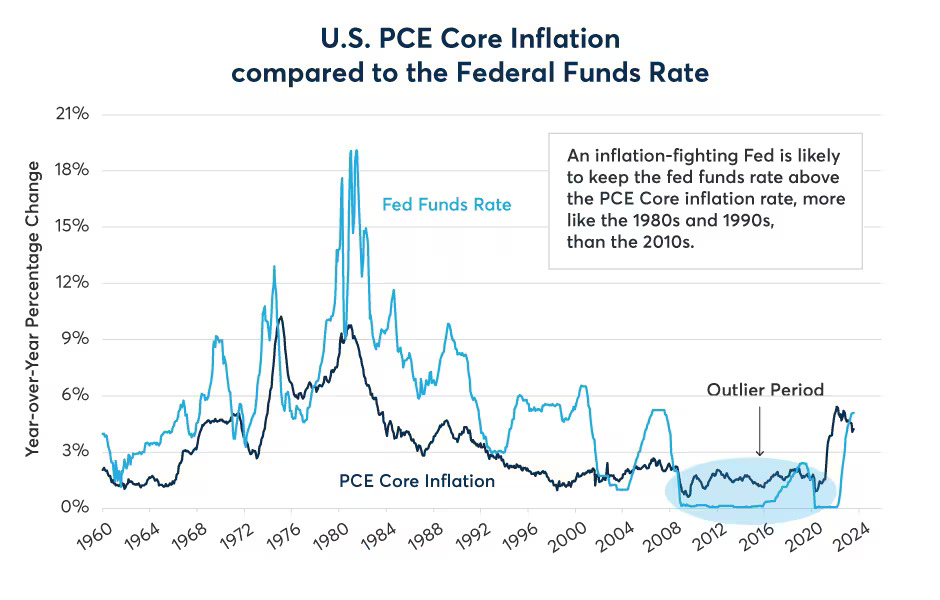

During much of the last two decades, the Fed set the stage for a suppression of the appetite for risk management with the commencement in 2003 of the 1% Federal Funds rate policy of the Greenspan-era, followed by the introduction of near 0% Federal Funds rates in the Bernanke-era following the Great Recession of 2008. Overall, from January 2009 through June 2022, the U.S. Federal Funds rate was below the year-over-year trailing CPI inflation rate for 83% of the time. Compared to the 1982-2002 period, the Federal Funds rate was above the prevailing rate of inflation 97% of the time, and the rare exceptions were typically associated with recessions or periods of economic weakness. That is, prior to the 2000s, the U.S. economy largely experienced overnight rates above the prevailing rate of inflation or positive real interest rates. Then, in the more recent era, the experience was dominated by negative real interest rates, and now we are returning to a positive real rate environment.

Our theoretical contention is that the degree of suppression of the appetite for risk management from an era of negative real short-term interest rates was of an exceptionally high magnitude, even if we cannot measure it. The practical problem, however, is that our assessment of current behavior by financial market participants is that they view the last 20+ years as “normal.” In many cases, those years served as the economic context for their whole careers. As a result of this “career context bias,” indeed because of it, the degree of suppression of the appetite for risk management during the 2003-2021 period is being grossly underestimated. And that means we are also under-estimating the importance of risk management in the new environment of positive real interest rates.

There are three additional considerations we wish to emphasize when thinking about the evolution of Fed policy and how it influences risk management. First, there is the shift from quantitative easing (QE, or asset purchases) to quantitative tightening (QT, or allowing the balance sheet to shrink as securities mature – note the Fed is not selling). QE distorted the price discovery process for both fixed income and equities to a very large degree, and the price discovery distortion has now been removed. QT has little impact so long as the Fed is not an active seller and only shrinks its balance sheet by not replacing maturing securities. That is, QT is not at all the inverse of QE. QE was about active buying of securities, and QT is only about passive non-replacement of maturing securities.

Second, the Fed has a well-known reluctance to change course, and then change course again. That is, for 2022-2023, the Fed has been on a course of raising rates. A pause is fine, but a cut in rates is highly unlikely until the Fed is highly confident it will not have to admit making a mistake and raise rates again.

Third, the Fed has taken a very hardline stance in terms of its current insistence of returning to its 2% core inflation target. This stands in contrast to the Fed’s willingness to consider in 2017-2018 some over-shooting of the 2% core inflation target, but that was when core inflation was stuck marginally below 2%. This hardline on keeping the 2% core inflation target is important because many of the key influences that kept core inflation around 2% during the 1994-2020 period are either in reverse (e.g., globalization and demographics) or completely played out (e.g., internet growth promoting comparison shopping has given way to AI, which is more likely a labor-saving technology than helping to keep inflation low).

Consequently, when taking these three considerations into account, we are probably looking at a very long period of positive real interest rates. There might be brief periods of recessions when short-term rates are pushed below the rate of inflation only to come back above the inflation rate once the recession is over and policy re-assessed.

Putting it all together, there is tremendous upside in the potential for risk management activity that has yet to be realized or appreciated. With the new policy approach of short-term interest rates elevated above the prevailing long-term periods, the Fed is now allowing more risk in the economic system in their shift to fighting inflation. This means economic agents, from investors and traders to financial institutions to commercial enterprises are all going to need to spend more time on risk management as a critical element of future success.

Interestingly, this may turn out to be exceptionally positive in the long run for the performance of the economy. Our view is that there is a natural amount of risk in a highly complex and integrated economic system. If one suppresses the risk from one source, the risk inside the system does not necessarily disappear; it may just migrate to another feature of the economic system. Think of a balloon representing the risk in the system. One can squeeze on one end of the balloon, but the air and bulge (risk) moves to another part of the balloon. This is the idea of conservation of risk. The Fed and other government entities can move risk around the system, but this probably does not reduce the overall risk in our complex and dynamic economy. In a competitive, capitalistic system, perhaps, it is better policy for long-term economic growth to allow economic agents to have an efficient and non-distorted price discovery system so they can manage their risks efficiently and achieve a more optimal allocation of capital than was allowed in the era of zero rates and QE.

—

Originally Posted September 13, 2023 – End of an Era of Risk Management Suppression

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the author and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.