The communications blackout period around the January 30-31 FOMC meeting goes into effect at midnight on Saturday, January 20 and lasts through midnight on Thursday, February 1. At this writing, Fed officials have pretty much said all they have to say regarding the outlook for monetary policy. The data about inflation in December suggests that while disinflation has made meaningful progress, the overall pace of improvement could be reaching a plateau. On the plus side, inflation expectations over the medium-term point to anticipation of moderation in inflation nearer the Fed’s two percent flexible average inflation target. The combination suggests that policymakers won’t be in a hurry to lower rates, but they are unlikely to raise them again absent an unpleasant shock to the economy.

There’s not a lot of data on the economic release calendar that is likely to alter current expectations for no change in monetary policy when the FOMC deliberates.

The advance estimate of fourth quarter GDP at 8:30 ET on Thursday is forecast to come in well below the third quarter’s 4.9 percent growth. Early estimates look for an increase of just over 2 percent. Growth should get support from robust consumer spending, but there’s likely to be a pinch for business and residential investment from higher interest rates, and caution regarding adding to inventories. Growth of around 2 percent is still above the FOMC’s longer-run estimate of up 1.8 percent, not the sort of below trend growth it has been forecasting. However, the first quarter 2024 could well reflect cooler growth as businesses ease up on hiring and wage increases – where they can – along with some drag as markets start to believe the FOMC that rate cuts are not right around the corner.

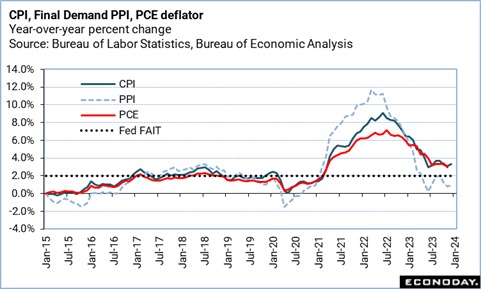

The data on personal income and spending in December at 8:30 ET on Friday includes the PCE deflator numbers. These should more-or-less align with the already-reported CPI movements. What may be more interesting is in the income data to see if there is an uptick in end-of-year bonuses and dividends, and in payouts of government benefits. Some bonuses will not show up until January. There’s also a substantial 3.2 percent increase in social security benefits in January, and some mandated increases in minimum wages.

—

Originally Posted January 2024 – High points for US economic data scheduled for January 22 week

Disclosure: Econoday Inc.

Important Legal Notice: Econoday has attempted to verify the information contained in this calendar. However, any aspect of such info may change without notice. Econoday does not provide investment advice, and does not represent that any of the information or related analysis is accurate or complete at any time.

© 1998-2022 Econoday, Inc. All Rights Reserved

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Econoday Inc. and is being posted with its permission. The views expressed in this material are solely those of the author and/or Econoday Inc. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.