")

Inflation remains a hot topic among investors, policy makers, and voters. While there is not a great deal that policy makers (fiscal or monetary) can do in the short term to control inflation (today’s announcements of coordinated releases from strategic oil reserves are mostly a signaling action), there are steps that can be taken on a longer horizon. Monetary policy has historically been the primary lever used to try to manage inflation, though it has arguably been less effective in recent years as it has run into the “zero lower bound” (ZLB) with short-term interest rates. Fiscal policy is likely a more potent lever but historically has not been used as such.

Higher reported inflation in the US recently has caused expectations of monetary policy tightening by the Federal Reserve to grow. The Fed has already announced that it will begin tapering its heavy bond buying program by $15 billion per month, comprised of $10 billion monthly reductions in Treasury bond purchases and $5 billion/month reductions in mortgage-backed bond purchases. At that pace, the bond buying program would come to an end around mid-year 2022. Consequently, investors are now starting to price in the potential for interest rate increases starting in the summer or fall of next year.

The question for the Fed and investors is whether the current high inflation readings will persist on a longer-term basis, or if inflation will revert back to earlier moderate levels once the COVID-related supply chain disruptions are mitigated. Institutional investors can make such a bet explicitly, using zero-coupon inflation swaps, and thus we can see what “the market” is expecting based on the prices of those instruments. Inflation swaps pay the owner a return equal to the increase in the US Consumer Price Index (CPI) over the term of the agreement (which is unknown when the swap starts, and is thus called the ”floating” part), in exchange for a fixed interest rate on the notional amount of the swap.

Right now, for example, the 5-year inflation swap is trading at a rate of 3.17%. This means that investors are willing to pay 3.17% in annual interest in order to receive a payment equal to the CPI inflation rate over the next five years. So on a $1 million notional amount, the buyer would pay about $31,700 per year in interest, or $158,500 total over five years. At the end of the five years, she would receive a cash payment equal to the total increase in the CPI. If the CPI were to increase at an average rate of, say, 4% per year, the cash payment would be roughly $200,000 (5yrs X 4% ~ 20%), leaving a net profit to the buyer (of about $41,500). If the CPI increased by less than 3.17% per year (say 2.5%), then the buyer would have a net loss after accounting for the interest paid. Thus the interest rate on the inflation swap is the market’s current expectation of the CPI inflation rate over the term of the swap.

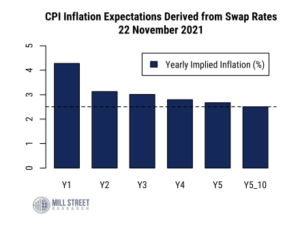

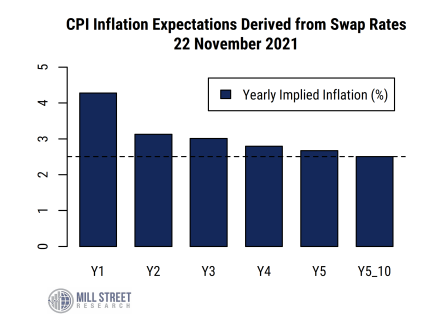

Swaps can be created for many different terms, so we can use the “yield curve” (current yields for various swap durations) on inflation swaps to extrapolate what investors expect for inflation in future years. The chart below shows our calculations for the market’s implicit inflation expectations for each of the next five years (roughly 2022 through 2026), and the longer-term average rate expected over the five years starting five years from now (roughly 2027-2032).

The horizontal dashed line represents an estimate of the Fed’s notional inflation target for the CPI. It is based on their 2% target for the Personal Consumption Expenditures (PCE) price index, which tends to run about 0.5% per year less than the CPI (for various technical reasons). So a 2.5% CPI rate (which would typically equal a PCE inflation rate of 2%) would likely be viewed as near the Fed’s target.

Source: Mill Street Research, Bloomberg

The market clearly seems to view inflation as likely to be high in the next year or two, and then return back to more moderate levels close to the Fed’s presumed inflation target. That is, investors seem to still view above-target inflation as a transitory event tied to COVID, stimulus, and supply chain disruptions, which will moderate back to normal levels within 2-3 years. Of course, not everyone agrees on the definition of “transitory”, but in economic cycle terms, the market’s elevated inflation expectations can be viewed as more transitory than structural.

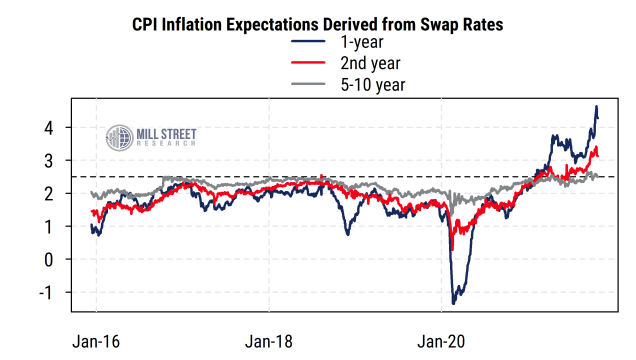

Notably, the current pattern of inflation expectations (higher now, lower later) is the reverse of the pattern we have seen for most of the last few years (and in fact longer than that), as shown in the chart below.

Source: Mill Street Research, Bloomberg

Until this year, near-term inflation expectations (red and blue lines) were mostly below the longer-term readings (grey line), suggesting that investors saw inflation as being low but likely to revert higher (but never very high). This reversal in the pattern highlights the extraordinary nature of the recent economic and policy activities driven by COVID and its related effects. The fact that the longer-term expectations (grey line) remain near levels often seen pre-COVID and near the Fed’s presumed inflation target suggests that inflation expectations are still “anchored” to moderate levels on a longer-term basis.

The bottom line for now is that while investors have increased their expectations of near-term inflation, they continue to expect inflation to moderate and return to near the Fed’s target in the next couple of years. Thus the Fed is likely to view this as a sign that longer-term inflation expectations remain under control and therefore aggressive monetary tightening is not likely to be necessary.

The markets have moved up their expectations for the timing of the first rate hike (now around June 2022) but still only expect short-term policy rates to get to around 1.2% five years from now, in line with the 1.3% rate on the five-year Treasury note. This would be far less cumulative tightening than in previous cycles, and would keep interest rates below the expected inflation rate, i.e,. negative real rates are expected to continue longer-term.

—

Originally Posted on November 23, 2021 – Inflation Expectations: Markets Showing More Worry Now, Less Worry Later

Disclosure: Mill Street Research

Source for data and statistics: Mill Street Research, FactSet, Bloomberg

This report is not intended to provide investment advice. This report does not constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdiction where such offer or solicitation would be prohibited. Past performance is not a guarantee of future results, and no representation or warranty, express or implied, is made regarding future performance of any security mentioned in this report.

All information, opinions and statistical data contained in this report were obtained or derived from public sources believed to be reliable, but Mill Street does not represent that any such information, opinion or statistical data is accurate or complete. All estimates, opinions and recommendations expressed herein constitute judgments as of the date of this report and are subject to change without notice.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Mill Street Research and is being posted with its permission. The views expressed in this material are solely those of the author and/or Mill Street Research and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.