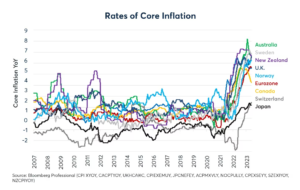

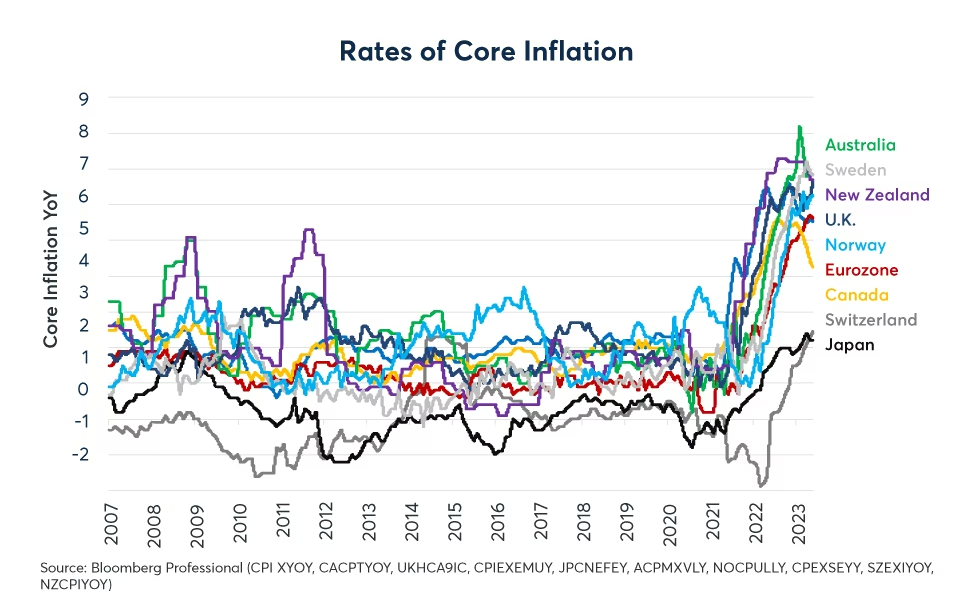

The past two years have been marked by two major global trends: 1) soaring inflation across nearly every major economy outside of China (Figure 1), and 2) a significant rise in interest rates in every major economy except China and Japan (Figure 2). When it comes to the degree of tightening monetary policy, however, there are subtle but important divergences occurring among central banks. Some of them have moved much more aggressively than others to contain inflation.

Figure 1: Core inflation has soared across OECD nations and may have crested in many nations

Figure 2: Most central banks outside of China and Japan have sharply raised short-term rates

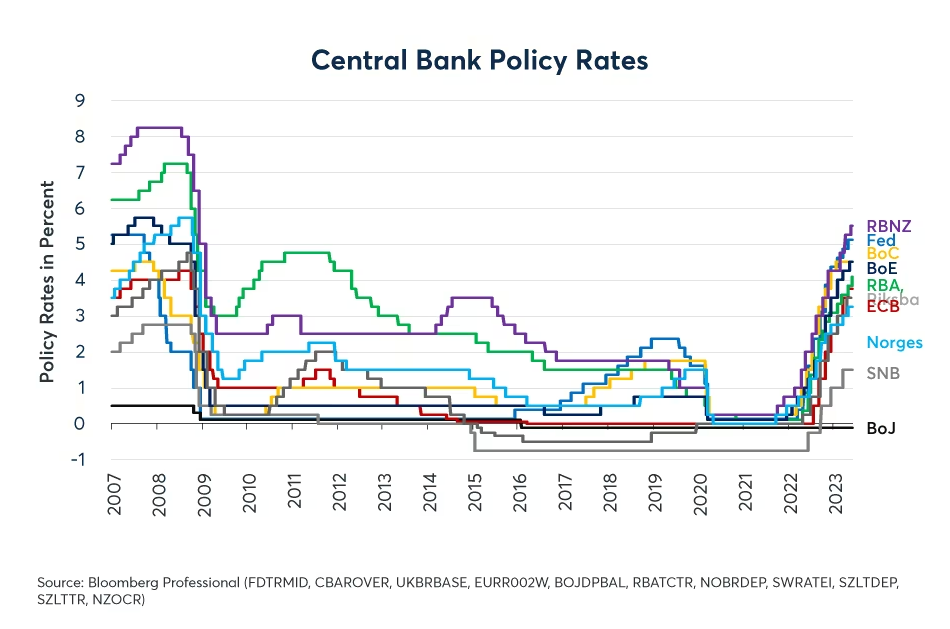

Notably, the Bank of Canada (BoC) has raised rates above its core (trimmed mean) inflation rate, and has become the first major central bank to pause its monetary tightening. The U.S. Federal Reserve (Fed) and Swiss National Bank (SNB) raised rates to nearly core inflation levels. Most other central banks maintain policy rates that are, for the moment, far below core inflation. In places like Australia, Norway and Sweden, policy rates are more than 3% below core inflation. In the U.K. and Japan, they are between 2% and 3% below core inflation, while in the eurozone and New Zealand, they are 1% to2% below core inflation. As such, much of the world still has negative real rates, where real rates are defined as the central bank’s policy rate less core inflation (Figure 3). Definitions of core inflation vary from one country to another but they all exclude the most volatile items, usually food and energy prices.

Figure 3: Real rates remain negative in most developed economies

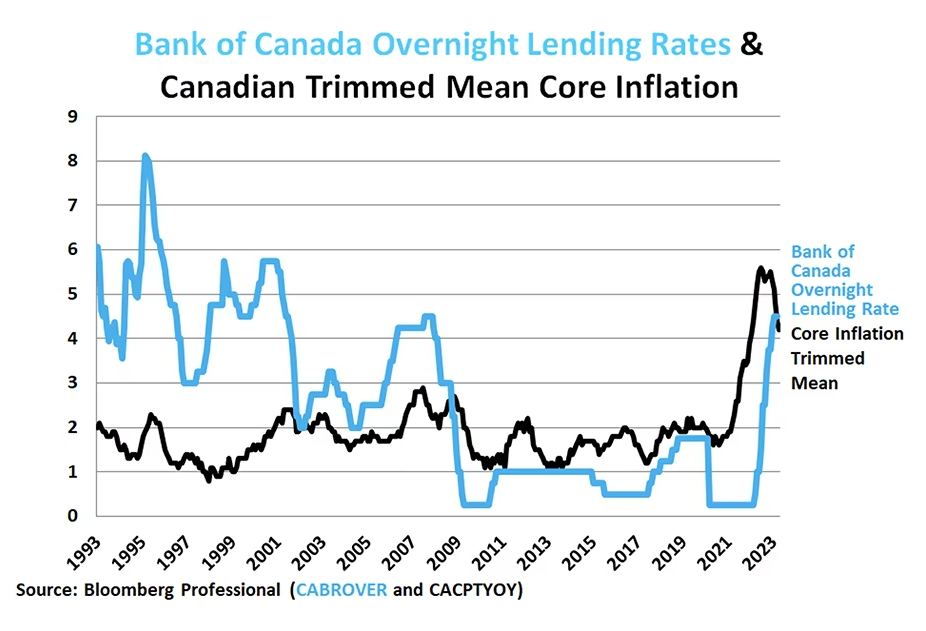

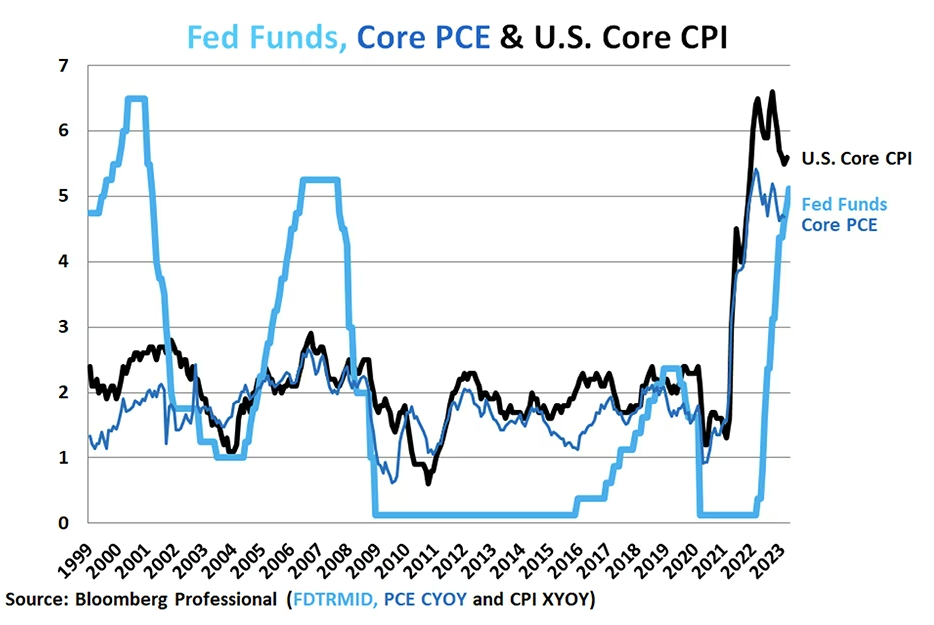

Core inflation may have crested earlier and may be receding faster in places where central banks have raised rated closer to being positive in real terms. Take Canada and the U.S. as examples. Both the BoC and the Fed have raised rates roughly to the level of core inflation and in both countries core inflation has been on a steady, if slow, path of decline (Figures 4 and 5).

Figure 4: Canadian inflation has dipped significantly and is now below BoC policy rate

Figure 5: The Fed has raised rates roughly to the level of the two key measures of core inflation

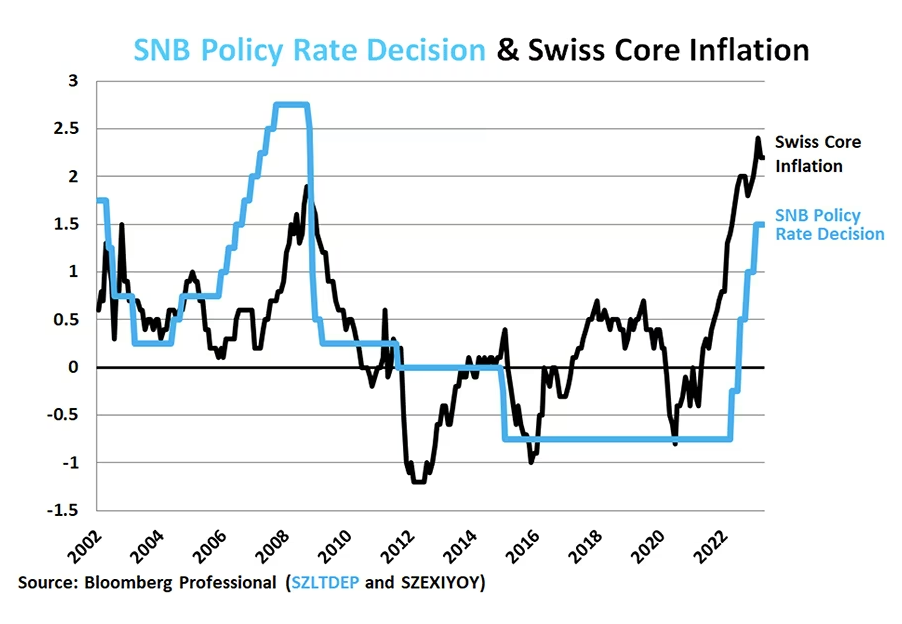

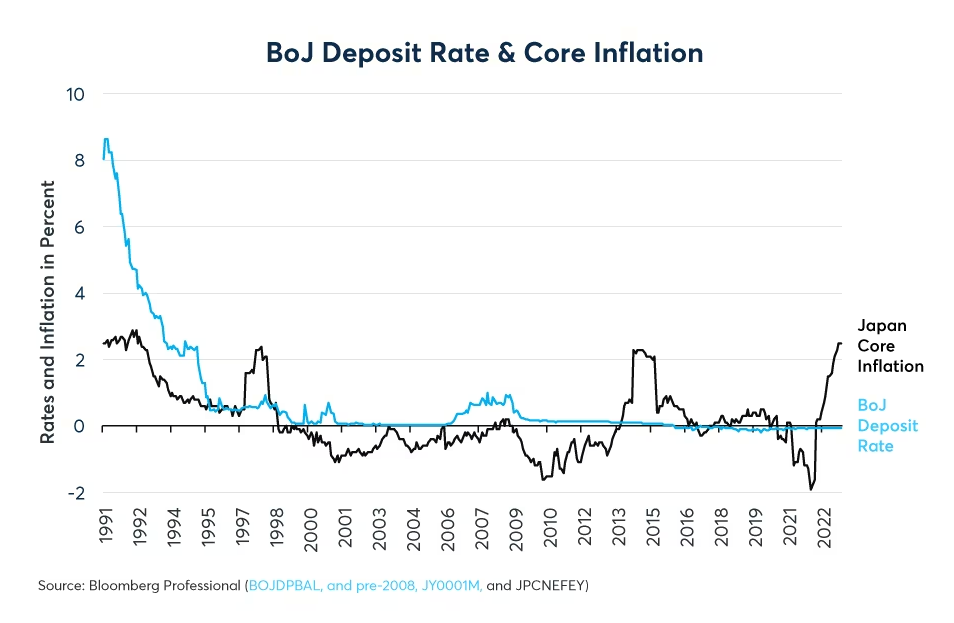

Then there are countries like Switzerland and Japan where inflation had been far below target before the pandemic. In these two nations, inflation has risen but only up to levels that are broadly consistent with the Swiss National Bank (SNB) and the Bank of Japan’s (BoJ’s) policy mandates. These two central banks may be content to see inflation finally achieving positive levels after many years of deflation and may not be eager to raise rates close to the level of core inflation – or in Japan’s case to raise interest rates at all. They may perceive risks as being evenly balanced. On the one hand, inflation could continue to rise and eventually achieve undesirable levels, a risk highlighted by the recent sharp fall in the yen. On the other hand, if they act too aggressively to contain inflation, they could find themselves back in the deflationary situation that they have struggled with for so long to overcome (Figures 6 and 7).

Figure 6: The SNB has tightened policy somewhat but may be satisfied with 2% core inflation

Figure 7: The BoJ may be rejoicing that decades of deflation have finally ended

Unlike in Switzerland or Japan, inflation in the U.K., the eurozone, Sweden and Australia has risen to undesirable levels. However, their central banks appear to have specific concerns that are preventing them from raising rates as close to core inflation as their peers in Canada and the U.S.

In the eurozone, the European Central Bank (ECB) may be concerned that raising rates too vigorously could reignite the eurozone debt crisis. The eurozone is unique in that a single central bank sets monetary policy for multiple countries. As a result, the ECB is not privileged to purchase the debt of one member nation over that of another, and the eurozone government debt market acts more like a municipal bond market than a standard sovereign bond market.

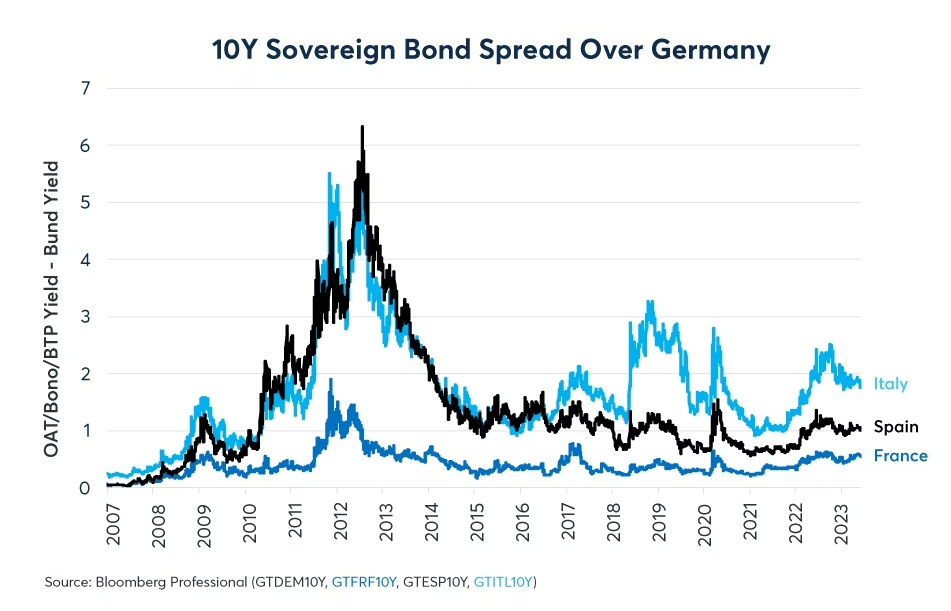

In 2012, then ECB President Mario Draghi pledged to do “whatever it takes” to keep the eurozone together, in large part because inflation was running at roughly half the ECB’s 2% target. This meant that he could cut rates to zero and ramp up an ambitious quantitative easing program with the idea of compressing the sovereign spreads within the eurozone. And it worked. Yields on Spanish and Italian debt came back down more closely in line with that of German debt, preventing a breakdown of the eurozone (Figure 8).

Figure 8: Mario Draghi did “whatever it takes” to save the Eurozone in 2012

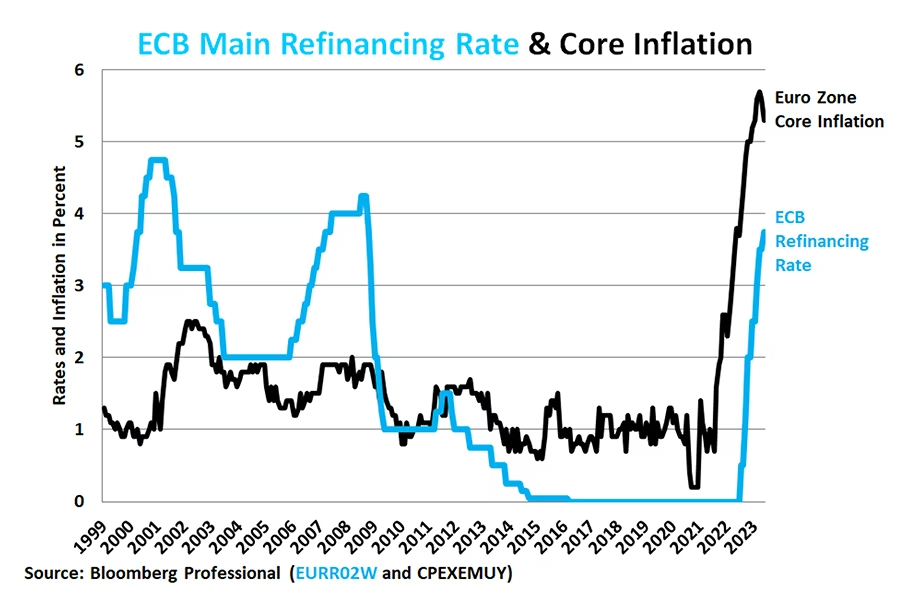

Current ECB President Christine Lagarde has no such option. Core inflation is now running over 5%. The ECB has been raising rates and shrinking its balance sheet. One major risk could be that intra-European bond spreads widen again, potentially triggering a second eurozone debt crisis – but one that would be much harder to grapple with than the previous one, which took place in the context of low inflation. As such, the ECB has been cautious about raising rates by as much as the Fed. However, there is an additional risk: if the ECB doesn’t do enough to tackle inflation today, the central bank may face an even worse problem in the future. Indeed, eurozone core inflation has not been subsiding as much or for as long as core inflation in Canada or in the U.S. (Figure 9).

Figure 9: Fears of a second Eurozone debt crisis may have slowed the ECB’s hand

Australia and the U.K. face a different set of circumstances. In both places the large majority of mortgage holders are on variable rates. Even what passes for “fixed term” mortgages in Australia and in the U.K. reset every two to five years.

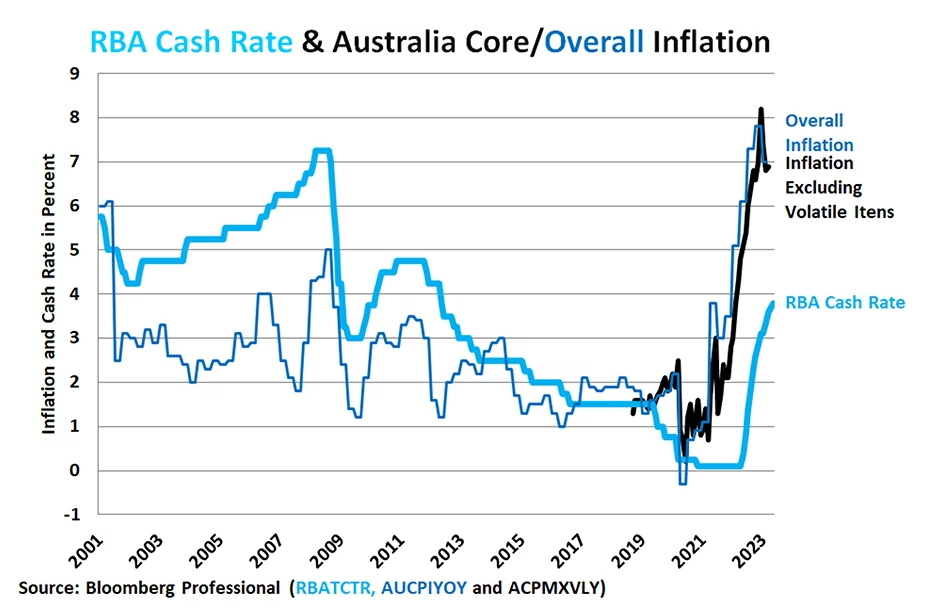

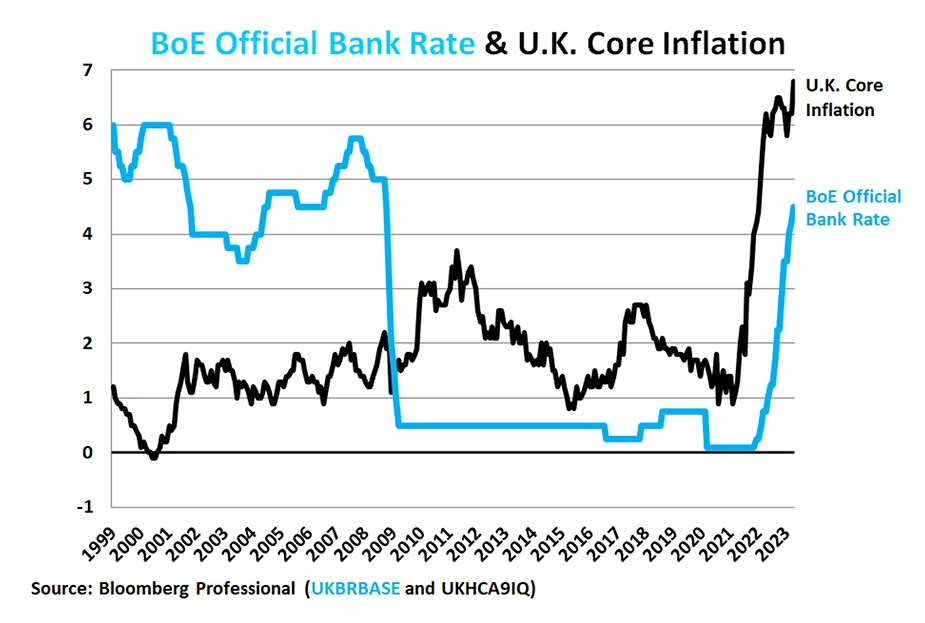

In Australia, this issue is especially acute given the unusually high level of household debt in the country and the fact that many people took out mortgages while the Reserve Bank of Australia (RBA) was engaging in yield curve control during the pandemic. When the yield curve control ended, it set up a potential “mortgage cliff” – a series of dates at which large numbers of mortgages would begin to reset at much higher rates. Moreover, both Australia and the U.K. have highly valued real estate markets and both have seen the economic fallout from collapsing real estate prices in places like Japan in the 1990s and the U.S., Spain and Ireland from 2007 to 2010. So, both central banks have their policy rates far below inflation.

While keeping policy rates far below inflation may prevent, or at least stave off a reckoning in the real estate market, it risks letting inflation continue to rise precipitously. In April, U.K. core inflation jumped from 6.2% to 6.8%, and Australia’s core inflation rate close to 7% (Figure 10 and 11).

Figure 10: The RBA’s policy rate remains low compared to core inflation

Figure 11: The BoE’s slow pace of raising rates may be fueling inflation

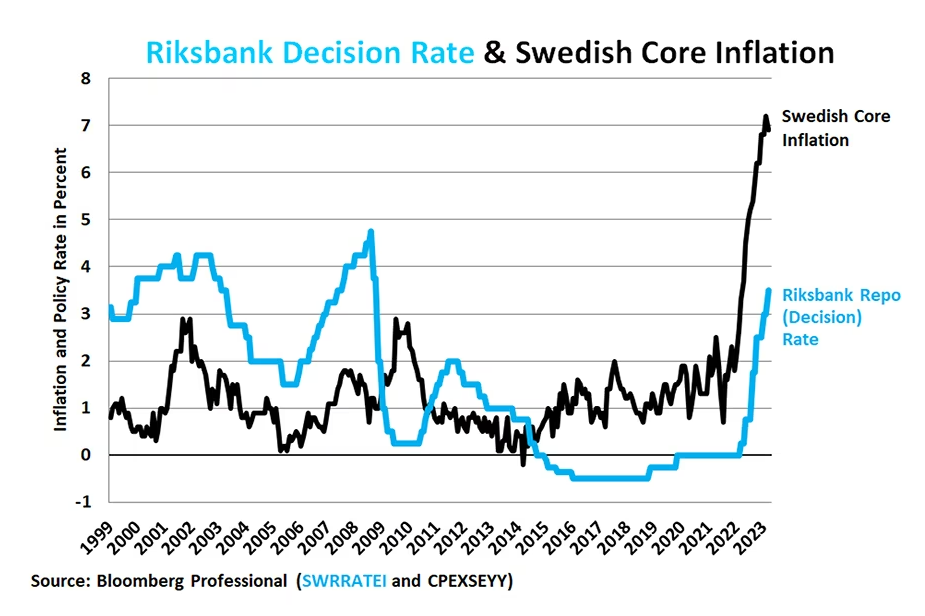

It’s a similar story in Sweden where the Riksbank, confronted with extraordinarily high levels of household debt – mostly mortgages—and extremely high real estate prices, might be concerned over financial stability from the consequences of raising rates too quickly. Memories of an economic and banking crisis in the early 1990s might also be slowing any move toward tighter policy. Like Australia and the U.K., Sweden’s core inflation rate is running close to 7% while the Riksbank policy rate is around half that level. Moreover, like the U.K. and Australia, inflation is showing few signs of subsiding outside of energy prices (Figure 12).

Figure 12: Sweden’s policy rate is half the level of inflation at 7%.

Bottom line

By raising rates comparatively quickly, the Fed and may be having more success at containing inflation than many of its peers. Other central banks have taken a slower approach and may have legitimate fears regarding financial stability if they did put real rates at the same levels of Canada and the U.S. That said, the choice to act less decisively against inflation may be generating higher inflation that could lead to even more painful choices in the future.

—

Originally Posted June 8, 2023 – Monetary Policies Diverge as Inflation Poses Unique Challenges, Benefits

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the author and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Forex

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.