")

As Q3 ends and with reporting season set to begin in the coming weeks, we can update the current consensus earnings outlooks for Q3 and Q4 as well as calendar year 2021 and 2022 for the S&P 500. Earnings should be up a lot from last year, but uncertainty among analysts remains quite high.

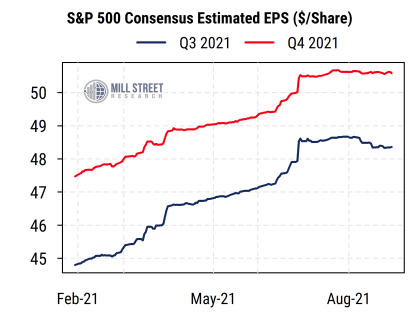

For Q3, S&P 500 earnings are expected to be up 28% from a year ago according to Factset, another big percentage gain. That figure is higher than it was at the start of the quarter (it was 24% on June 30th) but has been stable since July and down marginally since the end of August. So the pace of gains in aggregate index earnings has eased, but estimates are still rising modestly on balance.

Operating EPS expectations for Q3 of $48.35 per share are higher than all pre-COVID levels but expected to be slightly below Q2’s record reading of $52.36.

Despite the recent concerns about cost pressures, natural disasters, and China’s weakness, consensus continues to call for strong double-digit earnings growth in Q4 as well, with the current estimate of $50.62 expected to be up 22% from Q4 2020. That figure is unchanged from a month ago.

Source: Mill Street Research, Factset

The Q3 earnings reports and associated commentary/guidance will likely be key in determining whether analysts need to be more cautious in their outlooks for Q4 and 2022 or not.

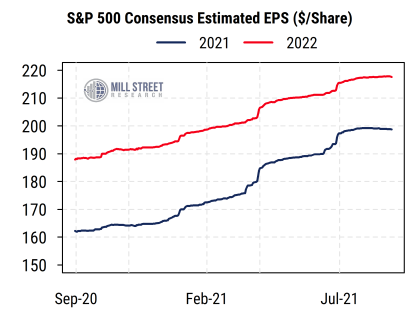

The current consensus S&P 500 EPS for calendar 2021 is now $198.76 (giving a 2021 P/E of 21.9 for the S&P 500), while the consensus for 2022 is $217.52 (P/E of 20.0).

The 2021 figure is down slightly from one month ago, but still much higher than it was at the start of Q3. The 2022 figure is up slightly from a month ago and also well above the level at the start of Q3.

Source: Mill Street Research, Factset

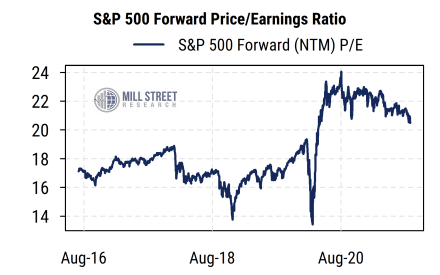

The recent pullback in stock prices has brought the forward (next 12 month, NTM) P/E for the S&P 500 down somewhat further, now just above 20 (or an earnings yield of about 5%). This is still above pre-COVID levels, but significantly below the levels since a year ago. This 5% earnings yield still compares favorably with the 10-year Treasury yield of about 1.5%.

Source: Mill Street Research, Factset

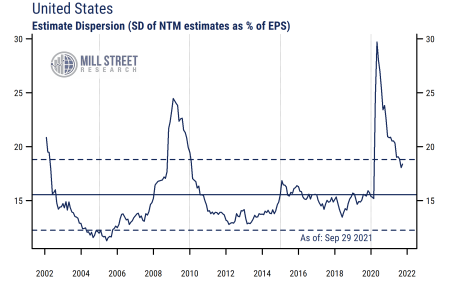

The other key point, which is perhaps not surprising but bears mentioning, is that uncertainty about corporate earnings among analysts remains quite high relative to historical norms. The range of estimates around the mean (consensus) among US stocks is still well above the normal range seen outside of recessionary periods.

Source: Mill Street Research, Factset

This suggests that even though GDP and earnings have been rebounding strongly recently, all of the uncertainty about policy, supply chains, the path of COVID and vaccinations, extreme weather, etc. is still provoking a lot of disagreement among analysts as to how much companies will make over the next year.

—

Originally Posted on September 30, 2021 – Q3 Earnings Should Be Good, But Uncertainty Remains High

Disclosure: Mill Street Research

Source for data and statistics: Mill Street Research, FactSet, Bloomberg

This report is not intended to provide investment advice. This report does not constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdiction where such offer or solicitation would be prohibited. Past performance is not a guarantee of future results, and no representation or warranty, express or implied, is made regarding future performance of any security mentioned in this report.

All information, opinions and statistical data contained in this report were obtained or derived from public sources believed to be reliable, but Mill Street does not represent that any such information, opinion or statistical data is accurate or complete. All estimates, opinions and recommendations expressed herein constitute judgments as of the date of this report and are subject to change without notice.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Mill Street Research and is being posted with its permission. The views expressed in this material are solely those of the author and/or Mill Street Research and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.