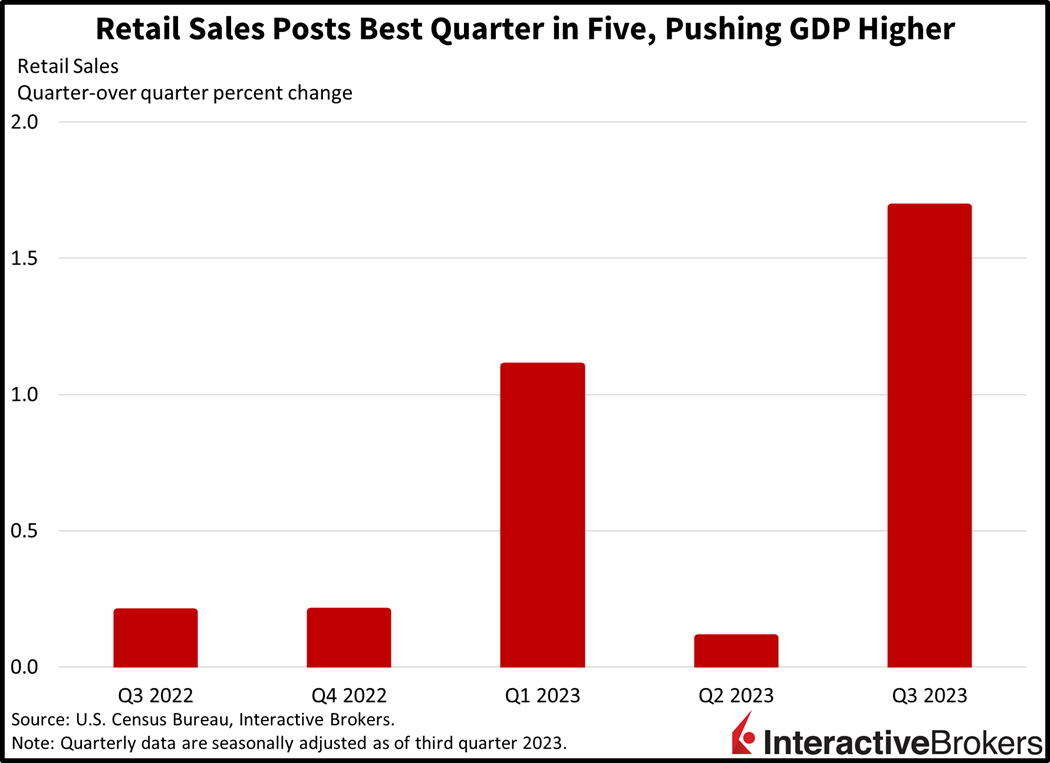

Equities have pared earlier losses after heightened geopolitical tensions in the Middle East and Far East generated risk-off sentiments. A double beat on retail sales, however, led to climbing bond yields which are approaching year-to-date highs. The strong retail sales data released this morning from the Commerce Department points to a giant third quarter GDP print, which is scheduled for release next week and is likely to keep the Federal Reserve a focus point for investors.

Cash registers finished the third quarter with a bang as September retail sales grew 0.7%, more than double the 0.3% rate forecasted by the consensus. While producing a double beat, sales slowed from the previous month’s 0.8%, but today’s strong report solidifies a robust GDP number next Thursday, October 26. Impressively, third quarter sales were the strongest in the past five quarters.

Miscellaneous Retailers Lead Sales

The following categories with the noted retail increases led sales:

- Miscellaneous retailers, 3%

- Ecommerce, 1.1%

- Automobile and parts dealerships, 1%

- Restaurants and drinking parlors, 0.9%

- Gasoline stations, 0.9%

- Health and personal care stores, 0.8%

Grocery stores and general merchandise shops notched modest gains of 0.4% while furniture showrooms and sporting goods retailers were flat month-over-month (m/m). Vendors specializing in apparel, electronics and building materials weighed on results with sales slipping 0.8%, 0.8% and 0.2%, respectively.

Homebuilders Sing the Blues

The outlook for building materials isn’t rosy either, with today’s Homebuilder Sentiment report plunging as the pressures of elevated rates, towering prices and narrower credit availability weigh upon the industry. The October figure dropped to 40, the third consecutive decline while coming in weaker than projections calling for an unchanged reading of 44. Homebuilders reported declines in their present and future outlooks while witnessing another drop in buyer traffic.

Manufacturing Picks Up, But Only Marginally

Industrial production notched a modest improvement from the previous month as the effects of the auto strikes have yet to make their way into the data. Industrial production rose 0.3% m/m in September, higher than estimates projecting an unchanged reading of 0%. On a year-over-year (y/y) basis, industrial production rose 0.1%, slightly lower than the 0.2% growth rate from August.

Equities Recoup Earlier Losses

Markets were generally selling off although stocks have come back and are now positive. Bonds are getting clobbered, with hot economic data concerning market players about the potential for a tougher Fed. The 2-year Treasury yield just matched its year-to-date high at 5.203% while the 10-year is 3 basis points (bps) away from its yearly high. The 2- and 10-year maturities are up 10 and 14 bps each to 5.203% and 4.855%. The dollar is roughly unchanged though, as it gains against the yuan, yen, pound sterling and Canadian dollar while losing value relative to the franc, euro and Aussie dollar. Major stock indices were mostly down but are now higher with the Nasdaq Composite, S&P 500 and Dow Jones Industrial indices up 0.3%, 0.3% and 0.1% while the small-cap Russell 2000 gains an impressive 1.8%. Sectoral breadth is positive, with the technology and utilities sectors the only ones losing value thus far in the session. WTI crude oil is down $1.00 or 1.1% to $86.00 per barrel on optimism about a potential handshake between Washington and Caracas that will bring additional barrels online from the country.

Uncertainty Persists at Home and Abroad

Meanwhile, the following conflicts in geopolitics, Washington, D.C., and Detroit continue to create uncertainty about a broad range of matters:

- In the Middle East, Israel’s attacks on the Gaza Strip in response to attacks from Hamas and the country’s preparation for a ground invasion of the region is swelling fears that the conflict may expand to neighboring countries and threaten the production and exportation of energy commodities. President Joe Biden is scheduled to meet with Israeli leaders tomorrow followed by meetings with Palestinian and Egyptian leaders in Jordan to discuss a potential solution to the crisis.

- In other geopolitical developments, the Biden Administration has announced plans to close loopholes that have allowed U.S. semiconductor chip manufacturers to circumvent bans on exporting advanced chip and manufacturing equipment to China. The new rules are expected to supplement restrictions imposed last October.

- In Washington, Representative Jim Jordan of Ohio’s 4th district, who is considered to be among the more conservative House Republicans, is inching closer to becoming House Speaker as the November 17 deadline for elected officials to pass a budget approaches. Without a House Speaker, the lower chamber of Congress is in disarray. Jordan is believed to have won the support of certain Republican moderates who previously said they wouldn’t back him, nevertheless, his party’s slim majority only allows him to lose a small number of Republican votes to win the position as all Democrats will likely vote against. As one of the more conservative House members and a deficit hawk, Jordan is believed to be more willing to allow a government shutdown if Democrats don’t agree to significant spending cuts.

- As the United Auto Workers’ picket lines at the nation’s largest three automakers continue, Detroit casino workers began striking today as well. The actions involve approximately 3,700 union members at three casinos in the Detroit area. Auto manufacturers, meanwhile, are continuing to layoff workers at plants that have been shut due to the ongoing strikes. Approximately 5,000 workers have been furloughed. In a win for the UAW, General Motors recently agreed to use union workers in its new electric vehicle plants. Approximately 20% of the union’s members work on engines and transmissions that would be phased out as EV adoption increases. Otherwise, the UAW and auto manufacturers haven’t provided any indication of how long the turmoil may continue.

Corporations Navigate a Challenging Macroenvironment

- Goldman Sachs reported a 33% y/y profit decline this morning as it strategically exits the consumer lending business. The investment bank was hurt by write-downs as it sold some of its investments related to main street lending and wealth management. A modest resumption in underwriting and initial public offerings alongside strong fixed income, currency and commodities trading offset some of the weakness, however, with the financial institution reporting a net profit of $2.06 billion or $5.47 per share, beating the median estimate of $5.31. CEO David Solomon is optimistic about the bank’s future as he steers the institution toward its traditionally reliable focuses of investment banking and trading while growing the wealth management business.

- Bank of America, meanwhile, sported its highest third quarter earnings in recent memory as fixed-income and equity trading buoyed profits. The financial institution earned $7.8 billion in net profit or $0.90 per share, better than the $0.81 projected. The bank’s non-interest expenses rose 3.5% y/y, however, as persistent inflation and wage gains mounted. CEO Brian Moynihan appeared satisfied with the bank’s account additions across all business lines while expressing caution of a slowing consumer.

- Among consumer-focused companies, Albertsons Companies, which operates grocery stores, pharmacies and gasoline retailers, reported a 2.9% y/y identical sales increase for its fiscal second quarter ended September 9. Its adjusted net earnings per share (EPS) of $0.63 exceeded the $0.56 consensus expectation. Revenues of $18.3 billion matched the consensus expectation. Its identical sales benefited from increased pharmacy sales, 19% growth in digital sales and price inflation. The company expects food inflation to ease but says it will still face broader headline inflation.

- Drug maker Johnson and Johnson, which spun off its consumer health division in August, reported adjusted EPS of $2.66, beating the analyst consensus expectation of $2.52. Its revenues of $21.35 billion also exceeded the consensus expectation, which was $21.04 billion. Its income of $4.31 billion matched the year ago quarter, but on a per share basis it increased from $1.62 to $1.69. The company said Covid-19 vaccine sales have been weakening but Darzalex, which is used for multiple myeloma; Erleada, which treats prostate cancer, and Stelara, which treats various immune-mediated inflammatory diseases, were strong. Johnson & Johnson also said 2023 sales will range from $83.6 billion to $84 billion, up from its August guidance of $83.2 billion to $84 billion.

Partyers Rock Out as Hot Data Keeps Rolling In

As the Fed takes a wait-and-see approach to assess the impact of its past rate hikes, October is dishing out hotter-than-expected data for September. Payrolls, the Consumer Price Index, the Producer Price Index and retail sales have all exceeded expectations. With GDP forecasted to come in at 4.1% next week ahead of an important Fed decision on November 1 regarding its fed funds interest rate, investors appear quite exuberant, having placed a low 7% odds of a 25-bp hike. Meanwhile, the consumer party is continuing with Taylor Swift’s concert film generating a record $92.8 million in sales during its three-day rollout, making it the highest ever grossing concert film and the second-best domestic movie opening to occur in October.

Visit Traders’ Academy to Learn More About Economic Indicators.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.