Corporate earnings are helping stocks scale the wall of worry following last week’s market debacle as investor sentiment rebounds based on expectations that the worst of the Middle East tension is behind us. Today’s gains are adding to yesterday’s bullish momentum with a combination of economic data such as the flash Purchasing Managers’ Indices (PMIs) and expectations for moderating second-quarter economic growth causing investors to adjust their positions as the path toward disinflation widens slightly. Lurking in the background, however, is a $69 billion auction for 2-year notes this afternoon and a GDP report this Thursday that is expected to depict blockbuster first-quarter growth.

Lofty Prices and Rates Weaken Demand

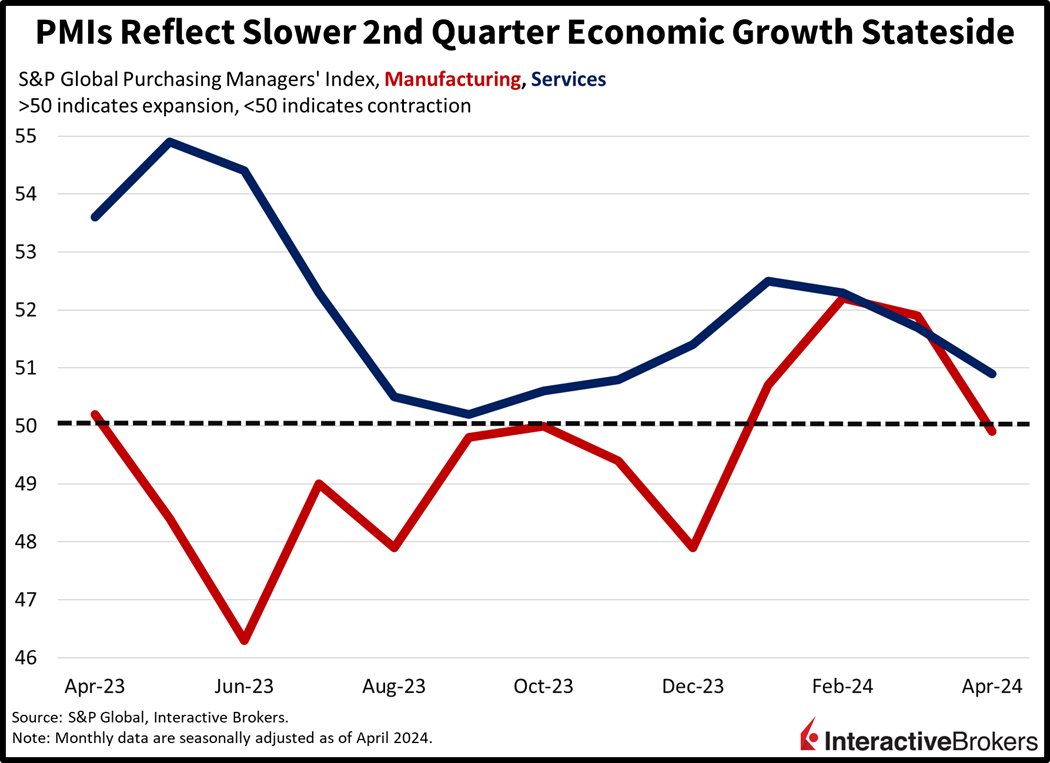

US economic growth slowed in April, according to the flash PMIs from S&P Global. The manufacturing sector contracted for the first time this year, following three consecutive quarters of expansion as consumers and businesses balked at lofty prices while feeling satisfied with their current inventories. Meanwhile, demand for services was the weakest of the year with firms perceiving that elevated interest rates and inflationary pressures pushed customers away. Both manufacturers and servicers reduced headcounts in efforts to preserve margins against the backdrop of questionable revenue growth. But while input costs rose sharply, price increases for customers slowed across both sectors, opening the door to potential disinflation in coming months if demand continues to slow.

April’s Manufacturing PMI of 49.9 was a whisker away from the expansion-contraction threshold of 50 and much worse than the consensus estimate of 52 as well as March’s 51.9. The Services PMI remained in expansionary territory, coming in at 50.9, but also beneath the median projection of 52 and March’s 51.7. Slowing demand and labor force softening is certainly needed to slow inflationary pressures. A continuation of these trends will help lower interest rates and keep the economic expansion going amidst decelerating price pressures.

Eurozone Outlook Brightens

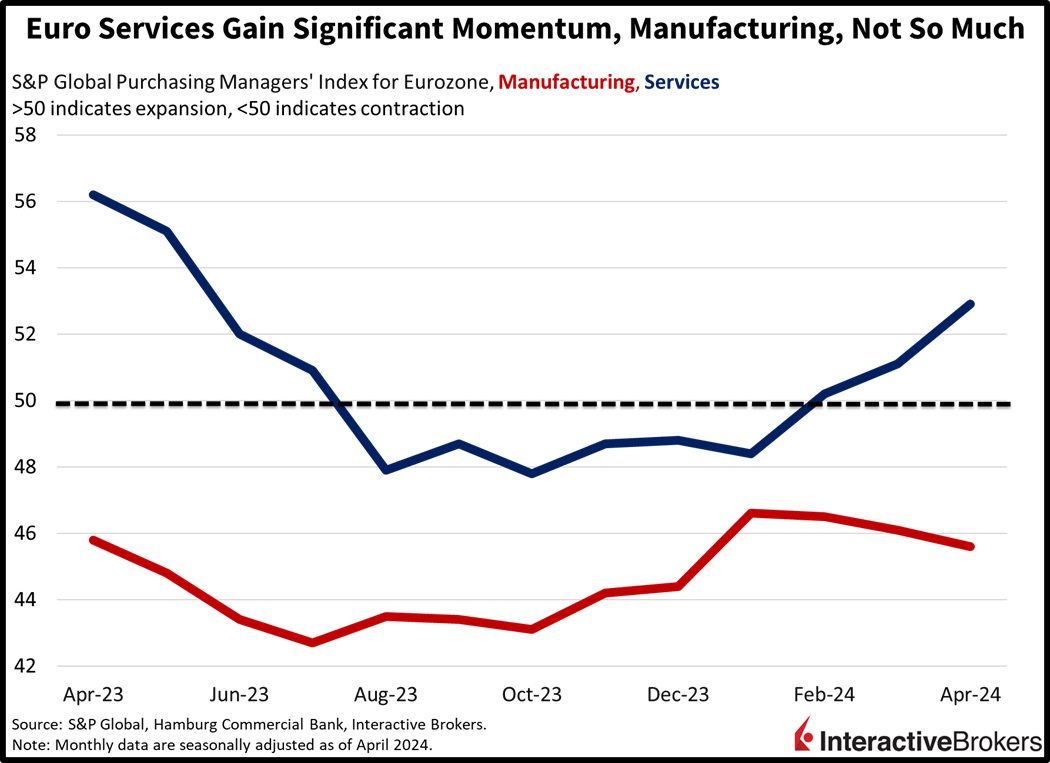

Across the Atlantic, eurozone economic growth accelerated sharply as the region gears up for the beginning of the European Central Bank’s easing cycle. Most nations performed well, but the bifurcation across manufacturing and services remained. The Services PMI accelerated strongly to 52.9, much higher than the 51.8 forecast and March’s 51.5. Headcounts, output and prices rose strongly, as loftier wage bills, robust demand and geopolitical pressures pushed up figures. Manufacturing remained in the tombs though, achieving a miserable score of 45.6, worse than the anticipated 46.5 and the 46.1 from the previous period. Supply chains did improve significantly though, as Red Sea disruptions appear increasingly tempered. Optimism was reported by executives in both sectors as firms look forward to rate cuts this June. The hope, however, is that this reacceleration in economic growth occurs alongside sustainable price increases, a challenging needle to thread.

Homebuyers Flock to New Construction

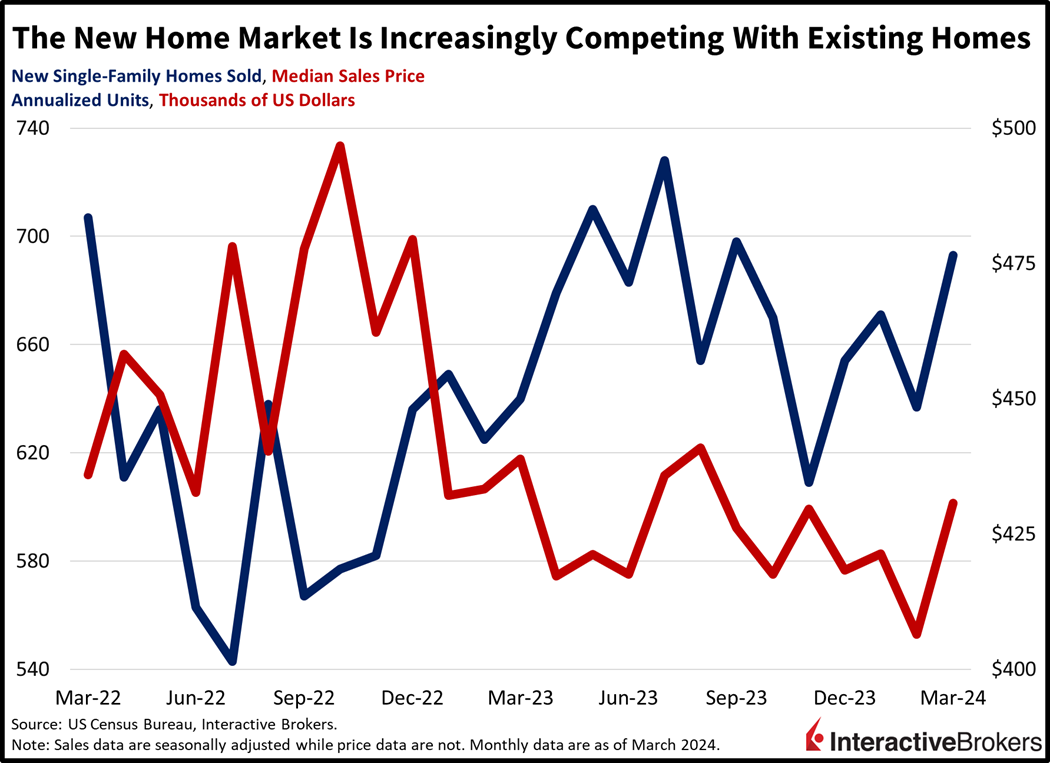

Homebuyers jumped to the new home market last month, with the pace of transactions rising at the fastest clip since last September. New home sales rose 8.8% month over month (m/m) to 693,000 seasonally adjusted annualized units in March, better than the 668,000 expected and the 637,000 from February. Transactions performed well in all regions with the Northeast, West, South and Midwest experiencing m/m sales increases of 27.8%, 8.6%, 7.7% and 5.3%. Prices also jumped to the highest level since last August, with the median cost of $430,700 in March increasing from $406,500 m/m. Inventories declined to 8.3 months at the current pace of sales, a sharp m/m decline from February’s 8.8 months. Bifurcated conditions between new and existing homes may begin to align this year as prospective existing home sellers compete with homebuilders for transactions, especially as the former cohort grows increasingly impatient awaiting lighter mortgage rates.

Package Delivery Demand Rebounds While GM Posts Strong Sales

Shipping volumes were weak in the first quarter but are improving, and separately, consumers are splurging on new pickup trucks and sport utility vehicles (SUVs). In other sectors, consumers are pushing back on higher beverage and snack prices, while strong air travel and issues at Boeing are supporting demand for after-market aviation products. Those are a few themes from the following earnings releases:

- UPS’ first-quarter earnings exceeded analysts’ expectations despite revenue missing forecasts. The company cut 12,000 jobs in January, which saved $1 billion and helped offset the impact of both declining shipping volumes and higher wages resulting from a new union agreement. The shipping volume declined due to demand returning to more normal levels after soaring during pandemic lockdowns and other measures to reduce the spread of Covid-19. Despite the cost-cutting measures, first-quarter earnings declined 35% year over year (y/y). On a positive note, UPS said shipping volumes increased as the quarter progressed, and it expects conditions to improve in the second half of this year. Its share price climbed approximately 3% in early trading.

- GM’s first-quarter results were highlighted by strong consumer demand for gas-powered pickup trucks and sport-utility vehicles in North America, which contributed to earnings climbing 24% y/y. Both earnings and revenue exceeded the analysts’ expectation. In response to the strong demand, GM raised its earnings guidance from between $8.50 and $9.50 to between $9 to $10 a share. GM CEO Mary Barra wrote in a shareholder letter that consumers have been extremely resilient as interest rates have increased. Markets outside of North America were stronger than the company expected but nevertheless weighed on results with a $106 million loss in China and smaller losses in other international markets. The price of GM shares climbed approximately 5% in early trading.

- PepsiCo’s first-quarter earnings and revenue beat analysts’ expectations. While North America consumers are busy at GM dealerships, some of them are ignoring PepsiCo products in supermarkets, with the company’s beverage unit reporting a 5% decline in sales by volume. More broadly, volume sales declined for Gatorade, Fritos and other products in response to the company raising its prices. Sales were also hurt by the company’s Quaker Foods division recalling products that may have had salmonella poisoning. PepsiCo also said sales among lower-income customers declined. In a related matter, teamsters Local 727 members employed by PepsiCo Beverages North America have voted to authorize a strike if the company fails to reach a contract with the union. The unit employees 800 workers. PepsiCo shares declined approximately 3% this morning.

- GE Aerospace provided upbeat guidance after explaining that Boeing production issues with the 737 Max will delay delivery of the passenger jet to airlines, resulting in sustained demand for parts for older aircraft that will remain in service longer than previously expected. The company, which resulted from splitting GE into separate energy, health care and aviation businesses, said it also expects strong travel volume this year to support demand for its after-market services, such as engines and other aviation products. It now expects total operating profit to range from $6.2 billion to $6.6 billion, up from its earlier guidance of $6 billion to $6.5 billion. Shares of GE Aerospace were up more than 6% in early trading.

Investors Embrace Risk

Risk-on sentiments are buoyant following today’s cooler-than-expected flash PMIs, which may pave the way for disinflation in the coming months. Stocks are up while the dollar and yields are submerging, as traders put July back on the table for the Fed’s first rate cut, but odds continue to favor September as the start of the easing cycle. All major US equity indices are higher with the Russell 2000, Nasdaq Composite, S&P 500 and Dow Jones Industrial indices up 1.5%, 1.3%, 1% and 0.5%. Sectoral breadth is positive with 10 out of 13 sectors up on the session. Leading the charge higher are communication services, technology and industrials; they’re up 1.6%, 1.2% and 1.2%. Meanwhile, materials, energy and consumer staples are lower by 0.8%, 0.2% and 0.1%. Yields are declining, with the 2- and 10-year Treasury maturities trading at 4.94% and 4.59%, 4 and 2 basis points (bps) lighter on the session. Lighter yields and softer inflation expectations are also weighing on the dollar, with its index down 35 bps to 105.78. The greenback is losing ground relative to most of its major developed market counterparts including the euro, pound sterling, yen and Aussie and Canadian dollars. It is gaining versus the yuan though. WTI Crude oil is up 0.9%, or $0.72, to $82.80, as rising probabilities of rate cuts stateside and in the eurozone propel the demand outlook even as supply prospects have improved on the back of simmering geopolitical tensions.

A More Favorable Outlook for Disinflation

As the year has progressed, inflation data has continued to point to the Fed delaying and reducing the number of rate cuts it would enact this year. While last week’s market volatility was driven, in part, by investors repricing equities based on the higher for longer outlook, today’s data is helping alleviate fears of the central bank staying restrictive for too long. On one hand, manufacturing and services PMIs show that both categories are reducing headcounts, an encouraging development that could help ease wage pressures that would otherwise cause businesses to increase their prices. Additionally, overall weakness in both the manufacturing and services PMI points to slowing economic growth and consumers balking at higher prices. While this week’s GDP and PCE reports will shed light on what’s been a powerful first quarter, the second quarter’s momentum will be driven by the sustainability of consumer spending momentum. Throughout this cycle, we’ve seen consumer spending freeze in certain months, only to reaccelerate later. Consumers may be erratic, but the trend remains positive, especially as the propensity to save has disappeared, providing corporates with incremental revenue growth.

Visit Traders’ Academy to Learn More About New Home Sales and Other Economic Indicators.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.

Leave a Reply

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

")

I’m confused. What about the $6 Trillion stimulus from the White House. When will the inflationary effect occur? Next year?