The headwinds of troubled real estate markets in China and the US combined with growing geopolitical risks and challenges associated with monetary policy are adding risks to economic prospects. Nevertheless, bright spots exist, such as the potential for artificial intelligence to enhance productivity, businesses right-sizing headcounts, the accelerating development of alternative energy and China’s growing electric vehicle market. A trend of nearshoring and onshoring is likely to support inflationary pressures, however, as corporations and countries select reliability over profitability. In the interim though, US stock indices have reached new all-time highs, including the S&P 500 benchmark marching north of the pivotal 5,000 level. Yields are cautious though, as an excessive degree of animal spirits incrementally keeps central bankers at bay while propping up price-pressure expectations. Indeed, rates have likely bottomed, with three strong auctions this week and this morning’s favorable downward revisions on the US’s Consumer Price Index failing to bring relief on the yield front.

IMF Expects Below Average Global Growth

The International Monetary Fund (IMF) recently set the stage for lackluster-economic expectations with its 2024 global GDP growth estimate of 3.1%, up only slightly from the organization’s 2.9% estimate in October. The revised rate would equal the estimated expansion for 2023, which is below the average annual growth of 3.8% occurring from 2000 to 2019. The IMF expects headline inflation of 5.8%, down from an estimated 2023 rate of 6.8%. It will allow certain central banks to become accommodative, but high debt levels will cause many countries to reduce fiscal support amidst unclear productivity trends. When central banks turn dovish, the lag of accelerating economic growth after the reduction of interest rates is likely to cause most of the year to feel the brunt of current restrictive policies.

Commercial Real Estate Presents Risks

In the near term, I expect real estate to be a considerable challenge for capital markets and economic stability with China having a surplus of developed properties and banks in the US and other countries struggling with troubled commercial-property loans.

China’s economy is expected to grow 4.6% this year and slow to 4.0% next year after climbing 5.2% in 2023, according to the IMF. Domestically, China’s glut of real estate is a significant headwind with investment in the sector dropping 9.6% last year as construction starts tumbled 20.4% and residential sales dropped 6.0%. Beijing has responded with billions of dollars in funding to lower mortgage rates and other programs to shore up the sector. Meanwhile debt-ridden municipal budgets are feeling the impact of the issue. The success of efforts to revive the sector will ultimately be determined by the willingness of gun-shy banks to provide loans. Meanwhile, a slow global economy that is feeling the strain of tighter monetary policy has crimped demand for Chinese manufacturing, with the country’s exports falling from $3.54 trillion in 2022 to $3.38 trillion last year. In addition, Mexico has recently topped China as the top exporter to the United States, pointing to continued stress on Beijing’s manufacturing orders and pricing power. The reduced pricing power is depicted in the nation’s deflationary trend. On an annualized basis, Goods prices have declined every month since March while overall consumer prices have declined every month since September.

The Far Reach of US Real Estate Troubles

In the US, the saga of regional banks and commercial real estate surfaced again with Moody’s Investor Services slapping New York Community Bank (NYCB) with its lowest possible investment grade rating. During the past few days, shares of NYCB dropped over 60% after the company disclosed that it increased its reserves for faulty commercial real estate loans, cut its dividend and suffered a $252 million net loss in the fourth quarter. The vast majority of commercial real estate loans are provided by regional banks that face the risks of property owners struggling to service debt payments as demand for their office properties weakens due to work-from-home arrangements. Other asset classes within commercial real estate are having problems as well but to lesser extents, as retail and apartment building properties contend with loftier interest rates alongside rising costs for labor, maintenance, insurance, etc. The problem isn’t limited to the US. Just recently, Aozora Bank in Tokyo announced a $221 million charge for bad US commercial real estate loans, resulting in the company generating a loss in 2023. South Korea banks are believed to also have exposure to US commercial real estate and underperforming real estate in Europe. Germany is also feeling the turmoil with Deutsche Bank quadrupling its commercial debt loss provision.

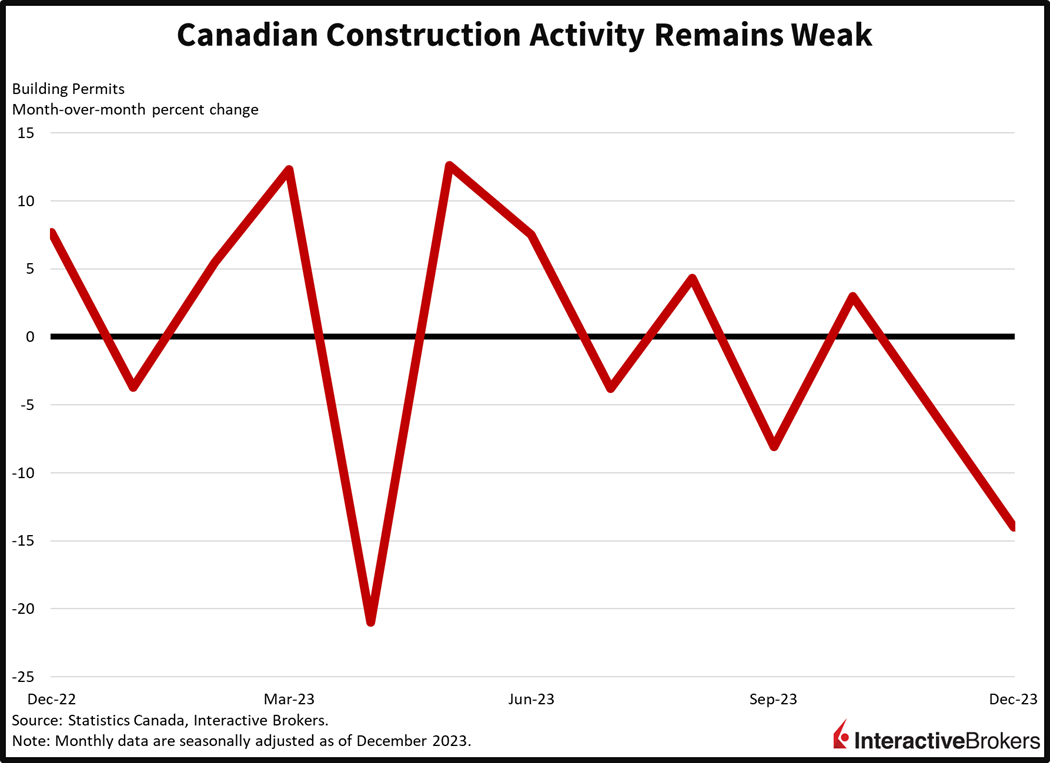

Canada Rate Cuts on Hold

Canada, meanwhile, is dealing with persistent inflation while high interest rates hit the construction industry. New building permits in December dropped 14% from November, missing the expectation for a 1.8% increase. Meanwhile, in the fourth quarter, residential building construction costs increased 0.9%, following a 1.2% increase in the previous quarter. Non-residential building construction costs rose 0.7% in the fourth quarter, following a 1.3% increase in the previous quarter. The broader economy, furthermore, appears strong enough to support additional price pressure with the January Ivey Purchasing Managers Index (PMI) reaching 56.5, its highest level in nine months. A reading above 50 indicates an increase in activity. The country’s central bank this week said it needs to see more data that shows that core inflation, currently at 3.5%, isn’t transitory before it embarks on monetary policy loosening. Indeed, this morning’s employment report saw job gains beat expectations by 22,000 while the unemployment rate dipped to 5.7% while economists were expecting an increase to 5.9%. Wages are also rising at a pace that isn’t conducive to 2% inflation, with today’s average hourly earnings rising 5.3% year over year (y/y).

BOJ Likely to Ease

The Japanese yen weakened following dovish comments from Uchida Shinichi, the Deputy Governor of the Bank of Japan. He indicated that the central bank is not looking to aggressively raise interest rates following a period of negative costs of capital. Shinichi pointed to real rates being significantly negative and monetary conditions highly accommodative, conditions that the BOJ would like to sustain. Japan, unlike other nations, is likely to remain relatively accommodative, with perhaps just a few occasional rate hikes occurring in the future. The position, however, is likely to keep pressure on the yen, as its attractiveness is impaired relative to its major counterparts. Dynamics concerning yield differentials and a stronger dollar as a result may incrementally tilt financial conditions toward the tighter side.

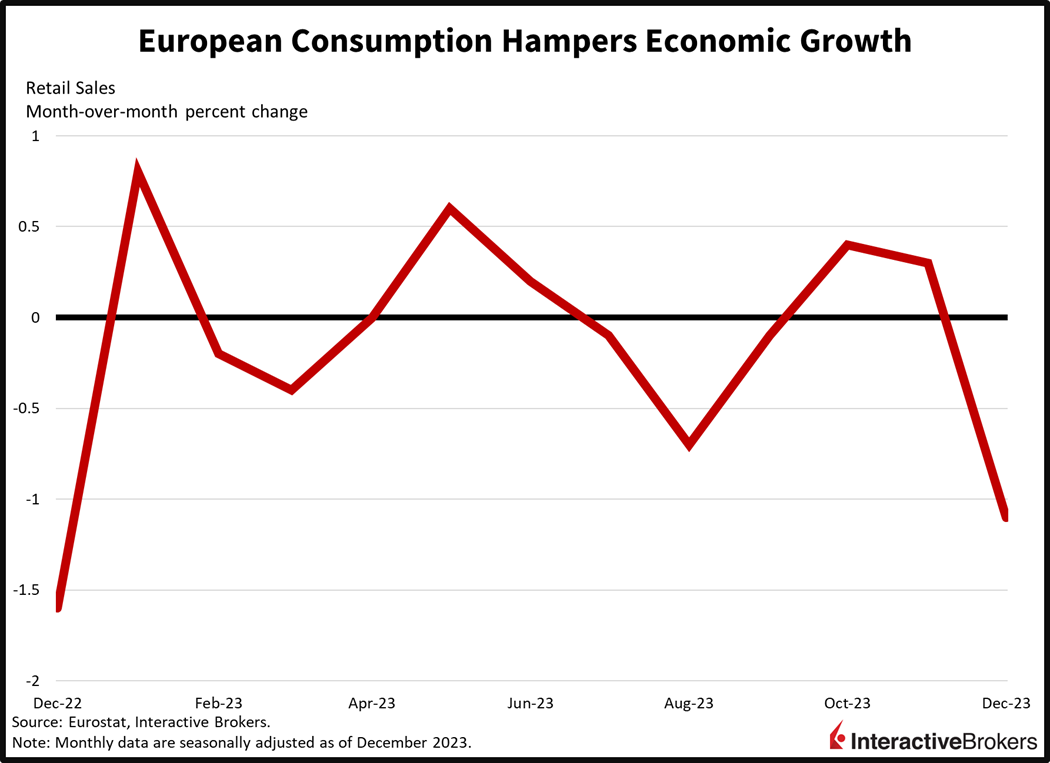

Europe Economy Limps Along

On Tuesday, Eurostat reported that December retail trade declined 1.1% in the euro area month over month (m/m) and 0.8% y/y. For calendar year 2023, the average level of trade declined 1.8%. The food, drinks and tobacco category experienced the largest decline of 1.6% while non-food products declined 1.0% and automobiles saw a 0.5% drop. Automotive fuel sales were flat. As the economy weakens and prices stabilize, expectations are growing for the central bank to cut rates. Much like the Bank of Canada and the US Federal Reserve, however, policymakers are cautiously waiting to cut rates with hopes of avoiding a second round of inflation that could result from turning dovish too quickly. In a Financial Times interview, ECB board member Isabel Schnabel noted that financial conditions have loosened, price expectations for services have increased, the supply chain is threatened by violence in the Red Sea and the labor market is resilient, all of which have intensified the debate about the timing of rate cuts.

Monetary Policy Will Hinder Growth

The European Central Bank and central banks of other developed countries such as Canada, the US and the UK are expected to loosen monetary policy this year. Meanwhile, various Latin American central banks have already shifted to dovish policies. Broadly speaking, economic data for developed countries has been stronger than expected, which could delay the easing of monetary policies and dampen growth in the coming months, while the lag in economic growth following the loosening of policies will be an obstacle among countries that have implemented rate cuts.

Geopolitical Risks Intensify

Geopolitical risks have escalated in recent months and could support price gains by hurting the supply chain, including the shipping of energy commodities and other products through the Red Sea. In the Israel-Hamas conflict, the multi-national Operation Prosperity Guardian established to safeguard the Red Sea hasn’t entirely eliminated the risks of Tehran-backed Houthi rebels who are attacking cargo ships as a show of support of Hamas. Meanwhile, the US has been attacking various targets in Iraq and Syria that are linked to Iran’s Islamic Revolutionary Guard and Iranian proxies. As the US carries out strikes, it will need to do so in a manner that doesn’t widen the Israel-Hamas conflict. Meanwhile, the Russia-Ukraine war that started roughly one year ago shows no sign of abating while the US Congress continues to debate providing additional support to Ukraine. In a final note, China appears to be in an uneasy holding pattern regarding its controversial desire to annex Taiwan. So far, peace has resulted from the view that Taiwan lacks formal independence, but at the same time, formal reunification hasn’t occurred.

Earnings Reflect Tough Macro Environment

A variety of economic cross currents influenced recent earnings reports as illustrated by the following examples:

- Alibaba’s fourth-quarter revenue of 260.35 billion yuan, or US$36.6 billion, grew only 5% y/y and missed the analyst expectation of 262.07 billion yuan. Its net income of 14.4 billion yuan dropped 69% y/y as the company faced the headwinds of weak domestic sales.

- Siemens Energy, a German technology provider, posted a 1.58 billion euro ($1.7 billion) net profit for its fiscal first quarter, with results benefiting from the company selling its 18% stake in India’s Siemens Limited for 2.1 billion euros. However, revenue on a comparable basis jumped 12.6% y/y driven by a 23.9% increase in orders. Its quarterly profit before special items hit 208 million euros compared to the 282 million euro loss in the year-ago quarter. Siemens is benefiting from a worldwide effort to reduce carbon emissions with BloombergNEF (BNEF) reporting that spending on developing renewable energy, creating alternative energy supply chains and financing totaled $2.8 trillion last year and increased 17%.

- Yum Brands, which operates Taco Bell, Pizza Hut and KFC, missed the analyst expectation with results hurt by the Israel-Hamas conflict. Its fourth-quarter earnings per share (EPS) of $1.26 adjusted fell below the $1.40 analyst estimate and revenue of $2.04 billion trailed expectations by $700 million. McDonalds and Starbucks have also felt the brunt of the conflict.

- Chipotle Mexican Grill results benefited from a strong increase in visits to its restaurants. Its adjusted EPS of $10.36 surpassed the analyst expectation of $9.75. Its revenue of $2.52 billion climbed 15.4% y/y and beat the analyst expectation of $2.49 billion. Many fast-food restaurants have reported declining visits to their locations, but Chipotle said its store traffic increased 7.4% and its comparable sales climbed 8.4%, beating the analyst expectation of 7.1%.

- Pinterest reported revenue of $981 million, which missed the $991 million expected by the analyst consensus despite climbing 12% y/y. However, its EPS of $0.53 beat the analyst expectation of $0.51. The company’s number of monthly active users increased, but the global average revenue per user of $2.00 missed the analyst estimate of $2.05.

Equity Investors Are Bullish

While most companies are struggling to sustain revenues and earnings against the backdrop of challenging macroeconomic conditions, investors are looking ahead to a rosier future. The bull case thrives on the idea that companies are downsizing and becoming more efficient through reduced headcounts and artificial intelligence adoption as they look forward to looser monetary policy in the near future. How much this enthusiasm reignites a fresh leg of inflationary pressures will be top of mind for central bankers, while market bulls continue to cheer on “productivity miracles”.

Most US equity indices are higher with the Nasdaq Composite, S&P 500 and Russell 2000 indices up 0.7%, 0.6% and 0.3%. The former two have reached fresh all-time highs again. The Dow Jones Industrial Average is down 0.2%, however. Sector breadth is awful with only the technology, consumer discretionary and communication services sectors higher on the session; they’re up 1.1%, 0.3% and 0.3%. The laggards are being led by consumer staples, energy and real estate, which are down 0.8%, 0.7% and 0.6%. Bond yields are cautious though, with the 2 and 10-year Treasury maturities being sold off even as this morning’s CPI revisions reflected lower inflation than in previous readings. The 2- and 10-year Treasurys are trading at 4.48% and 4.18%, 2 and 3 basis points (bps) higher on the session. The dollar is near the flatline though, with the greenback gaining against the franc, yuan and yen but losing ground relative to the euro, pound sterling and Aussie and Canadian dollars. Crude oil is nearly unchanged with WTI at $76.50 per barrel as oil traders reflect on escalation-ceasefire dynamics in the Middle East.

How Much Valuation Expansion is Too Much?

With US equities now trading at 21 times forward earnings amidst lofty interest rates and little demand for cheap hedges against the backdrop of low volatility levels, bulls and bears are wrestling over the sustainability of this rally. Are we entering a new era of loftier valuations due to rising productivity, increased retail participation and money shifting from the East to the West? Or is this a bubblicious mania that will end in tears as wild speculation takes over markets? In the end, only time will tell, but my intuition keeps me in the bearish camp based on a thought process anchored by funds shifting towards reasonable efficiencies over the medium- to long-term rather than chasing unlimited upside, an unsustainable process in my view. Forward earnings yields of 4.7% just aren’t enough compensation to own risk assets when considering the plethora of risks on the horizon alongside fixed-income alternatives that pay well in excess of 5%.

Visit Traders’ Academy to Learn More About Economic Indicators.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.