Equity markets are soaring on the back of a big thumbs-up following Nvidia’s earnings report featuring robust growth in its data-center segment. The S&P 500 and Dow Jones Industrial indices marched to fresh all-time highs, while the Nasdaq Composite remains a few points away from another milestone. On the fixed-income front though, stronger than expected data, hawkish rhetoric from Fed members, a lousy 20-year auction and loftier oil prices are pushing bonds lower and yields higher. The animal spirits in stocks are hard to ignore, with stocks up 7% year to date following a buoyant 24% last year, leading to some market participants becoming increasingly worried about inflationary pressures. Against the backdrop, the June Fed meeting is slowly moving into coin-flip territory for the first cut while other market players start to wonder if the central bank should hike again.

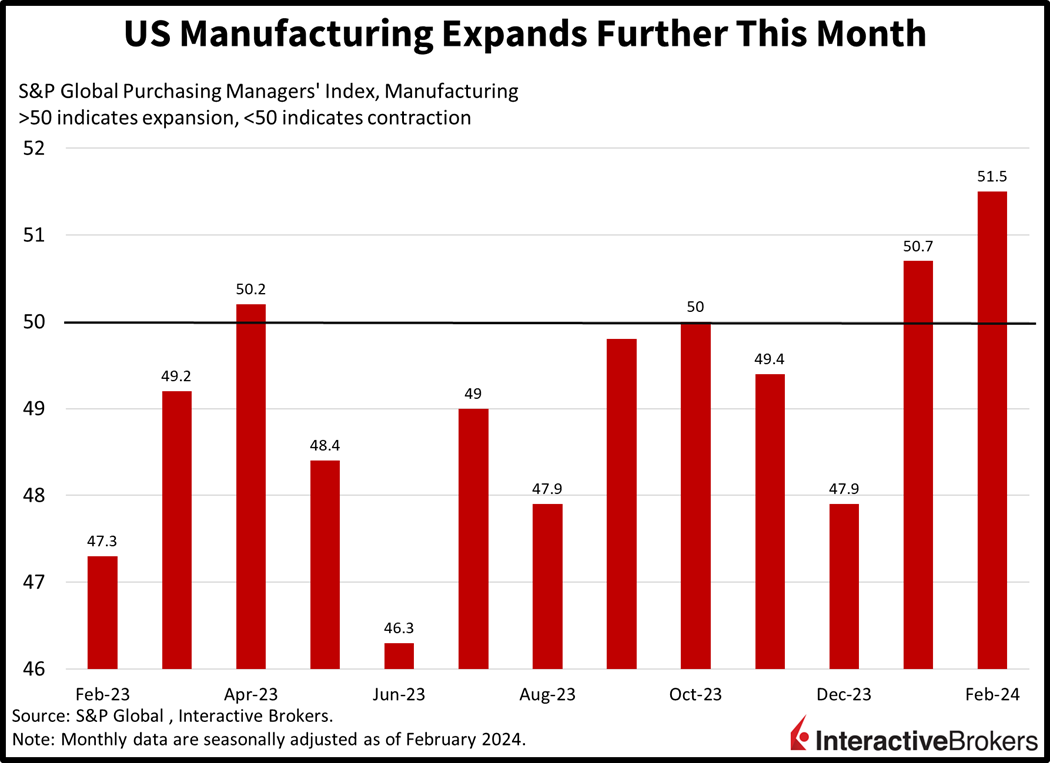

US Manufacturing Expands Further

The US economy is expanding solidly so far this month, according to S&P Global’s Purchasing Managers’ Indices (PMI). The manufacturing sector led for a change, reaching a 15-month high. With a PMI result of 51.5, it was solidly above the contraction-expansion threshold of 50 and better than the 50.5 anticipated by analysts. Growth was supported by stronger ordering, which drove quicker outputs and higher selling prices despite lighter cost burdens for manufacturers. Higher headcounts, increased confidence and faster delivery times on the back of improved weather conditions also contributed to the positive momentum in the sector.

US Services Decelerates Marginally

The US services sector also reported growth while it did decelerate from the previous month. The Services PMI arrived at 51.3, lighter than the estimated 52 and the 52.5 from last month. While demand has been firmly positive so far this month, slower ordering and lighter output relative to last month contributed to the deceleration. The slowdown affected hiring levels and confidence, which were hampered by reduced customer traffic. Indeed, the pace of hiring slowed to the lowest speed in three months. Prices did provide some support to the figure, however, with servicers raising their charges on consumers.

Europe Economies Continue to Weaken

Across the Atlantic, economic conditions remained in contraction territory in the eurozone even as the services sector climbed into purgatory. Recovering services led to the economy slipping at the slowest rate in eight months. The services sector achieved a breakeven figure of 50, better than last month’s 48.4 as forecasters were awaiting 48.8. For services, this is the first month above contraction since July. Hiring and business confidence helped the sector significantly, but prices did climb at the fastest pace in nine months. The manufacturing sector remained in the basement, meanwhile, coming in at 46.1, below the projected 47 and January’s 46.6. Weak ordering and lighter workforce numbers contributed to softer selling prices despite rising cost burdens. A decline in business sentiment also weighed on the sector. The eurozone is particularly vulnerable to the disruption in goods transportation via the Red Sea which is pushing up input costs and weighing on margins and orders. Improved prospects in France offset sharp weaknesses in Germany, the region’s largest economy.

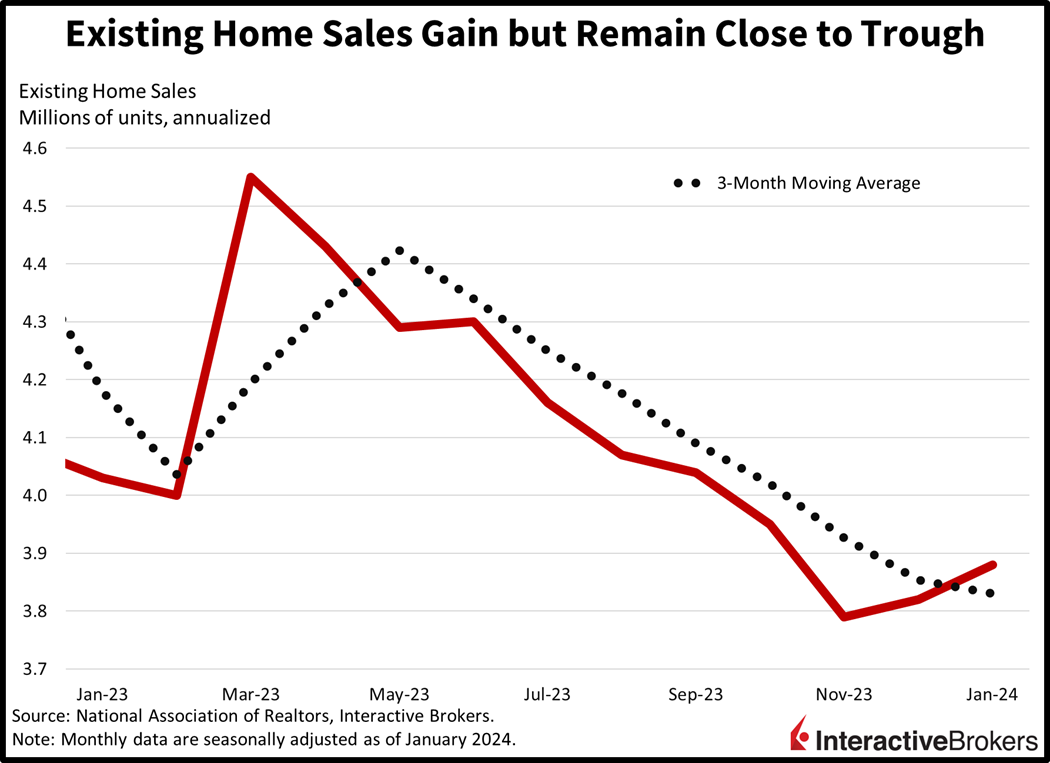

Real Estate Picks Up

In real estate land, the pace of existing home sales recovered last month as buyers took advantage of a sharp decline in mortgage rates. Rate relief off of the October highs led to a recovery in December and January. In January, the rate of existing home sales rose 3.1% month over month (m/m) to 4 million seasonally adjusted annualized units (SAAU), better than the 3.97 million anticipated and the 3.88 million reported in December. Gains were driven by single-family homes, which were up 3.4% m/m, while the condominium and cooperative segment was unchanged during the period. Across regions, the West, South and Midwest led, with transactions rising 4.3%, 4% and 2.2% m/m. The Northeast came in unchanged. Against that backdrop, inventories rose 2% m/m to a level consistent with three months of supply considering the current transaction tempo. Median prices rose to an all-time high of $379,100, a 5.1% gain on a year-over-year (y/y) basis, the seventh consecutive period of y/y progress. High equity levels, buoyant capital markets and most mortgages locked in below 4% contributed to a low level of distressed sales, amounting to just 2% of total transactions, quite unchanged m/m and y/y. Realtors were more dependent on all-cash buyers, though, which represented 32% of the total, up from 29% m/m.

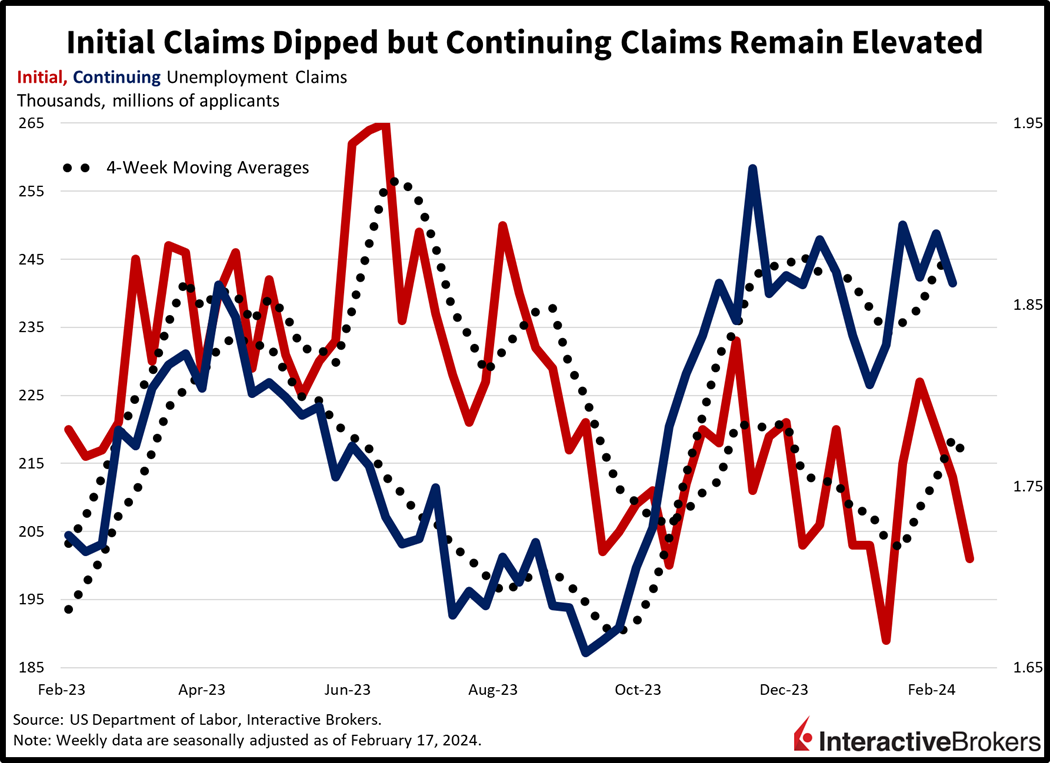

US Layoffs Fall

The trend of initial unemployment claims descended last week as employers avoided wide scale layoffs. Continuing claims remained elevated, however, pointing to laid off workers taking a longer time replacing their former paychecks. Initial unemployment claims fell to a five-week low of 201,000 during the week ended February 17, despite economists expecting a figure closer to 218,00. Last week’s initial claims drifted from the previous week’s 213,000 and its four-week moving average dropped to 215,250 from 218,750. Continuing unemployment claims came in at 1.862 million for the week ended February 10, down from 1.889 million reported in the previous period and below the 1.885 million expected. Although continuing claims declined, its four-week moving average rose to a fresh cycle high of 1.878 million from 1.869 million during the prior week.

Fed Remains Concerned About Inflation

Yesterday’s release of minutes from the Fed’s January meeting helped cement expectations that the central bank won’t cut the federal funds rate until June. The cautious tone of the minutes, however, reflects policymakers’ views prior to more recent data depicting much stronger-than-expected inflation. Broadly speaking, Fed members agreed with Chairman Powell’s January comments that more evidence showing that declining inflation is sustainable and is required before the bank can confidently ease monetary policy without risking a resurgence in price pressures. Policymakers also said they are highly attentive to the possibility of the decline in price pressures stalling and that more progress toward the central bank’s 2% inflation target is needed. The cautious tone of the minutes appears well warranted. January’s inflation reports were scorchers for both consumers and wholesalers. Furthermore, our real-time inflation indicators point to the likeliness of a worrisome inflation increase in next month’s data releases, reflecting the fourth consecutive monthly pickup in price pressures. This development may raise expectancies of a possible surprise hike by the Fed at their March meeting, which is currently not in the cards.

Nvidia Earnings Drive Euphoria

As the equity rally has narrowed and valuations have soared, investors have turned to Nvidia to assess semiconductor demand and the strength of the artificial intelligence (AI) sector. The company, which is a leading provider of computer chips for AI, computer gaming and data centers didn’t disappoint. Last night, it reported fiscal fourth-quarter revenue of $22.1 billion, which more than tripled y/y. The result surpassed the analyst expectation of $20.4 billion and the company’s guidance of $20 billion. Nvidia posted $12.3 billion in quarterly profits, or an adjusted earnings per share (EPS) of $5.16 that beat the analyst expectation of $4.64 and climbed significantly from $1.41 billion, or an EPS of $0.57, y/y. Nvidia estimates it will generate $24 billion in revenue for the current quarter, while the average analyst forecast was $22 billion. Nvidia Co-founder and Chief Executive Jensen Huang provided an optimistic outlook, explaining that he believes data centers will need to invest approximately $2 trillion to meet growing demands for AI. Nvidia shares rallied more than 12% after the earnings release.

AI Optimism Propels Equities Upward

Stocks are jumping higher as AI prospects encourage investors to pencil in future earnings and productivity growth. The action isn’t limited to the US, with Germany and Japan’s indices also marching to new all-time highs despite the nations navigating recessions. Who said recessions were bad for stocks? In the US, the Nasdaq Composite, S&P 500, Dow Jones Industrial and Russell 2000 indices are all higher by 2.5%, 1.7%, 0.7% and 0.7%. Sectoral breadth is impressively positive, with every sector higher minus a pair of defensive categories. Technology, communication services and consumer discretionary are leading; they’re up 3%, 1.4% and 1.3%. Defensive utilities and consumer staples are down 1% and 0.3%, meanwhile. Rates are moving higher though as the 2- and 10-year Treasury maturities trade near year-to-date highs of 4.71%, and 4.33%, 4 and 1 basis points (bps) higher on the session. The dollar is catching a bid on the back of tighter Fed anticipations, loftier yields, rising inflation expectations and better economic performance relative to its global peers. The greenback’s index is up 4 bps to 104.04 as the US currency gains relative to most of its major counterparts including the euro, pound sterling, franc, yen, yuan and Aussie and Canadian dollars. Crude oil is higher on the back of a mixed inventory report from the US that depicted a crude build amidst a gasoline draw. Ongoing geopolitical tensions are also supporting price gains. WTI crude is up 0.7%, or $0.54, to $78.52 per barrel on the news.

Will AI Improve Earnings Though?

After Nvidia’s robust earnings report, investors are focused on whether AI will continue to drive strong results for leading technology providers and if it will allow companies that eventually implement the products to become increasingly productive and more profitable. With many companies outside of the tech sector providing cautious guidance, it appears that the practical aspects of AI have yet to support aggregate profits. Nevertheless, the combination of high equity valuations and cautious guidance from many businesses outside of the tech sector has increased the significance of AI’s support of investor sentiment. Only time will tell if Nvidia CEO Jensen’s optimism is warranted and while bulls have been energized by his comments and Nvidia’s quarterly results, bears are praying that AI may be more fluff than substance.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.