Stocks are recovering today following yesterday’s head-fake on the back of a lousy 5-year note auction. However, this morning brought news of robust economic growth despite increasing layoffs, reinforcing the Goldilocks narrative. Additionally, the GDP report today highlighted a softening of price pressures in the fourth quarter, providing more ammunition for bullish market players. Yet, the possibility of a repeat of yesterday’s market reversal is certainly possible, especially with a 7-year note auction scheduled for 1:00 pm today. Investors are also grappling with the ongoing reversal of the cooperative roles that goods and commodities inflation have played last year. A key question many have asked me recently is “why is almost every single data point coming in hotter than expected?”

GDP Slows but Still Exceeds Expectations

Fourth-quarter economic growth came in strongly above expectations, with the second briskest pace of acceleration in 2023. This morning’s Gross Domestic Product release from the Bureau of Economic Analysis reflected a growth rate of 3.3%, shattering estimates for just 2% but slowing from the third quarter’s blistering 4.9% tempo. There was broad-based firmness across components. Consumption rose 2.8%, similar to the previous quarter’s 3.1%, as services outlays ramped up while goods spending slowed. Investment grew 2.1%, hitting the brakes from the previous period’s 10%, as homebuilder activity decelerated sharply while business investment also softened. Net exports and government spending also supported a robust headline figure, with the former contributing more relative to the last quarter while the latter gained at a more tempered level.

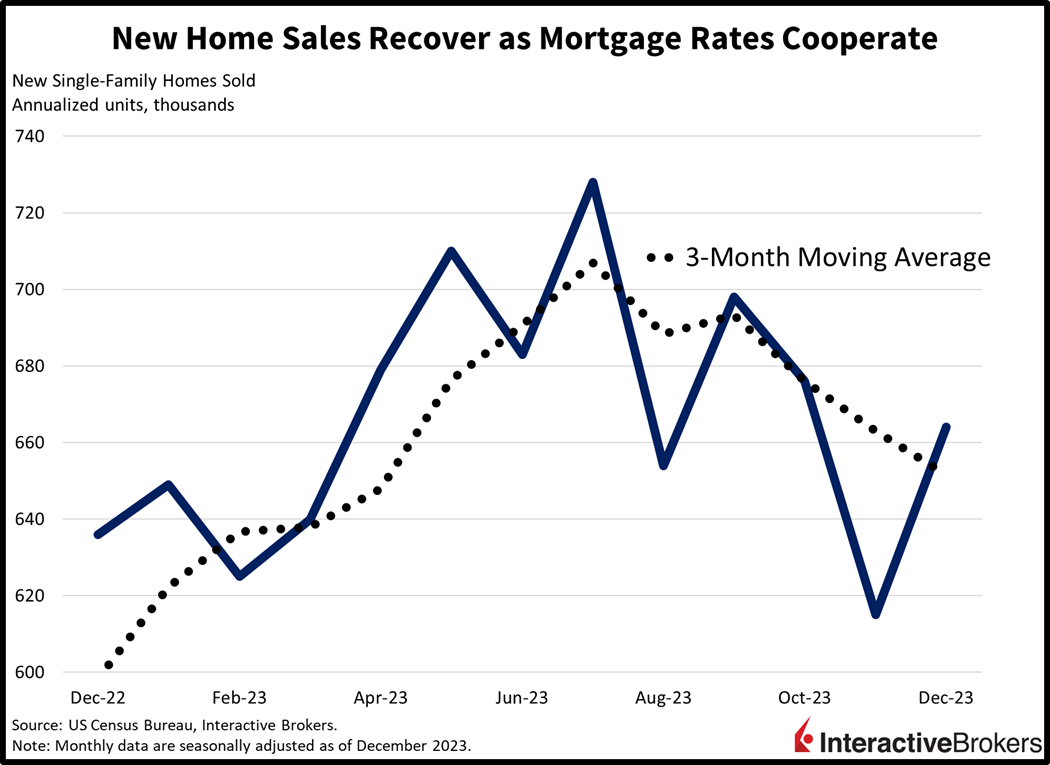

Dip In Mortgage Rates Supports New Home Sales

New home sales rose last month, propelled by lower mortgage rates that brought prospective buyers off of the sidelines. The seasonally adjusted annualized units (SAAU) reached 664,000, handsomely beating projections of 645,000 and marking a rise from 615,000 in November. The robust 8% month-over-month (m/m) increase benefited from significant contributions from the Northeast, up 32% m/m, the South, up 10.6% m/m, and the Midwest, up 9.2% m/m. However, the West declined 3.4% during the same period. Builders relied on discounting strategies to boost volumes, however, leading to a decrease in the median sales price from $426,000 to $413,200 m/m.

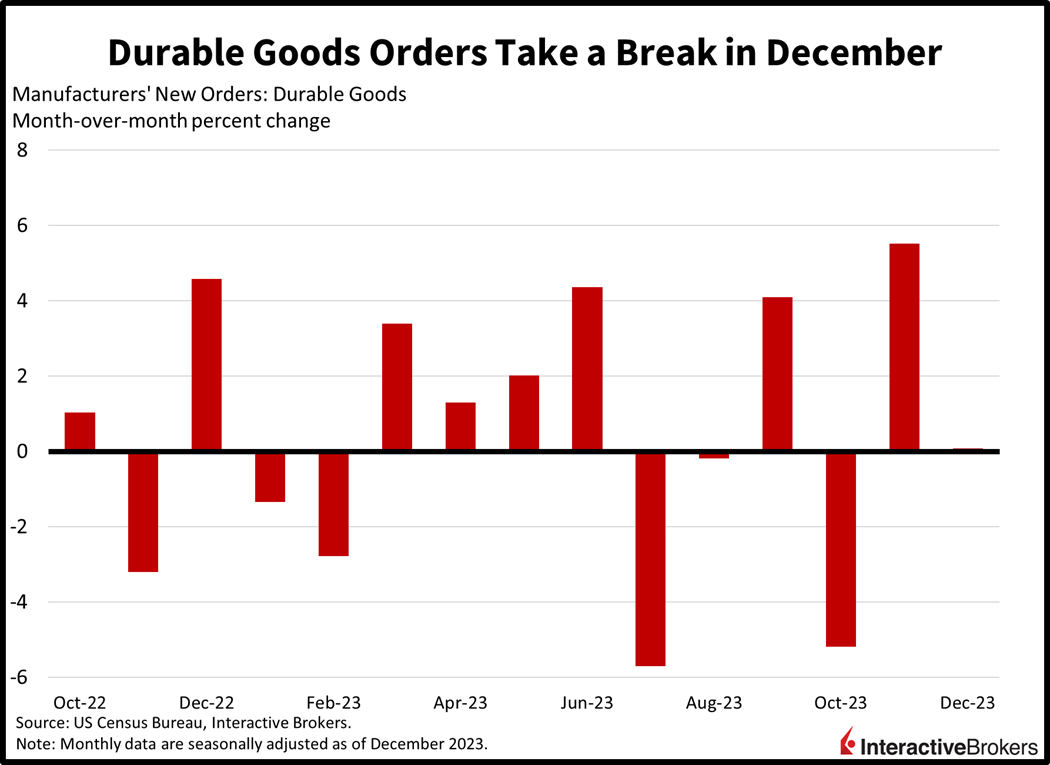

GDP Growth Bypasses Durable Goods

This morning’s durable goods report was a big doughnut, with new orders unexpectedly stalling last month. Economists anticipated slowing growth, projecting 1.1% following November’s sharp 5.5% m/m increase. Durable goods, excluding transportation, performed relatively better, increasing 0.6% m/m, and surpassing expectations of 0.2% and the previous period’s 0.5%. Notably, the largest decliner was defense aircraft, dropping by 2.9% m/m. Conversely, the leaders in the report were the communication equipment, electrical equipment, and primary metals categories, which saw gains of 5.2%, 1.8%, and 1.4%, respectively. Core capital goods, which exclude defense orders and aircraft and serve as a proxy for business investment, saw a modest increase of 0.3% m/m, slowing from the previous month’s 1% gain.

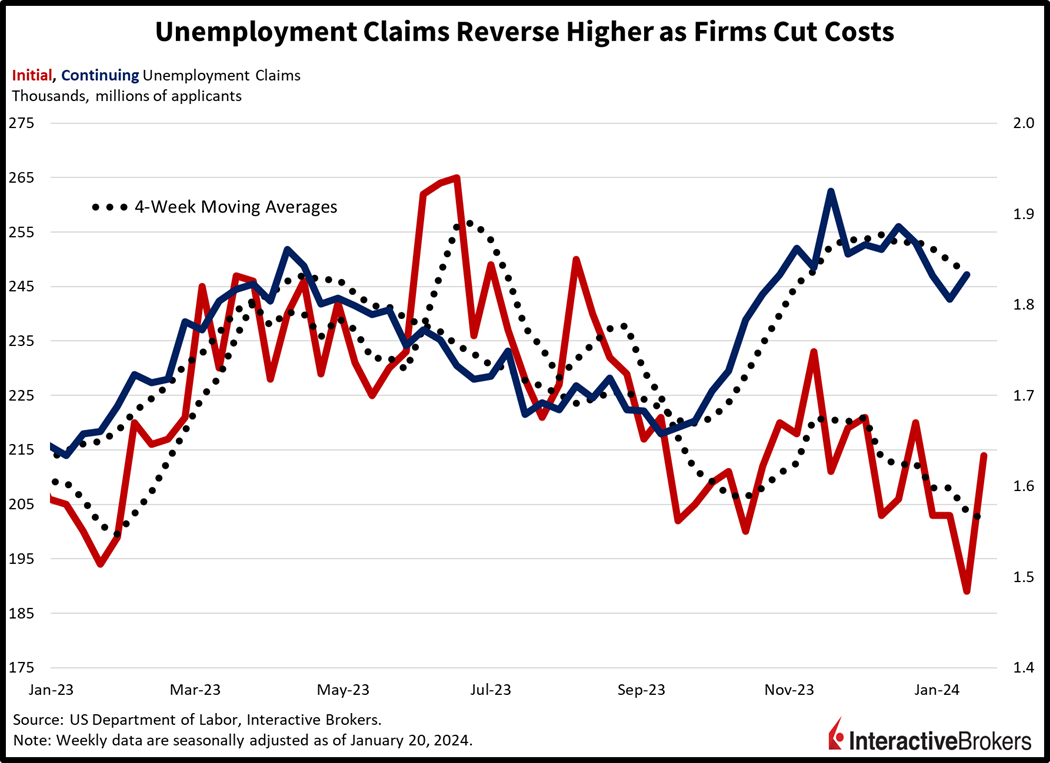

Layoff Announcements Make It to the Data

Unemployment claims rose last week as firms continued to push cost-cutting, efficiency and productivity efforts with top-line results under pressure. The impact of descending inflation is affecting pricing power and the ability to achieve revenue growth. Initial unemployment claims rose to 214,000 for the week ended January 20, surpassing the previous week’s 189,000 and exceeding estimates of 200,000. Continuing claims also saw an uptick, rising to 1.833 million from 1.806 million for the week ended January 13, exceeding forecasts of 1.828 million. The trend for both figures, however, continued to point lower, with the four-week moving averages for initial claims and continuing claims shifting from 203,750 and 1.848 million to 202,250 and 1.835 million, respectively.

IBM Gains as Businesses Seek Efficiency

Artificial intelligence is continuing to fuel optimism about potential growth of technology companies while a price battle has weighed upon the earnings of Tesla. Consider the following fourth-quarter earnings highlights:

- IBM, like many other tech companies, expressed optimism regarding the growth of artificial intelligence (AI) as companies react to a challenging economy by seeking new ways to improve efficiencies. In the fourth quarter, the company’s earnings per share (EPS) of $3.87, not including irregular expenses, grew 8% year-over-year (y/y) and beat the analyst expectation of $3.76. Fourth-quarter revenue of $17.4 billion climbed 4.1% from the year-ago quarter and surpassed the analyst expectation of $17.3 billion. During the recent quarter, IBM’s revenue for generative AI doubled from the third quarter. The company’s consulting and software revenues fell short of the analyst consensus expectation, but infrastructure revenue, which includes mainframe computers, totaled $4.60 billion, up 3% y/y and above the $4.28 billion expected by analysts. Earnings benefited, in part, from the company reducing capital expenditures and trimming its real estate. Chief Executive Officer Arvind Krishna says he expects a trend of businesses using technology to improve productivity is likely to continue this year. The company also said it expects 2024 revenue to grow in the “mid-single digits” while analysts expected a 3% growth rate. It estimates free cash flow will increase to about $12 billion this year, up from $11.2 billion in 2023 and above analysts’ expectation for $10.9 billion. Shares are up 11% on the session.

- Tesla generated a disappointing quarter, a result of discounting prices to boost sales in response to growing competition as more companies roll out electric vehicles. The company reported a fourth-quarter EPS of $0.71, down from $1.19 in the year-ago quarter and trailing the consensus estimate of $0.73. Tesla’s revenue of $25.2 billion climbed 3% y/y but missed the analyst expectation of $25.9 billion. An increase in vehicle deliveries and sales of batteries supported revenue, but a decline in the average selling price of vehicles and the timing of recognizing sales from its Full Self-Driving (FSD) Beta v12 update were headwinds. Expenses from AI and other R&D projects, the lower average vehicle selling price and costs of ramping up its Cybertruck sales hurt earnings. While the company didn’t provide earnings guidance, Elon Musk said he is optimistic that the launch of a lower priced model to be built in Mexico and Texas will support growth. However, Tesla’s share price declined approximately 8% this morning.

Market Bulls Try to Recover

Markets are bullish with all major US equity indices higher on the session while bond yields decline. The small-cap Russell 2000 and technology concentrated Nasdaq Composite indices are leading the way higher; they’re up 0.6% each. The S&P 500 and Dow Jones Industrial indices aren’t far behind, with the measures gaining 0.5% and 0.3%. Sectoral breadth is impressively positive, with all sectors higher except consumer discretionary and healthcare; those sectors are down 1.1% and 0.9%. The other nine sectors are higher, led by real estate, communication services and technology which are up 1.4%, 1.4% and 1.2%. Bond yields are lower ahead of a big auction. The 2- and 10-year Treasury yields are trading at 4.33% and 4.15% with the instruments’ yields down 5 and 3 basis points (bps) on the session. The dollar is recovering from yesterday’s losses, though, as the European Central Bank refused to discuss rate cuts at today’s meeting. The result is a selloff in European currencies, as market players become nervous that the continent’s nations need rate cuts right here right now. A lack of progress on inflation, however, kept Lagarde and her squad hawkish. The Dollar Index is up 33 bps to 103.59 as the greenback gains versus the euro, pound sterling, franc, yen, yuan and Aussie dollar while the US currency backtracks relative to the Canadian dollar.

China Stimulus Ignites Oil Price Rally

Oil prices surged on today as China’s decision to lower bank reserve requirement to stimulate its ailing economy with a $140 billion injection into the financial system fueled expectations that demand for energy commodities will surge. Additionally, the recent attack by Houthi forces on ships near Yemen’s coast also highlighted the risks to trade along a crucial global transit route. These factors pushed up Brent crude oil’s price $1.29, or 1.6%, to $81.33 per barrel while U.S. WTI increased $1.37, or 1.8%, and hit $76.46 per barrel.

Hot Data Dampens Optimism for March Rate Cut

Overall, this level of economic growth alongside a tight labor market and above-target inflation is likely to make the journey across the monetary policy bridge longer and riskier, with market players now pricing in the first Fed cut in May rather than in March. A higher-than-expected Personal Consumption Expenditures report tomorrow could cement three consecutive weeks with hat tricks of robust economic data, pointing to growing disparity between investors’ expectations for a rate cut and likely actions from the central bank’s policymakers. Last week featured strengthening consumer sentiment, low unemployment claims and hot shopping trends during the holiday season. Yesterday saw PMI-Manufacturing turn positive and increasing momentum in PMI-Services. After today’s GDP read, a hot PCE report tomorrow would be just one of many recent indicators pointing to continued upside risks in economic activity that could lead to inflation. Market direction is likely to be determined by investors focusing on either the potential for a strong economy to support earnings growth or fears that prolonged monetary tightening will challenge earnings, valuations and economic prospects. Finally, the Fed is taking notice of animal spirits in markets and is withdrawing liquidity, announcing yesterday that the Bank Term Funding Program will end on March 11 and not be extended. This development is likely to weigh on bond yields and challenge the health of regional banks.

Visit Traders’ Academy to Learn More About GDP and Other Economic Indicators.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.