Christian Correa, Chief Investment Officer of Franklin Mutual Series, discusses his team’s top three themes for the back half of 2023: a less-gloomy US macroeconomic outlook, real asset investment and Japan’s rising sun.

It’s been an eventful year so far. Investors are navigating geopolitical and economic challenges in the United States and abroad. Some investors and economists believe the specter of a US recession still lurks on the horizon. Regardless of the market environment, we believe there are three main themes emerging for the final months of 2023. We believe strong underlying forces carrying the US economy forward, continued investment in real assets and growth in Japan can provide a beacon for investors the back half of the year.

The US macroeconomy

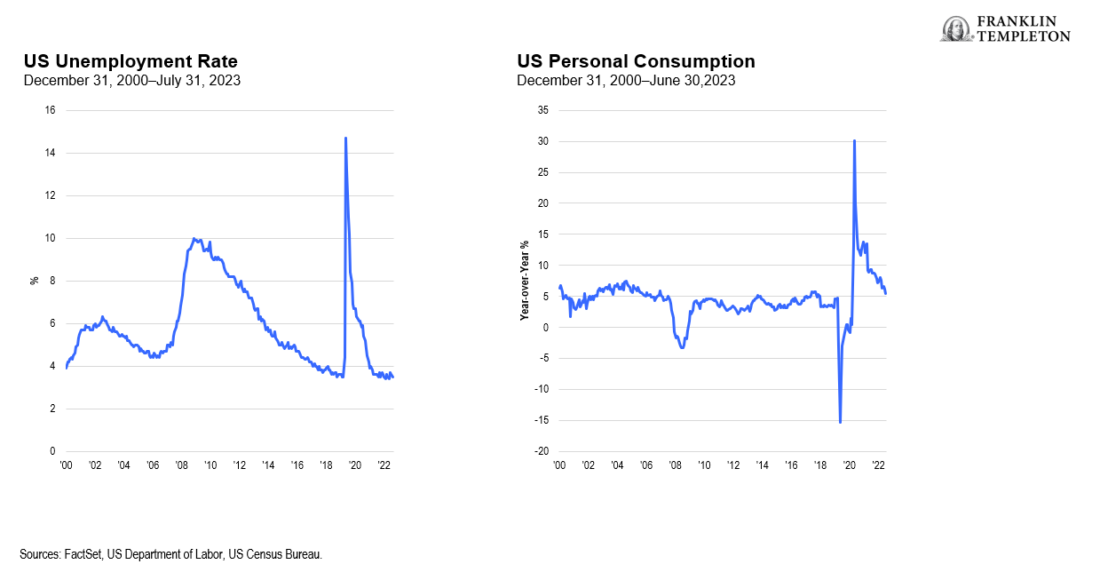

Inflationary pressures may not be the deathblow for the US economy that many expected. A tight labor market, strong consumer spending and economic strength across several industries have driven inflation but are also generally positive for economic activity. However, we expect the consumer to pull back on spending if we start to see job losses or deteriorating confidence, which in turn might dampen pricing pressures.

Exhibit 1: An Employed Consumer Continues to Spend

The prospect of higher interest rates leading to a recession has made investors nervous, causing volatility and market dislocations. But as US inflation continues to subside and labor markets remain strong, we continue to see opportunities at reasonable prices.

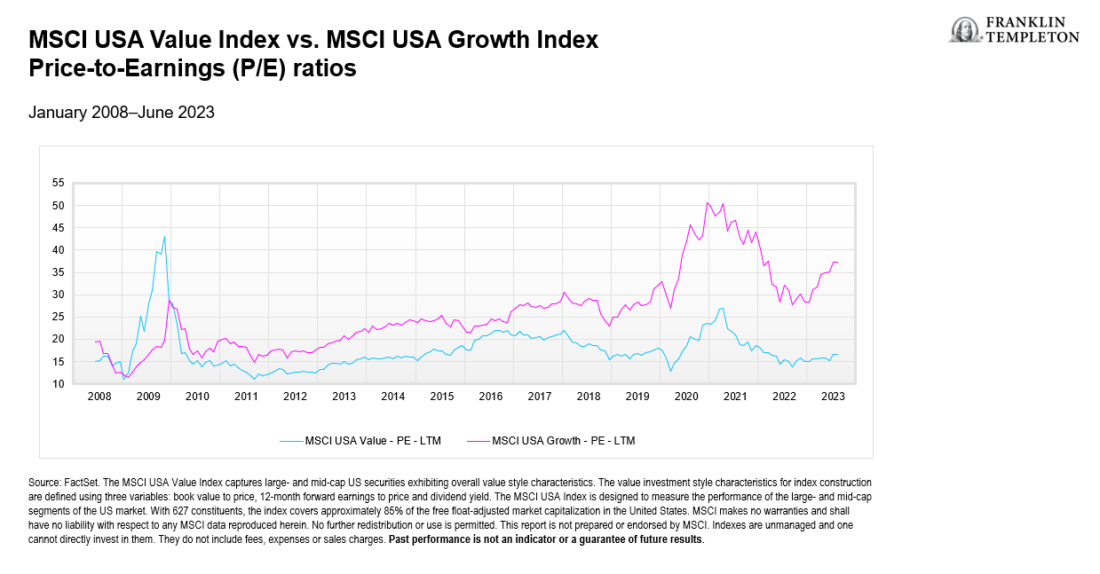

Meanwhile, valuations for growth stocks have inflated again to historically high levels, which are correlated with historically low forward returns. Moreover, long-term interest rates have a greater bearing on economic strength than short-term rates, in our view. And through the rate hiking cycle, long rates have responded more slowly and have remained near historic lows.

Exhibit 2: A Less Expensive Entry Point for More Potential Upside

Investing in real assets

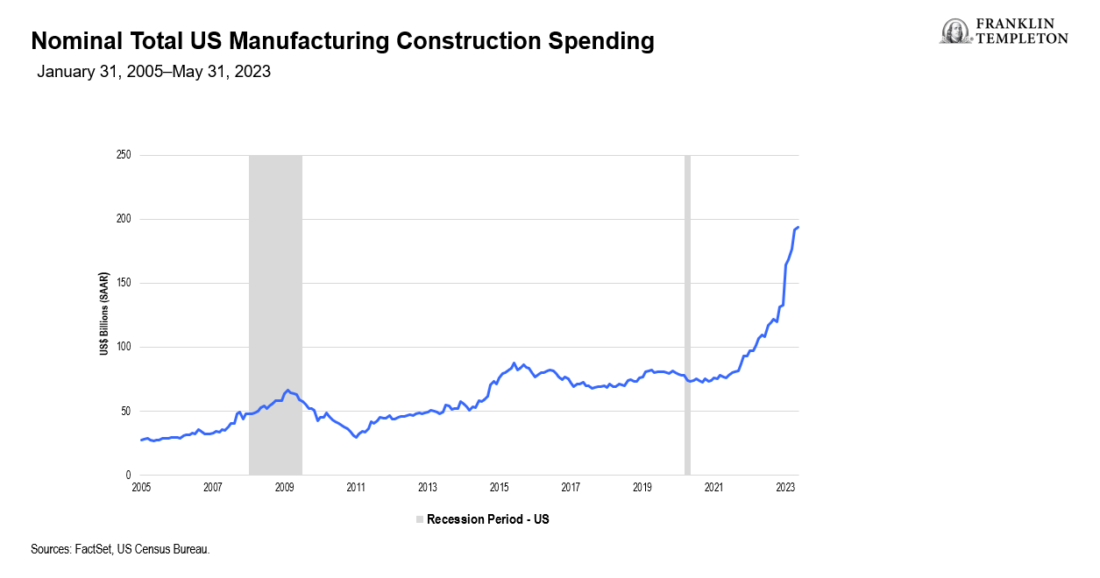

We expect an increase in infrastructure spending to support investment in real assets. This increased spending should be positive for the US and global economies as well as for value investors. Recent US legislation incentivizes US infrastructure building and reshoring initiatives, while Europe and Japan have their own initiatives.

Spending on projects has only just started, and we expect increased construction and manufacturing activity to bolster the economy and revenues for companies that produce physical items, like mining and aluminum companies, or those which could benefit from the knock-on effects of increased demand for these things. We expect value-oriented companies that deal in building materials, construction equipment, manufacturing, and other related industries to see increased demand as this trend continues over the next several years.

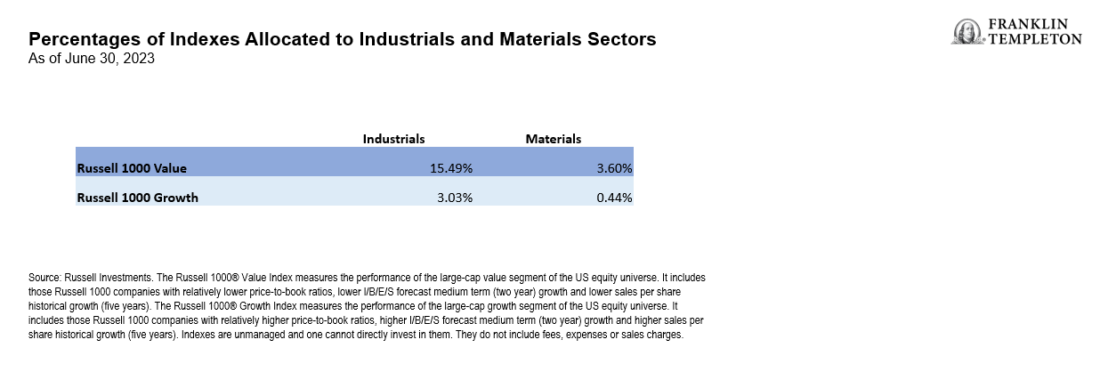

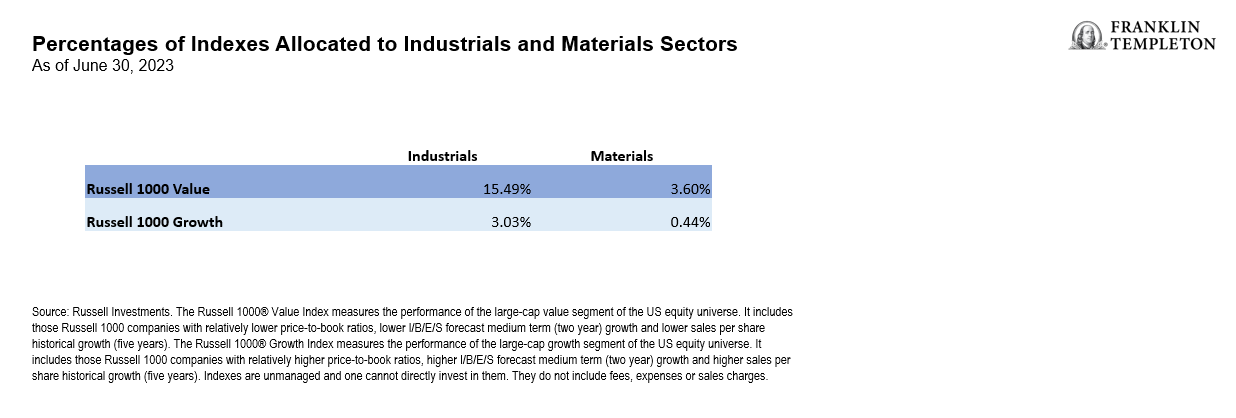

Exhibit 3: Construction Spending Booms…

Exhibit 4: …Providing an Opportunity for Value Stocks

Japan

Opportunities to invest in undervalued companies outside of the United States abound, particularly in Japan, where we believe the economy is poised for growth and modest inflation. Additionally, the government, the stock exchange and shareholders are all pushing companies to improve business dynamism.

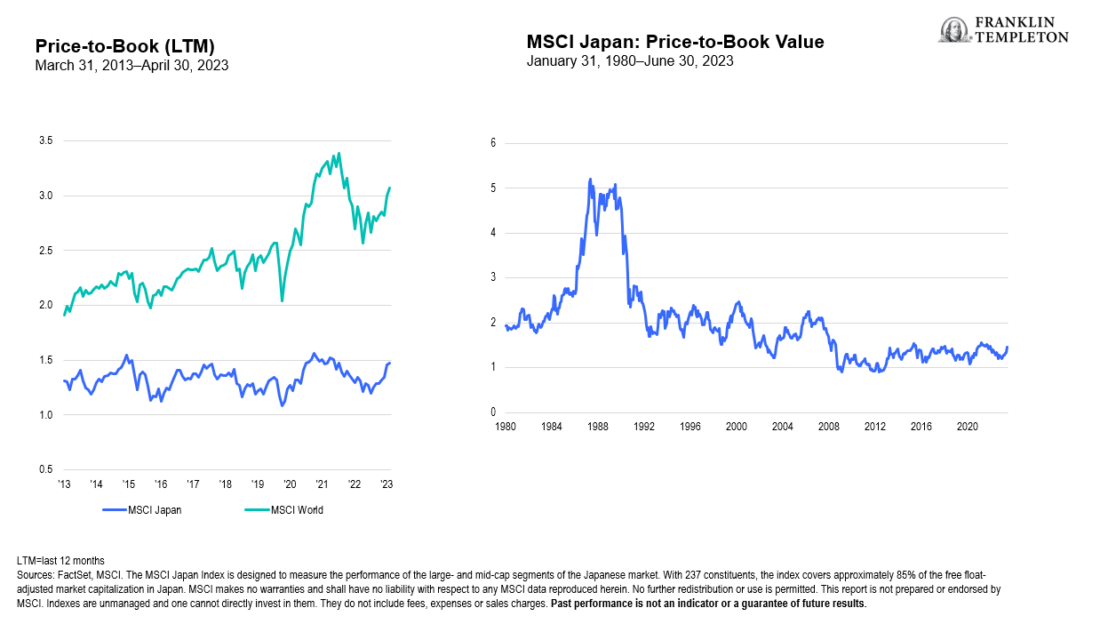

Japanese companies provided a competitive price to book (P/B) value in the 1980s but have lagged the rest of the world in recent decades. Unlike in the past, management teams are now younger and more willing to change. As a result, we see a focus on corporate reform and returns on equity, producing new investment opportunities.

Exhibit 5: Japanese Companies are Focused on Improving Price-to-Book Value

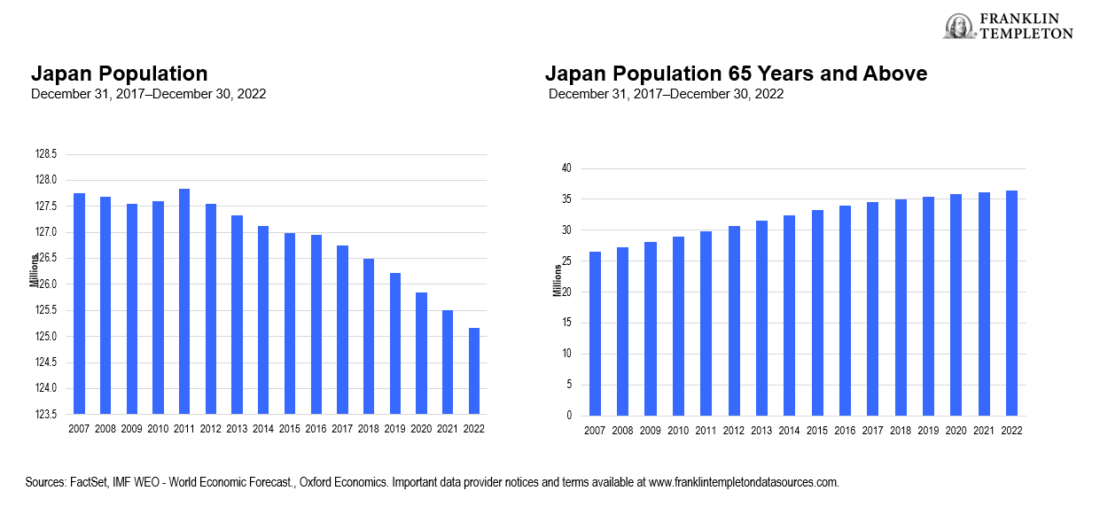

In our opinion, an overarching catalyst for reform in Japan is a societal understanding that demographics have changed. Japan is an aging society, and thus the ability to add more labor is difficult. To fund the government, social insurance payments and health care, the Japanese economy needs to increase the returns on its capital base. Changes in the economy and to the way businesses operate will be necessary to facilitate returns.

Exhibit 6: An Aging Population Means a Need for Increased Business Dynamism

Our approach to investing in Japan mirrors our approach for all markets—to look for inexpensive, undervalued companies that can find new growth opportunities globally and where management is willing to engage with us.

In the back half of this year, we think it is possible geopolitical events and central bank decisions may continue to drive market volatility. We will continue to look for these dislocations to provide chances to purchase quality companies below what we believe to be their fundamental value. Despite these factors, we currently see opportunities in non-US and US companies driven by strong underlying trends in the US economy, incased investment in real assets and changes in Japanese capital markets. We think that these themes stand out against the backdrop as areas of opportunity for investors in the coming months and look forward to providing additional insights and updates as the year unfolds.

—

Originally Posted August 11, 2023 – Three value equity themes for the end of 2023

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

To the extent a strategy invests in companies in a specific country or region, it may experience greater volatility than a strategy that is more broadly diversified geographically.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Value securities may not increase in price as anticipated or may decline further in value. The investment style may become out of favor, which may have a negative impact on performance.

Active management does not ensure gains or protect against market declines.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

Disclosure: Franklin Templeton

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Franklin Templeton and is being posted with its permission. The views expressed in this material are solely those of the author and/or Franklin Templeton and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.