The eagerly awaited Nonfarm Payrolls report was released at 8:30 (EST) this morning, and it produced a collective gasp amidst traders. The headline number was an increase of 210,000 vs. a consensus estimate of 550,000. That is an enormous miss, and appears to reflect significant weakness in the labor market. The knee-jerk reaction was a rally in both bonds and stocks, which reflected something we discussed yesterday:

Tomorrow’s report may prove to be a case where traders are actually hoping for bad news. A stronger than expected report would further kindle fears that the Fed would be more aggressive in tapering purchases and more able to raise rates sooner than hoped, while a weaker result could be perceived as allowing the Fed to extend monetary stimulus more than currently expected.

It is clear that both traders and news-reading algorithms were programmed to buy those assets if the headline number missed expectations. But a closer reading of today’s statistics was warranted. The unemployment rate plunged to 4.2% vs. a 4.5% estimate even as the labor force participation rate rose to 61.8% vs. a 61.7% expectation. The underemployment rate also dropped to 7.8% from a previous 8.3%. It could be a sign of labor slack if the unemployment rate fell because the labor force declined, but these appeared to be directly contradicting the nonfarm payroll report. Bonds quickly reversed their early gains, leading to higher yields across the curve, though stock futures continued higher into the 9:30 market open. That was their high for the day so far.

For those of you who may wonder why I assert that bond traders have a better read on the economy then their equity brethren, this is yet another example. Fixed income markets recognized that there was little in today’s report to dissuade the Federal Reserve from accelerating their taper while stock traders remained fixated on momentum and continuing yesterday’s buy-the-dip bounce. Bond traders were quicker to recognize the inherent strength in the bulk of the report.

Today’s report reminds me of the September payrolls report. On October 8th we saw a nonfarm payrolls increase of 194,000 vs. a 500,000 estimate. At the same time, the unemployment rate fell to 4.8% vs. a 5.1% estimate. That failed to dissuade the Fed from announcing that they would taper bond purchases when they met on November 3rd. And two days later, on November 5th, there was a reversal in labor statistics. The payrolls report showed an increase of 531,000 in October vs. a 450,000 estimate while September was revised up to 379,000. Bear in mind that every payrolls report since April has been revised upward. If I know this, then the labor economists at the Fed certainly do.

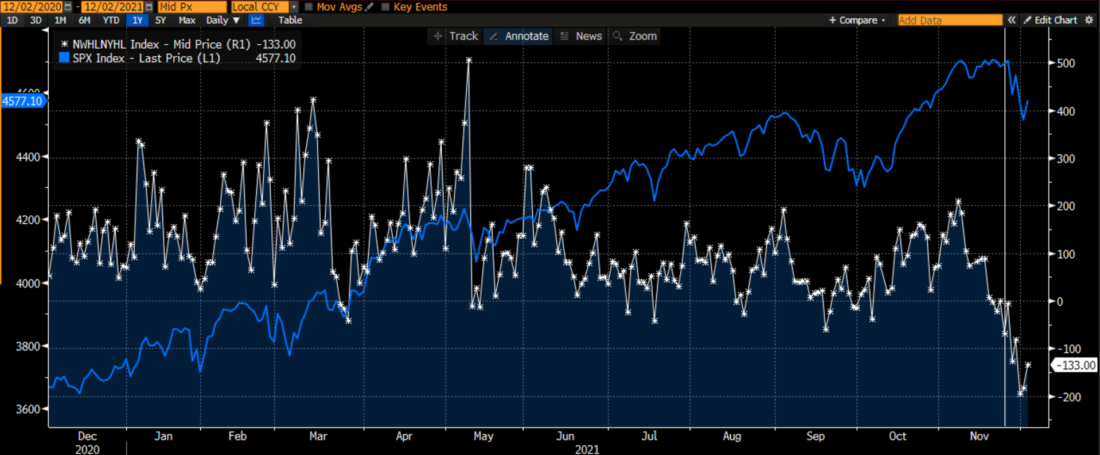

Reading below the headlines is important for stock traders in many other ways. Various technical indicators were flashing cautious signs just as the Omicron Covid news came to light. One important signal was the failure of the cumulative advance-decline lines to confirm the recent highs in the S&P 500 (SPX) and NASDAQ 100 (NDX) indices, as evidenced below:

SPX (white) and NDX (yellow) Versus NYSE (red) and NASDAQ (green) Cumulative Advance-Declines

Source: Bloomberg

Pay particularly close attention to the period in mid to late November. We see the advance-decline lines decline even as SPX and NDX reach new all-time highs. This shows that even as the key large-cap stock indices displayed strength, the majority of stocks on major US exchanges were not. A graph of NYSE new highs minus new lows tells a similar story. New lows on the NYSE were outpacing new highs even as SPX hit its highs, as the graph below shows:

SPX (blue) vs. NYSE New Highs – New Lows (white)

Source: Bloomberg

We all know that technical analysis is far from foolproof. But during the prior month’s euphoria and new highs in key equity indices, a close look below the surface of the markets told a different story than the headlines, just as today’s labor report showed too.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.