Those willing to do the groundwork and explore a less glamorous aspect of the energy transition may discover many opportunities in grid investment.

The pandemic and Ukraine war have tested the limits of all variety of supply chain. In a similar fashion, we expect the risks of unchecked climate change to focus minds on another vital supply chain to our everyday lives and the smooth running of business – electricity grids.

High voltage cables are at the heart of these networks, such as the new ones currently being laid in three-metre wide specially created tunnels up to 50 metres under London’s streets. I recently visited the “London Power Tunnels” to witness the great progress being made here (see video, above).

New cabling such as this will be vital to meet a dramatic increase in demand for electricity as fossil fuel based heating and transport systems are electrified in the coming decade. The upgrading of grids have also become a national security priority after the invasion of Ukraine exposed Europe’s unhealthy reliance on Russian gas.

While the tunnels may be one of London’s largest capital investment programmes at present, they are just a single element of a much more ambitious root-and-branch overhaul of the entire UK electricity grid, requiring tens of billions of pounds of investment.

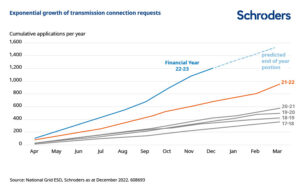

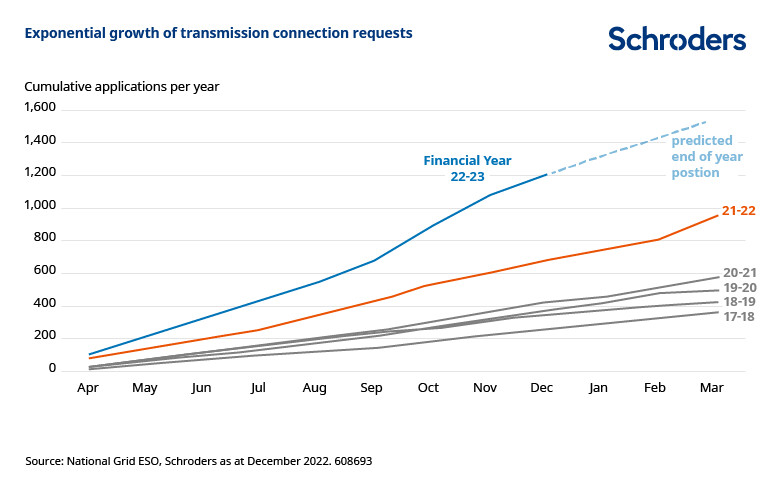

Step-change in grid investment requirements

These developments are creating significant growth opportunities for investors. While potentially less photogenic than the huge new windfarms currently being built off the shores of Scotland and England’s eastern flank, the grid is just as vital to the energy transition under way.

That said, I think you’d agree from my video of the London Power Tunnels, they are quite a feat of engineering.

Countries around the world are racing to meet ambitious targets to reduce greenhouse gas emissions to net zero to avoid unchecked global warming – “decarbonising” grids will be a necessary condition of meeting these targets.

Not only will the grid need to keep pace with the growth in electricity demand, but also connect to a multitude of new renewable energy sources coming online in the coming decade. That means a whole array of new equipment will be required, from interconnectors to battery storage capacity, the latter to help manage the intermittent nature of renewable energy.

A grid powered by renewable energy will also have fundamentally different properties to the existing configuration based on mainly gas-powered turbines. As a result, new investment will also be required in technologies to maintain system stability.

As such, the International Energy Agency forecasts every $1 spent on renewables will soon require a matching $1 on grid investment (versus 70c in the past) – totalling some $800 billion per annum globally post 2030.

UK chasing ambitious decarbonisation targets

Certainly the UK is showing ambition for connecting up renewable generation, with the current government committed to decarbonise the electricity system by 2035 and the Labour Party aiming for an even more ambitious deadline of 2030.

The UK grid was largely built in the 1960s and was designed to generally transport power from large single source coal and nuclear plants, typically located in the north of England to the areas of greater electricity demand in the south.

Now it will need to adapt to remote large offshore wind farms, as well as a multitude of smaller “decentralised” solar or battery storage projects, including smaller scale – distribution level – installations in homes and businesses.

The annual level of transmission connection requests has increased by around ten times compared to the level five years ago (see chart, below).

The National Grid Electricity System Operator (ESO), the body in charge of managing the grid, estimates UK electricity demand is forecast to grow by roughly 50% by 2035 and could double by 2050, driven by the decarbonisation of heat and transport.

Hence the clamour for connections, and reports that renewable projects are currently being given grid connection dates as late as 2037 or later.

To achieve the UK government’s target to connect to the grid 50 GW offshore wind generation by 2030, National Grid – the largest of the three UK transmission companies which own and operate the high voltage lines, including the London Power Tunnels – will need to materially ramp up investment.

The group will need to deliver at least five times more onshore transmission lines in the next seven years that it has delivered in the past 30 years and build four times more subsea cables than it currently owns.

Indeed, the scale of required investment in grids in many cases exceeds the funding capabilities of individual companies. In part that is why Scottish-based SSE – the other of the two UK-quoted transmission owners, the third being Iberdrola of Spain – recently sold 25% of its electricity transmission business to a Canadian pension fund investor.

Investment will also be required from the low carbon and renewable generation developers (wind, solar, nuclear, hydrogen-to-power and carbon capture technologies) and distribution network operators, who own the part of the grid between the high voltage lines and homes and businesses.

Although not on the same scale as transmission, much additional distribution network investment will be required to accommodate electric vehicle charging points, heat pumps, and smaller scale decentralised solar power and battery storage units.

Investment in the latter will better enable energy consumers to help manage the intermittency of renewables and/or sell electricity back to the grid at certain times.

Digging deep to unearth energy transition opportunities

National Grid plans to invest up to £40 billon for its five-year plan ending 2026. Around £29 billion, or more than 70% of this will be directly invested into the decarbonisation of energy networks, split roughly equally between the grid assets it owns in the UK and US.

Investment requirements for the next five-year period are likely to be even higher. This period will include the commencement of investment in 26 strategically important grid projects, among them a number of new high voltage lines to link up offshore windfarms, which are due to come on stream and whose connection to the grid are key to realising the government’s 50 GW target.

Further investment to accommodate the ScotWind (the next phase of the Scottish offshore windfarm developments) and Irish Sea offshore wind projects is yet to be costed.

Upgrading the UK grid is a huge task, but one where environmental and security concerns are likely to drive rapid change. It is also likely to create many investment opportunities for those willing to dig deeper and explore this less glamourous aspect of the energy transition.

The sectors, securities, regions and countries shown are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

—

Originally Posted June 1, 2023 – What “rewiring” an economy looks like, and what it means for investors

The views and opinions contained herein are those of Schroders’ investment teams and/or Economics Group, and do not necessarily represent Schroder Investment Management North America Inc.’s house views. These views are subject to change. This information is intended to be for information purposes only and it is not intended as promotional material in any respect.

Disclosure: Schroders

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realized. These views and opinions may change. Schroder Investment Management North America Inc. is a SEC registered adviser and indirect wholly owned subsidiary of Schroders plc providing asset management products and services to clients in the US and Canada. Interactive Brokers and Schroders are not affiliated entities. Further information about Schroders can be found at www.schroders.com/us. Schroder Investment Management North America Inc. 7 Bryant Park, New York, NY, 10018-3706, (212) 641-3800.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Schroders and is being posted with its permission. The views expressed in this material are solely those of the author and/or Schroders and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.