By: Iouri Saroukhanov and Joran Zoutendijk

Iouri Saroukhanov, Head of European Derivatives at Cboe Europe, and Joran Zoutendijk, Equity Derivatives Trader at Flow Traders, discuss the market structure differences between the U.S. and European futures markets.

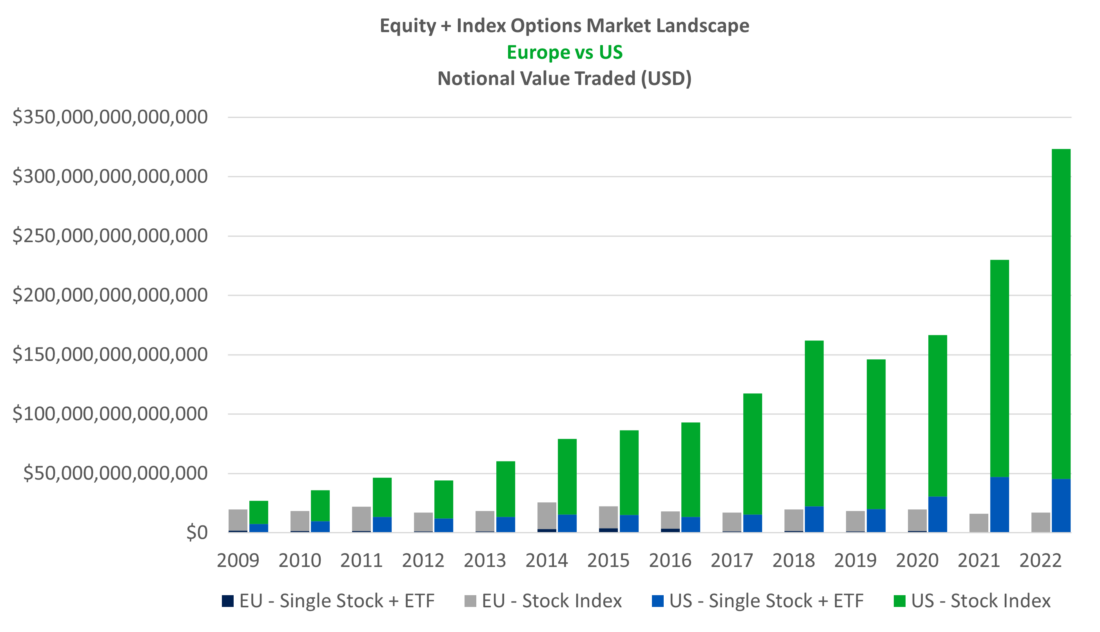

The highly liquid nature of U.S. derivatives markets, with multiple competing exchanges and participation from both the institutional and retail trading communities, has led to a steady increase in volumes over the last decade. By contrast, European activity has stagnated against the backdrop of a market structure which has limited on-screen liquidity and hasn’t attracted retail investors in the same way the U.S. markets have experienced. Cboe Europe Derivatives, a pan-European equity derivatives exchange was launched in 2021 to help bridge the gap between the two regions and systemically grow the European market.

Source: WFE, FIA, OCC and Cboe Global Markets data

Joran, how would you characterise the European equity derivatives market and why volumes have been subdued?

The European derivatives landscape is fragmented along national boundaries with several vertically integrated exchanges, each with their own regional products. The result is minimal competition and higher costs for participants that are looking to gain exposure to equities on a pan-European basis. Furthermore, much of the trading in European derivatives is pre-arranged and brought onto exchange for reporting purposes. This has resulted in limited on-screen liquidity and is historically what has dissuaded participants from entering the European market, particularly retail investors and those who are based in the U.S., accustomed to highly liquid markets.

At Flow Traders, we look at the markets as a whole. We leverage our expertise across cash equity and derived products, which enables us to provide liquidity on-screen through our tight bid/ask spreads and therefore providing that extra layer of transparency needed to grow the appetite in the European market. In addition, our algorithms and robust risk management allow us to add meaningful depth to the markets, accommodating retail and institutional flow. Given our focus, we believe that Europe is ready for further transition towards electronic markets and are encouraged at the efforts being made to improve the on-screen picture in European markets.

Iouri, how is CEDX attempting to improve European derivatives market?

One of CEDX’s key value proposition is that we are a genuinely pan-European marketplace. Through a single connection to CEDX and Cboe Clear Europe, participants can gain derivatives exposure to equites listed across all major European countries. Currently, participants have to connect to multiple different European exchanges and clearing houses for a similar level of exposure, which is inefficient, costly from an operational perspective and does not allow for optimisation of collateral. We enable participants to access a vibrant equity derivatives market through a single access point, creating efficiencies in connectivity, trading, clearing and market data. Our other big focus is on creating a deep and liquid on-screen market for European equity derivatives. A central limit order book sits at the core of the CEDX offering and is promoted through attractive incentive programmes and in-built protections for market-makers. Additional functionality, aimed at supporting price discovery and price improvement, include automated price improvement auctions (options market only), which guarantees a client a fill at a pre-agreed price, but allows for price improvement from competing participants.

CEDX is initially offering index derivatives based on select Cboe Europe Indices single country and pan-European indices. These indices are checked daily to monitor for compliance with CFTC and SEC rules on broad-based indices, ensuring they are eligible for qualified U.S. investors. This allows us to broaden our base of participants, promoting a diverse marketplace. We are expanding into pan-European single stock options later this year, subject to regulatory approvals.

Joran, how does the European market benefit from the CEDX offering and can you elaborate on the importance of a diverse set of participants in the market?

We very much view the CEDX exchange as a welcome addition to the European equity derivatives landscape. This exchange provides an opportunity for investors to improve the implementation of pan-European trading strategies and risk management procedures in a more cost-effective and efficient way.

The CEDX structure has lowered barriers to entry through lowering costs and improving connectivity efficiencies. As Iouri mentioned, all CEDX futures are based on indices that are monitored daily to ensure eligibility for qualified U.S. investors. These factors will help create a more liquid, diversified, and competitive market for European derivatives, ultimately benefiting all participants.

Iouri, how would you assess the development of CEDX to date?

We are happy with our progress to date. Volumes are growing – including record volumes in January – we are adding new participants and our price pictures continues to improve, particularly for index futures products. Overall, Cboe’s strong European cash equities presence – we are the largest stock exchange by market share – gives us a lot of credibility as we continue to build out our index contacts and prepare for the launch of equity options. Our cash equities market produces robust and high-quality market data which Cboe Europe Indices are based on. These indices are transparently designed and managed under a uniform set of rules and perform closely in line with comparable benchmarks. They are a highly cost-effective solution and from the participant point of view means we have a uniform set of index derivatives which are all designed the same way. It is important to reiterate that CEDX is at the start of its journey, it takes time for new initiatives of this type to gain traction and we are committed to making it work over the shortest timeframe possible.

—

Originally Posted March 20, 2023 – Cboe Europe Derivatives and Flow Traders Discuss European Derivatives Markets

Disclaimer: This information is not being provided as part of an offer or sale of any futures or options products to any persons located within the United States.

Disclosure: Cboe Global Markets

Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of Characteristics and Risks of Standardized Options. Copies are available from your broker, or at www.theocc.com. The information in this program is provided solely for general education and information purposes. No statement within the program should be construed as a recommendation to buy or sell a security or to provide investment advice. The opinions expressed in this program are solely the opinions of the participants, and do not necessarily reflect the opinions of Cboe or any of its subsidiaries or affiliates. You agree that under no circumstances will Cboe or its affiliates, or their respective directors, officers, trading permit holders, employees, and agents, be liable for any loss or damage caused by your reliance on information obtained from the program.

Copyright © 2023 Chicago Board Options Exchange, Incorporated. All rights reserved.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Cboe Global Markets and is being posted with its permission. The views expressed in this material are solely those of the author and/or Cboe Global Markets and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.