")

Suppose I laid out the following scenario: after an uninterrupted week of market gains it became apparent that the much-need fiscal stimulus talks are on life support, the Fed balance sheet continued to stagnate at levels seen for weeks, US-China tensions would rise, and a much watched economic number would modestly beat expectations. In a normal environment, one might expect some profit taking because three pillars supporting market valuation appear threatened. In this environment, the market chose to focus on the good news, as it has almost exclusively, and markets are roughly unchanged at this writing.

This poses a real conundrum for seasoned investors. We see markets rising and understand that the path of least resistance for a rising market is to continue its trajectory. We also know that markets are subject to bouts of vertigo at the least opportune moments. If investors are supposed to be fearful when others are greedy, what is one to do?

The simple answer is to consider hedging with puts. With VIX in the low 20’s, volatility is not nearly as expensive as it was earlier this year. That said, it is still not cheap, and not at the sort of low levels that we would consider complacent. Furthermore, skew is relatively steep, with levels similar to those that we saw in early February and late last year.

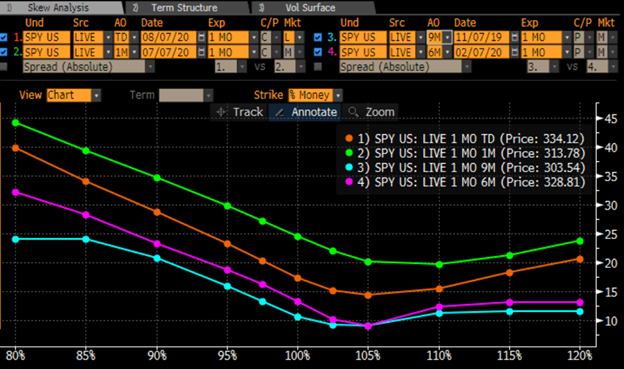

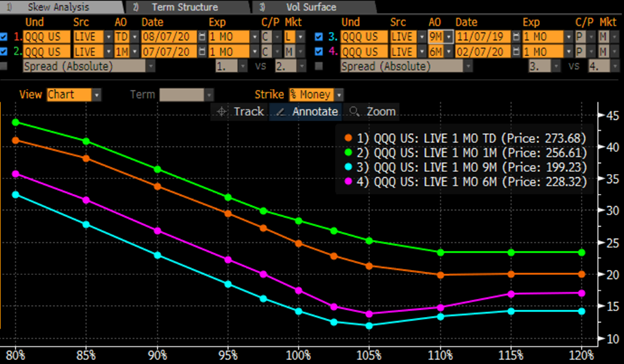

Source Bloomberg

The graphs above show the prices of options in SPY and QQQ at various levels of moneyness. We can see that in all cases, the shape of the curves is similar, with out of the money puts trading with implied volatilities above those of at money and out of the money calls. The interesting feature is that for the most part, the shapes of the curves at levels between 85-100% of the current price are roughly parallel. The skew is quite similar, meaning that the markets are willing to pay similar premia for downside put protection.

The bad news for hedgers is that it is not cheap to hedge. The good news for hedgers is that the magenta lines were from six months ago, when markets were pushing to new highs and ignoring the threat of the coronavirus. It means that some number of options investors were using puts to hedge a risk that few others considered.

To the extent that these put buyers were indeed savvy hedgers, their out of the money put strategy proved effective. They paid a relatively minor insurance premium to protect some of their gains. In today’s market environment, when good news is beloved and bad news shrugged off, it may be wise to consider pricing in a bit of fear while – or because – everyone appears greedy.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. Multiple leg strategies, including spreads, will incur multiple commission charges. For more information read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD) or visit ibkr.com/occ

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.