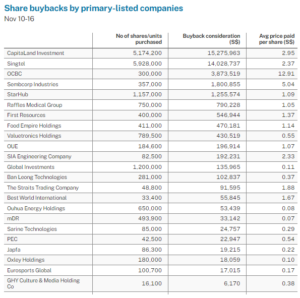

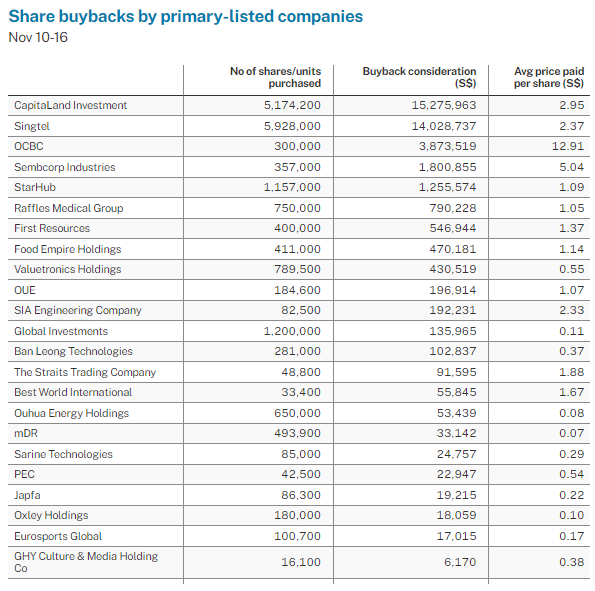

INSTITUTIONS were net sellers of Singapore stocks over the four trading sessions through to Nov 16, with S$198 million of net institutional outflow, as 24 primary-listed companies conducted buybacks with a total consideration of S$39.4 million.

CapitaLand Investment bought back 5,174,200 shares at an average price of S$2.95 per share on Nov 14. This took the cumulative number of shares purchased in the current mandate to 21,394,100 shares, representing 0.42 per cent of the company’s issued shares excluding treasury shares as of the mandate resolution date.

Digital Core Reit Management also bought back units of Digital Core Reit over the four sessions.

Leading the net institutional outflow over the four sessions were DBS, UOB, Singapore Airlines, Singtel, OCBC, City Developments, CapitaLand Ascendas Reit, Seatrium, Singapore Exchange and AEM Holdings.

Meanwhile, Genting Singapore, Sats, Venture Corporation, CapitaLand Investment, CapitaLand Integrated Commercial Trust, Keppel DC Reit, Keppel Reit, iFAST Corporation, Amara Holdings and Frasers Centrepoint Trust led the net institutional inflow over the four sessions. This saw consumer cyclicals and Reits lead the net institutional inflow over the four sessions, while financial services (including banks) and industrials led the net institutional outflows.

The four trading sessions saw close to 40 changes to director interests and substantial shareholdings filed for 25 primary-listed stocks. Directors or CEOs filed three acquisitions and no disposals while substantial shareholders filed two acquisitions and seven disposals.

AEM Holdings

On Nov 10, the deemed substantial shareholding of Malaysia’s Employees Provident Fund Board (EPF) in AEM Holdings crossed the 11 per cent threshold with a market transaction that saw 564,500 shares of the Catalist listed stock acquired at an average price of S$3.35 per share.

This followed on from the EPF’s deemed substantial shareholding in AEM Holdings crossing the 10 per cent threshold on Jun 21 and the 9 per cent level on Mar 2. Previously, the EPF’s deemed substantial shareholding in AEM Holdings crossed the 8 per cent mark in October 2022, exceeded the 7 per cent point in July 2022, and crossed the 6 per cent mark and 5 per cent substantial shareholder threshold in June 2022.

On Nov 9, AEM Holdings provided a Q3FY23 (ended Sep 30) business update and maintained the same FY23 guidance of between S$460 million and S$490 million provided with the H1FY23 results. The group has so far achieved revenue of S$387 million in the nine months of FY23 with a profit before tax margin of 2.6 per cent.

AEM Holdings attributed the slowdown in 9MFY23 revenue to overall sluggishness in the semiconductor industry, with most customers pushing out their capital expenditure related to testing to 2024 due to lower end demand across the industry.

On the strategic front, AEM has continued to invest in developing its suite of Test 2.0 innovations and capabilities. This has resulted in the group being awarded additional patents for its thermal capabilities in Q3FY23, and most of its customer engagements relate to next generation test requirements for advanced packaging chips used in high performance computing and AI.

The group also believes that the generative AI wave that gained momentum early this year, especially in the data centre space, is expanding to edge computing devices, increasing the overall transistor counts and architectural complexity.

It adds that these devices will face extreme test challenges that will translate into longer test times due to the increased test complexity and should provide long term tailwinds for the group’s Test 2.0 business. With regards to timing, the group believes demand for test solutions to address this market will be realised towards the end of 2024 and into 2025.

While ranking among the top 40 stocks by trading turnover this year, AEM Holdings has booked the twelfth highest net institutional inflows across the Singapore stock market.

Coinciding with the semiconductor downcycle, the past 12 months have seen the AEM Holdings’ share price decline by 10 per cent. This week the price-to-book ratio of AEM Holdings declined to 2.0x, compared to the average five-year price-to-book ratio of 4.0x which coincided with a 240 per cent price return.

Wing Tai Holdings

Wing Tai Holdings chairman and managing director Cheng Wai Keung has continued to build his deemed interest in the company, through his spouse Helen Chow acquiring shares. From Nov 10 through to Nov 16, Cheng has increased his deemed interest in the leading real estate developer and lifestyle retailer by 95,000 shares.

He maintains a 61.35 per cent total interest in the company. This has increased from 60.92 per cent, prior to Chow’s recent sequence of acquisitions that began on Sep 8. Cheng was appointed to the board of Wing Tai Holdings in 1973, and as managing director, the former chairman continues to play a pivotal role in the growth and success of the group’s business.

Wilmar International

On Nov 14, Wilmar International chairman and CEO, Kuok Khoon Hong, increased his deemed interest in the global agri-business from 13.49 per cent to 13.50 per cent. This saw Longhlin Asia acquire 200,000 shares and Hong Lee Holdings buy 200,000 shares and Jaygar Holdings acquire 100,000 shares. The 500,000 shares were all acquired at an average price of S$3.58 per share.

Kuok has been gradually increasing his total interest in Wilmar International from 12.94 per cent in October 2022.

MSM International

On Nov 15, MSM International (MSM) executive director and CEO Chan Wen Chau acquired 1.5 million shares of the Catalist-listed company at 2.8 cents per share. This increased his direct interest in the integrated metal engineering company from 2.85 per cent to 3.13 per cent. Acquired in a married deal, the transaction of 1.5 million shares represented the highest daily trading volume for the stock since 2010.

MSM offers a comprehensive suite of services spanning design, product development, prototyping, tool & die fabrication, production, and assembly.

Chan spearheads the expansion and growth of the group and is responsible for overall business and strategic development, corporate planning, operations, and management. Closely involved in all levels of operation of the group, he was appointed a director of the company in October 2009.

On November 9, MSM reported H1FY24 (ended Sep 30) revenue of RM44.0 million, an increase of 10.7 per cent from H1FY23. This was mainly due to the increase in revenue from the cleanroom and laboratories segment by RM4.6 million, offset with the decrease in revenue by F&B segment of approximately RM0.4 million.

The better performance of cleanroom and laboratories segment was due to resumption of few projects which were put on hold or postponed in the prior year. For its FY23, MSM recorded a 3.3 per cent improvement in revenue from FY22.

Through its 270,000 sq ft of specialised production space in Malaysia and Indonesia, MSM provides solutions to customers in Asia and Europe across the semiconductor, healthcare, food & beverage, and hospitality industries.

MSM’s business activities include OEM contract manufacturing, kitchen appliances, equipment, and related services, as well as cleanroom and laboratories. The group also operates a total of six showroom outlets occupying approximately 29,000 sq ft of floor space in Malaysia and Indonesia.

Beng Kuang Marine

On Nov 16, Beng Kuang Marine CEO Yong Jiunn Run acquired 200,000 shares at an average price of S$0.058 per share. With a consideration of S$11,600, this took his direct interest in the company from 4.19 per cent to 4.29 per cent.

His preceding acquisitions were on Aug 30 with 250,000 shares acquired at S$0.065 per share and on July 4, with 100,000 shares bought at S$0.07 per share. Yong’s responsibilities include making major corporate decisions, developing, and steering corporate plans, implement business directions and strategies for the group.

The group’s business strategy is oriented towards an asset-light and service-oriented business model, coupled with monetising fixed assets and deleveraging initiatives.

Its 51 per cent owned subsidiary, Asian Sealand Offshore & Marine (ASOM) specialises in asset integrity solutions for operating floating assets such as floating production storage and offloading vessels and floating storage and offloading vessels among others.

Targeting a larger customer base globally, ASOM has established itself as a proficient “one-stop” offshore in-situ turnkey solutions provider, leveraging sandwich plate system technology, to optimise and extend the life of such operating floating assets.

Inside Insights is a weekly column on The Business Times, read the original version.

Enjoying this read?

- Subscribe now to the weekly SGX My Gateway newsletter for a compilation of latest market news, sector performances, new product release updates, and research reports on SGX-listed companies.

- Stay up-to-date with our SGX Invest Telegram channel.

—

Originally Posted November 20, 2023 – Malaysia’s EPF lifts its stake in AEM to 11 per cent

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Singapore Exchange and is being posted with its permission. The views expressed in this material are solely those of the author and/or Singapore Exchange and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.