When it came to writing about Nvidia (NVDA) yet again, part of a quote from “Caddyshack” came to mind: “I didn’t want to do it. I felt I owed it to them.” But after a period of intense pre-earnings discussion and a subsequently astounding relief rally, a wrap-up discussion seemed appropriate.

Over a week ago we alerted readers that NVDA earnings would be a market-moving event. That part is evident from today’s rally. We were concerned that it would take a huge beat and raise for the stock not to fall, and NVDA delivered. It is indeed a reason to celebrate, as this morning’s 15% rally shows.

In case you were wondering why NVDA is inextricably linked to artificial intelligence, listening to yesterday’s earnings call should have more than satisfied your curiosity. I counted 67 uses of the term “AI” before the first question was asked. After the year-ago conference call, I found it telling that they used the term 37 times before the first question. That’s a bit less than doubling in a year. On the other hand, the stock is up nearly fourfold since then!

Even though I warned that there was more risk to the downside – and I still believe that a shortfall would have resulted in an even bigger move than today’s upswing – it wasn’t something I was hoping for. I don’t want to be perceived as rooting against our customers, but I think that every investor does himself a huge disservice if he fails to be aware of risks in both directions.

Always keep this fact in mind: no one should ever want their insurance to pay off! We all need to be wary of fire or floods that could damage our homes, illnesses that could damage our well-being, or the risk of accidents that could damage our cars, and we all carry insurance to mitigate the financial effects of those risks. But are any of us ever angry that we didn’t put in a major insurance claim in a given year? Of course not. The same mentality should apply when one hedges major market risks.

It’s important to keep in mind that I believe that my initial piece and a subsequent TV visit raised a set of risks that were not being considered at that time. By yesterday morning, this was a mainstream topic of market conversation. As a result, the stock price reflected the risk.

Bear in mind that the stock had fallen 10% from just after the start of trading on Friday until about 3pm yesterday. Paradoxically, that balanced the risks ahead of the earnings report. While the current NVDA price is well above last week’s prevailing levels, the intervening dip reflected a more widespread concern about the potential for a market-moving result. That the Cboe Volatility Index had been trading in the 15-16 level ahead of the earnings report also reflected perceptions about the broader risks inherent in an NVDA shortfall.

So, what’s next for NVDA specifically and the AI trade in general? It’s a tricky call because this is now perhaps the ultimate FOMO – maybe even “weaponized FOMO.” It’s awfully tempting to jump onto the bandwagon, and a treacherous trend to fight.

An institutional manager who is underweight NVDA, and peers like SMCI and AMD, is suffering. Many will be incentivized to chase. Remember, FOMO reflects career risk for institutional investors. None of them want to risk underperforming their benchmark or their peers. As for individuals, however, FOMO is more about greed than actual fear. No one wants to miss a rally, but that’s frustrating, not a career-threatening. The decision for all investors needs to be about balancing risk and reward, and chasing a stock that is up 15% in a day does involve a fair amount of risk. It’s up to each investor to know their own tolerances.

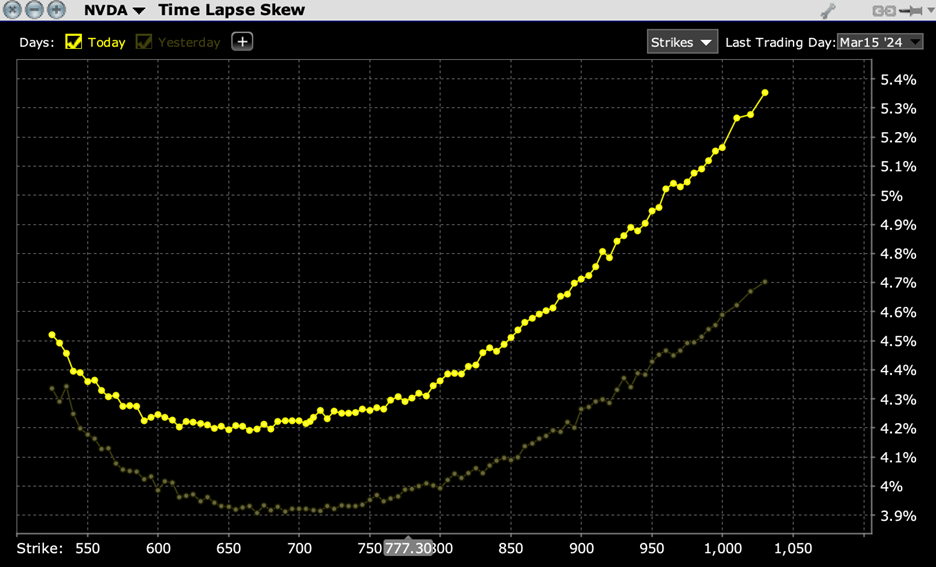

One way that both sets of investors are dealing with the situation is to buy calls rather than the stock itself (though of course, PLENTY are buying the shares!) The calls aren’t cheap, but they have limited downside and leveraged upside. This demand is reflected in an unusual skew in NVDA options. Normally we see above-market options trading at lower implied volatilities than below-market options. That is because there are typically natural sellers of calls (covered call writers) and demand for protection from hedgers. In the case of NVDA, we see the opposite – above market options are generally much more expensive. That means there is greater demand than usual for speculative calls.

NVDA Skew for Options Expiring March 15th, 2024, Today (bright yellow) vs. Yesterday (fainter yellow)

Source: Interactive Brokers

At least so far, today’s advance is truly a tech-driven rally. A 1.75% rally in SPX would normally be accompanied by advancing stocks far outpacing decliners. Right now it’s about 2:1. And the Russell 2000 (RTY), which has recently been about 2X as volatile as SPX (up and down) is a big laggard this morning. It’s NVDA’s market, and we’re all living in it.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.

Leave a Reply

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Hi Steve _ As per usual an insightful article. However NVDA’s Earnings of 22B were NOT spectacular as they measure against the expected Earnings (20.8B to a Whisper of 24B). nor was the Forecast of next Q of 24B. They were good of course but not spectacular given that the stock price had already reflected 21 to 25B.

Interesting that the stock dove down (as did all other Tech stocks) when earnings were released, from 670 to 640……BUT THEN…..someone / Org started to BUY…and BUY and BUY…and the rest of the market followed. Very Strange….very. Not a 1st World market anymore. Approaching a 3rd World market.

The day before market moving days like today (NVDA release) are the perfect time to set up delta neutral trades (sell the stock and buy calls or buy the stock and buy puts). If you wish to continue the trade beyond today simply rebalance the delta or if you are experienced enough – – rebalance by selling nearby options against a part of the long option position to create a part of your position as either a diagonal spread or calendar spread. Then you can continue to trade the delta neutral trade but without time premium loss (theta positive or neutral).

The QQQ options and stock are especially useful for delta neutral trades if you plan to short the stock and buy calls as there is less dividend to pay on the short stock when compared to SPY (if you plan to trade the position through the ex dividend date).

huh. hmm.

I wonder how much of this rally is driven by foreign investors? For example, I understand that many Chinese investors are leaving the domestic market and buying ETFs which track US stocks. Many have lost confidence in their government’s management of their economy and are pulling out. I don’t know how to quantify it, but might help explain exceptionally high valuations. If the future looks bleak at home, why not roll the dice on something (AI & NVDA) that may be promising?

Earnings are real. What no one knows is how the AI chips will result in profit for those companies who are buying the chips. Ultimately, every company is dependent on the consumer. I get nervous when the CEO of a high flying company hypes his business. My instincts say the NVDA earnings explosion will slow as the low hanging fruit is exhausted. Good for those who own it but one of the most speculative stocks since the internet bubble.

NVDA = Cyberdyne Systems in their early days?… 🙂 “I’ll be back.” And Arnold aboard the HD Fatboy totally sold out orders for that bike back in the day. And if NVDA begins a pilot project called …. hmmm…. Skynet? Lookout!! 🙂