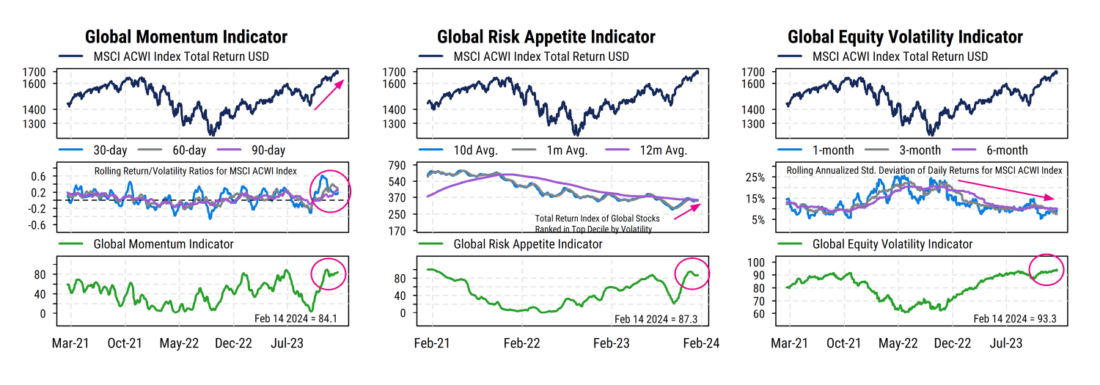

Staying in line with the trend in markets has long been shown to be useful for allocation and risk control, which is why we include trend-oriented indicators in the Global Equity Risk Model we use as the anchor for our 1-6 month stock/bond (and general “risk on/risk off”) allocation views.

Perhaps even more important is our underlying view that having multiple indicators aligned and confirming tends to produce better results than any individual indicator could on its own. That is why the Equity Risk Model incorporates eight indicators rather than trying to rely on any single “best” indicator alone.

Three of those indicators are shown in the charts below and tell us:

- that the intermediate-term trend in major equity indices (we use the global MSCI ACWI index) is quite strong

- riskier (higher volatility) stocks are rising and outperforming, a sign of risk appetite

- Overall equity index volatility (which tends to be persistent) is low

The alignment of these three equity price-based indicators has historically been bullish for the near-term (1-3 month) outlook for stocks.

Source: Mill Street Research, Factset

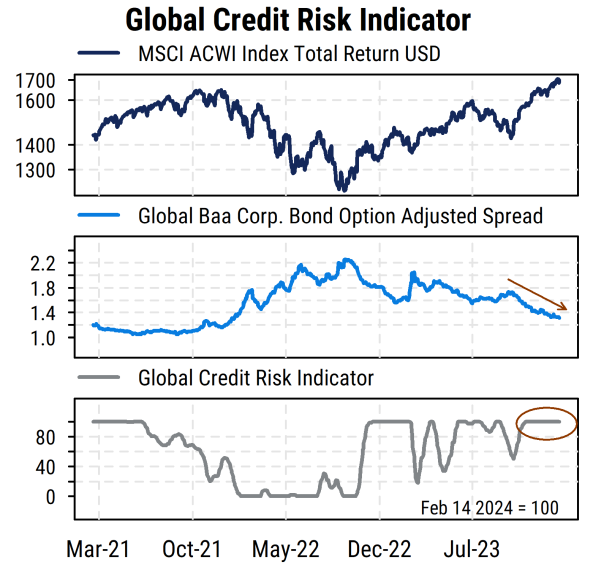

We can then look for corroboration outside of equities to see if credit investors are showing similar behavior, or if they are contradicting the equity signals. As shown in the chart below, credit spreads on global Baa-rated corporate bonds continue to contract. This is a sign that corporate debt investors are also willing to take on more risk (i.e., require less additional yield over risk-free government bonds) and do not see reason to expect corporate fundamentals (ability to meet debt obligations) to get worse in the near-term.

Source: Mill Street Research, Factset

Credit spreads, like most sentiment indicators, can go too far and become a concern. Thus far, spreads have been declining from earlier elevated levels and have not reached historically low readings like we saw in 2021. With no signs of an upturn in spreads thus far, our indicator remains bullish.

Momentum = FOMO

When investors have been too cautious and then strong uptrends develop, the psychological impact for investors (particularly those needing to beat a benchmark) is “FOMO”, or Fear Of Missing Out on the gains. This can make the trend persist longer than expected, which is why waiting for a break in the trend as a signal to reduce exposure tends to be less risky than trying to “pick the top”, even if it means giving back some fraction of the maximum gains from a peak.

The discipline of our indicators thus argues for staying with the trend by remaining overweight equities for now.

What about the fundamentals? And haven’t stock prices gone too far?

As we get slightly further into 2024, the data suggests that underlying fundamentals for the US economy and corporate earnings remain reasonably good. Notably, though, this is (still) true more for large companies than small companies, and conditions outside the US are not nearly as strong.

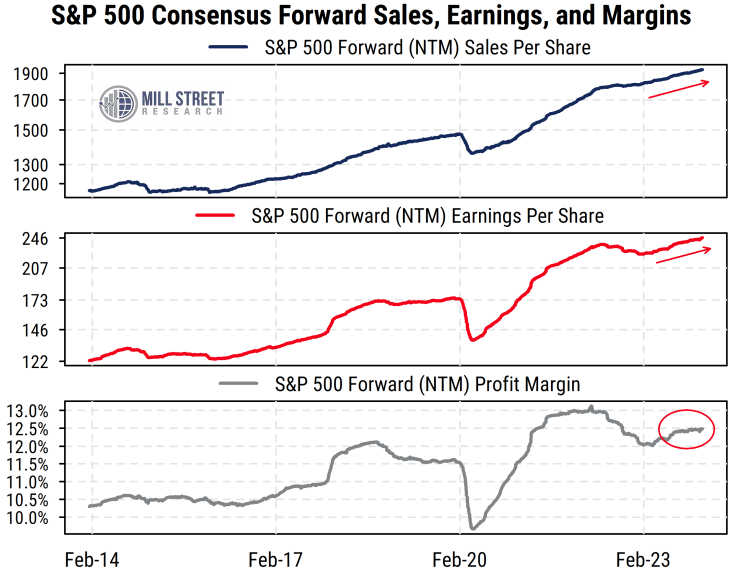

Looking at the S&P 500 data (i.e., US large-caps), we can see in the top section of the chart below that forecasted top-line sales per share over the next 12 months (NTM) continue to rise steadily. This contrasts, for instance, with the 2015-17 period when sales estimates were flat to down.

Earnings forecasts, though always more volatile, are following a similar path. Forecasted EPS for the S&P 500 continue to make new all-time highs (middle section). It is worth noting that the S&P 500 trends stand in contrast with the European STOXX 600 index EPS forecasts, which have been flat to down recently as Europe’s economy lags that of the US.

Crucially, forecasted profit margins for the S&P 500 have rebounded from the 2022 pullback and are largely steady lately not far from their own highs. It looks more like margins are holding at meaningfully higher levels than in the mid-2010s, and thus may be a reason for some of the valuation expansion in the S&P 500 recently. The steady margins are notable given that interest rates have been higher (i.e., 5-6% rates on typical Baa-rated corporate debt, versus rates of 2-2.5% in 2021) for well over a year now.

So if the top line and bottom line are still growing and rates are not slowing the economy much thus far, the more visible risk to markets may be less about the fundamentals and more about investor sentiment.

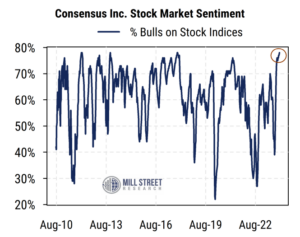

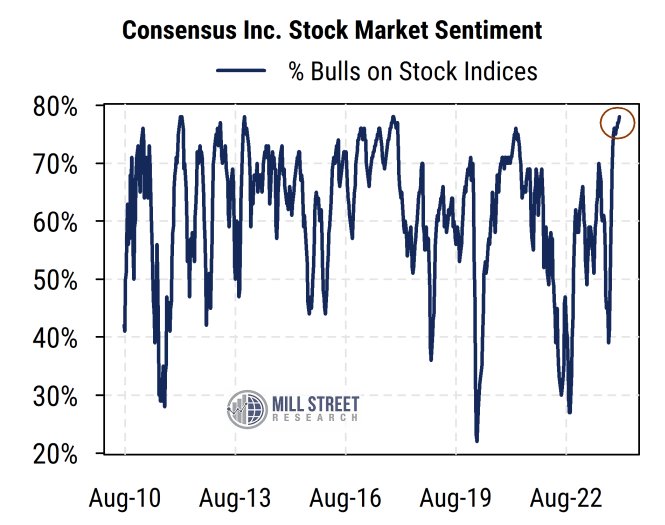

Even if the fundamental news is indeed good, any amount of good news can be eventually priced in and make stocks riskier. While valuations for stocks are certainly higher, they are not yet excessive in our view, but sentiment surveys like the ones from Consensus Inc. show a historically high level of bullishness among market watchers (chart below).

Source: Mill Street Research, Consensus Inc.

The latest reading of 78% bulls matches the peak readings since 2010, though high readings can persist for weeks at times in a strong trend. High sentiment can be followed by consolidation or mild corrections, or something worse if fundamentals deteriorate. Thus far, the downside looks more limited and the uptrend in equities could go on a while longer, but sentiment by some measures is now roughly the opposite of the late 2022 low readings. In other words, it is likely going to harder to get “better-than-expected” news now than it was a year ago since expectations are higher.

—

Originally Posted February 15, 2024 – TREND (AND FOMO) IS STRONG BUT SENTIMENT IS GETTING STRETCHED

Disclosure: Mill Street Research

Source for data and statistics: Mill Street Research, FactSet, Bloomberg

This report is not intended to provide investment advice. This report does not constitute an offer or solicitation to buy or sell any securities discussed herein in any jurisdiction where such offer or solicitation would be prohibited. Past performance is not a guarantee of future results, and no representation or warranty, express or implied, is made regarding future performance of any security mentioned in this report.

All information, opinions and statistical data contained in this report were obtained or derived from public sources believed to be reliable, but Mill Street does not represent that any such information, opinion or statistical data is accurate or complete. All estimates, opinions and recommendations expressed herein constitute judgments as of the date of this report and are subject to change without notice.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Mill Street Research and is being posted with its permission. The views expressed in this material are solely those of the author and/or Mill Street Research and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.