We see an enormous opportunity for companies making a direct contribution to the circular economy, but investors must take care to focus on those companies genuinely enabling the transition.

The transition to a circular economy means moving from the existing “take-make-waste” economic model, to an approach that designs out waste and pollution to keep materials in use. It is driven by the urgent requirement to improve resource efficiency, as well as the need to rapidly decarbonise the global economy.

Accenture estimates that the resource gap (the difference between supply and demand) opening up over the coming decades will create a $25 trillion opportunity by 2050 for circular economy business models. This means there are a lot of opportunities for investors to aim at.

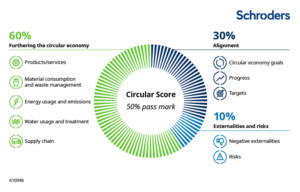

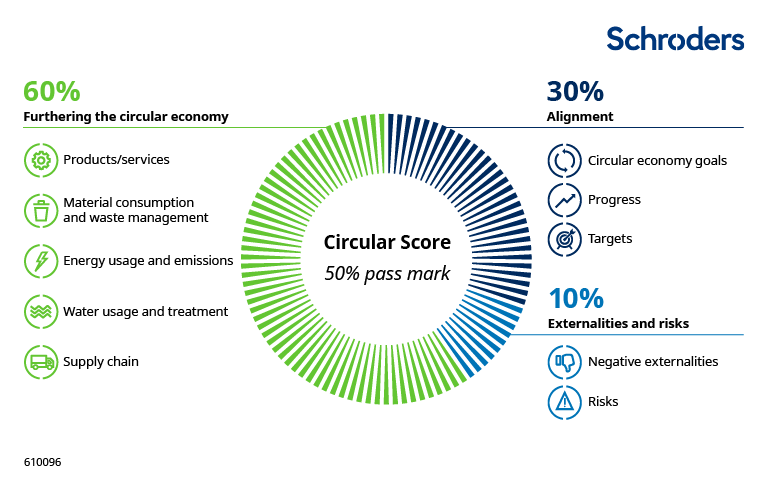

But the best opportunities will be those that are genuine pure plays on the circular economy. We have developed a unique “Circular Score” approach to assessing a company’s circular economy credentials.

As circular economy investors, we want to focus only on these opportunities and our Circular Score approach helps to ensure this. Using this approach, we’ve found that Microsoft and other big tech companies don’t make the cut.

Focus on pure plays, not “good citizens”

We see pure play circular economy firms being able to tap into the trillions of dollars of opportunity over the coming years by helping to close the resource gap. “Good citizens” are more likely to be buying the products/services of our pure-plays than tapping directly into the resource gap opportunity.

We class the likes of Microsoft as a “good citizen”. The company is doing great work on emissions reduction, recycling waste and old electronics from its data centres, as well as investing hundreds of millions of dollars into a climate innovation fund.

But in terms of their Circular Score, Microsoft fails our assessment because the products and services it sells don’t enable or contribute to the circular economy in a direct manner. Microsoft sells software and cloud services (along with other business lines like Bing, Xbox, tablets etc.). These aren’t circular economy enabling products nor are they driven directly by the need for a circular economy.

This is not to say that Microsoft is not a good investment; it clearly has been in the past and has the characteristics of a business that could continue to be in the future.

The same “good citizen” perspective applies to other companies adopting some circular economy best practice. For example, many fast-moving consumer goods companies (FMCGs – often food & beverage or personal care firms) are introducing higher levels of recycled content and other recyclable materials for their packaging. But we don’t view these as pure plays on the circular economy either.

The issue is that these companies don’t see their revenue and profits grow as a result of the adoption of these circular practices. It’s not clear to us that, for example, consumers buy more soft drinks or make-up due to higher recycled plastic content in packages. We anticipate greater opportunity in the companies providing the solutions to solve FMCG firms’ circularity challenges.

These types of companies don’t form part of the universe of stocks that we see benefitting from the circular economy growth theme. And we don’t feel the need to expand our universe to “good citizens” given the size of the opportunity ahead for the pure play winners.

Our Circular Score approach ensures differentiated exposure to a long-term growth theme

We can imagine most investors already have high exposure to the likes of Microsoft and other “mega-cap” companies. These dominate not just the global stock market indices but also many sustainability (including circular economy) and growth funds.

Our approach of assessing every company we invest in through the lens of our proprietary Circular Score helps to ensure investors are getting diversified exposure to a differentiated secular growth theme.

These companies will be the authentic circular economy winners that we believe will see accelerated growth and enhanced cost control from embedding circular practices in their operations. It gives us confidence as investors to put capital behind companies with such a strong tailwind in their sails.

Our approach leads us to a greater focus on the smaller and mid-cap parts of the market, rather than the mega-caps who tend to be more in the “good citizen” bucket. These firms tend to be more directly geared into the structural growth trend of the circular economy and are what excites us about the opportunity given we believe these are “underfished”, or lesser-known, waters.

—

Originally Posted October 24, 2023 – Why Microsoft doesn’t make the cut as a circular economy stock

Disclosure: Schroders

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realized. These views and opinions may change. Schroder Investment Management North America Inc. is a SEC registered adviser and indirect wholly owned subsidiary of Schroders plc providing asset management products and services to clients in the US and Canada. Interactive Brokers and Schroders are not affiliated entities. Further information about Schroders can be found at www.schroders.com/us. Schroder Investment Management North America Inc. 7 Bryant Park, New York, NY, 10018-3706, (212) 641-3800.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Schroders and is being posted with its permission. The views expressed in this material are solely those of the author and/or Schroders and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.