Excerpt

Introduction

Our main goal in Quantpedia is to broaden the horizons of our readers in the field of systematic investing and quantitative trading. We do not aim to sell trading signals but to inspire and give fresh ideas, of how to invest limited time and resources on quantitative research. Clients can adopt trading strategy ideas derived out of academic research or further adapt them to their needs and requirements. But the best course of action is to try fundamentally understand anomalies and explore their functioning besides the original scope of the academic research papers. The following article is one such example of how can our readers get inspiration for a strategy and further modify or improve it according to their desire.

Skewness across asset classes

Based on the idea of Skewness in Commodities, we have decided to follow in steps of an additional paper written by Nick Baltas and Gabriel Salinas: Cross-Asset Skew and test, whether the Skewness effect can be used to profit from also in other asset classes, and how can the presented strategy be further enhanced. So let’s check whether a similar trading strategy could also be applied for currencies, equities and bonds.

Skewness in currencies

Our investment universe for testing the skewness effect in currencies consists of 8 CME futures contracts on the following currencies: AUD, GBP, CAD, EUR, JPY, MXN, NZD, CHF. Our dataset started in December 2006, and we have decided to follow the exact same strategy, as proposed in the first-mentioned paper (Fernandez-Perez at al.).

First of all, the skewness of returns has to be calculated for each trading day. In our test, we have calculated the skewness for day t based on the daily return of day t and daily returns of previous 259 trading days, which gives us approximately a yearly lookback period. Then we assess the skewness data of the last trading day in a month t-1, to create a portfolio in month t. Based on the assessment, we open a short position in two currencies futures with the highest skewness and long position in two currency futures with the lowest skewness on the first trading day of the month t. The portfolio is equally-weighted and held to the first trading day of month t+1 when its rebalanced according to the new skewness data. As the first skewness data are available at 12/31/2007, our trading sample starts from January 2008 and ends on May 2020. The presented strategy gained an annual return of 1,76%, with 8,87% yearly volatility, which gave us a 0,20 Sharpe ratio.

Skewness in equities

For equities, we have decided to test this effect with the same approach, as for currencies. Our equity investment universe is represented by futures contracts on eight different stock market indices: NASDAQ, DAX, S&P 500, SMI, EURO STOXX 50, CAC 40, FTSE 100 and Nikkei 225. Our data sample starts in June 1999, with the first skewness data available at 06/30/2000. Therefore, our trading sample starts in July 2000 and lasts until May 2020. Using the exact same strategy with going long on two instruments with the lowest skewness and short on two instruments with the highest skewness, the investor would achieve an annual return of 0,96% with equally-weighted portfolio. The annual yearly volatility reached 11,34%.

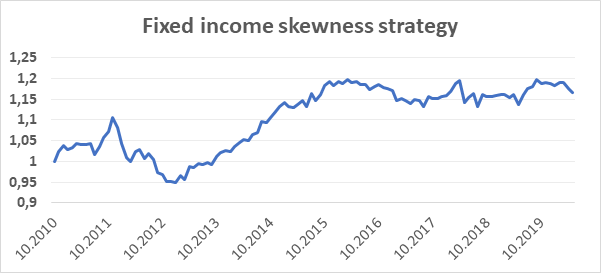

Skewness in fixed income

Finally, we have decided to test the same strategy also for fixed income assets. In our test, fixed-income assets are represented by seven different 10Y bonds futures. Our data sample begins in September 2009, meaning that first skewness data to be used are available at 10/29/2010. Our trading sample then begins in November 2010 and ends with May 2020. Since our universe consists only of 7 different instruments, the division into quartiles could not be followed exactly. Still, we decided to use the same principle: open long positions in the two bonds futures with the lowest skewness in returns and open short positions in the two bonds futures with the highest skewness. This time, the strategy would earn us an annual return of 1,62% with equally-weighted portfolio. With the annual yearly volatility at 4,78%, the strategy provides 0,34 Sharpe ratio.

Visit Quantpedia website to read the full article:

https://quantpedia.com/multi-asset-skewness-trading-strategy/

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Quantpedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Quantpedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Forex

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.