Excerpt

Trend-following funds and strategies were once extremely popular after the 2008/2009 crisis. They offered attractive performance, and diversification properties made them a nice addition to investor’s portfolios. Ten years later, “trend-following strategy” is not such a popular word. Strategies didn’t blow-up, but their performance was far from spectacular. What are the main reasons for that? Is it an increased correlation among markets? Are trend rules inefficient? An important recent academic study written by Babu, Hoffman, Levine, Ooi, Schroeder, and Stamelos (all from AQR Capital Management) analyzes trend-following performance for each decade in the last 140 years and uses three distinct factors: the magnitude of market moves, the efficacy of trend-following strategies at capturing profitability from market moves, and the degree of diversification across trends in a trend-following portfolio. They show that it’s the first factor (a lack of large risk-adjusted market moves, positive or negative) that had the biggest impact in the last decade.

Authors: Babu, Hoffman, Levine, Ooi, Schroeder, and Stamelos

Title: You Can’t Always Trend When You Want

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3487134

Notable quotations from the academic research paper:

“Our approach builds on the trend-following strategy as defined in Hurst et al. (2013, 2017) and uses data from the late 1800s through 2018. The markets considered include: 29 commodities, 11 equity indices, 15 bond markets, and 12 currency pairs. For each of the markets described above we construct 1-month, 3-month and 12-month time series momentum signals. The three signals are then equally weighted. Positions are sized according to their expected volatilities and then scaled in aggregate such that the portfolio maintains a 10% ex-ante annualized volatility target.

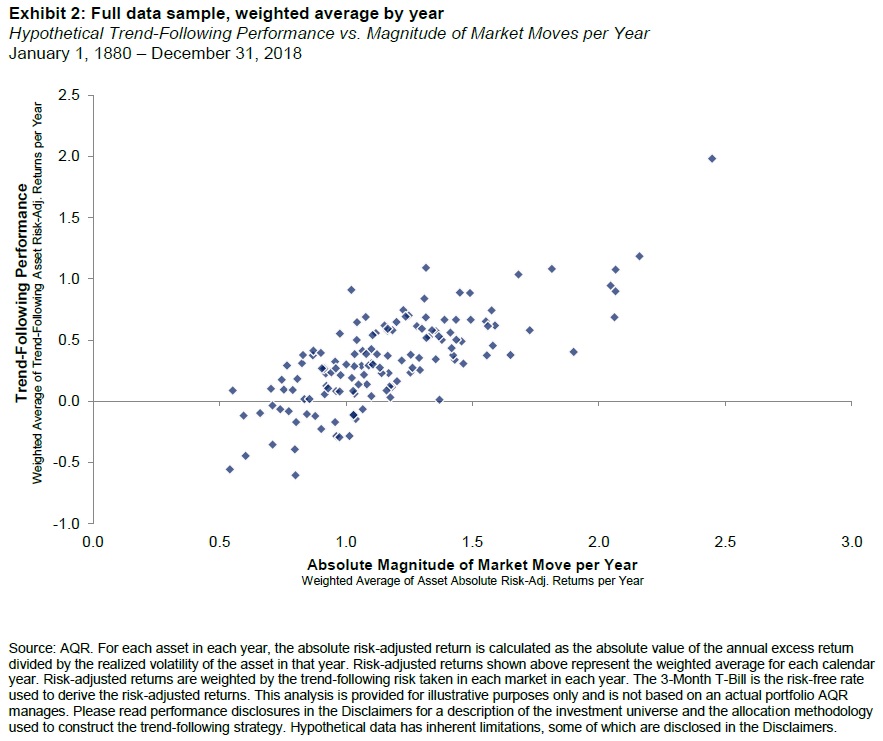

Exhibits 1 and 2 show there is a clear historical positive relationship between the absolute magnitude of moves in individual markets and the risk-adjusted returns of a hypothetical trend-following strategy.

Visit Quantpedia to read the full article:

https://quantpedia.com/why-did-trend-following-underperform-in-the-last-decade

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Quantpedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Quantpedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.