Excerpt

Federal Open Market Committee meetings (aka FED meetings) have a significant influence on the number of different assets (see for example our article related to drift in equities during FED meetings). The main channel which FED uses to influence the US economy is the level of short term interest rates. Therefore, it’s not a surprise that FED meetings have influence also on long-term interest rates. But just how big? Bigger than most people think. We are presenting one interesting research paper written by Sebastian Hillenbrand, which shows that the whole secular decline in equity yields and long-term interest rates since 1980 was realized entirely in a 3-day window around FOMC meetings. Now, that’s called the influence …

Author: Hillenbrand

Title: The Secular Decline in Long-Term Yields around FOMC Meetings

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3550593

Abstract:

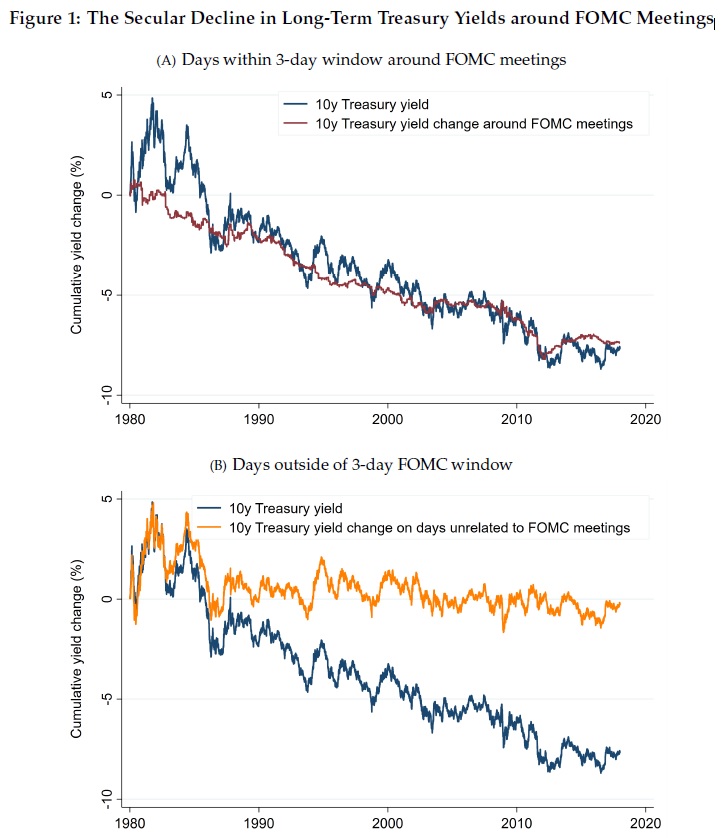

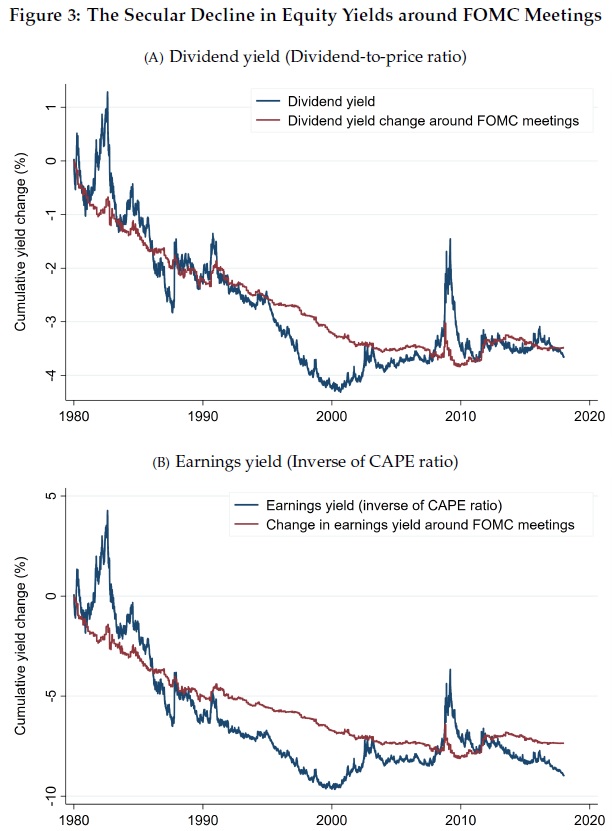

Long-term U.S. Treasury yields fell by almost 8% between 1980 and 2017. I document that the entire decline in long-term interest rates was realized in a 3-day window around FOMC meetings. I find a similar pattern for U.S. equities: the same 3-day window can account for the entire decline in equity yields over the same time period. Decomposing the decline into an expected short-rate and a risk premium component, I find that the fall in long-term yields around FOMC meetings can be mostly attributed to a lower expected path for the future short rate. I argue that these results are surprising in light of theories on monetary policy and the secular decline in interest rates.

Notable quotations from the academic research paper:

“There was a large and persistent decline in long-term yields over the last four decades. The 10-year U.S. Treasury yield decreased from 10.1% at the beginning of 1980 to 2.4% at the end of 2017. During the same time period, the S&P 500 dividend yield fell by 3.7% and the S&P 500 earnings yield by 9.0%.

While the secular decline in long-term yields has important consequences, it is hard to empirically determine its cause. Several theories exist which address the secular decline in interest rates. According to the most prominent explanations, the decline is associated with the idea of secular stagnation and the savings glut – the notion that there is excess savings demand driving down interest rates.

Visit Quantpedia to read the full article:

https://quantpedia.com/secular-decline-in-yields-around-fomc-meetings/

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Quantpedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Quantpedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.