![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-700x394.jpg.webp "[Gamma] Scalping Please")

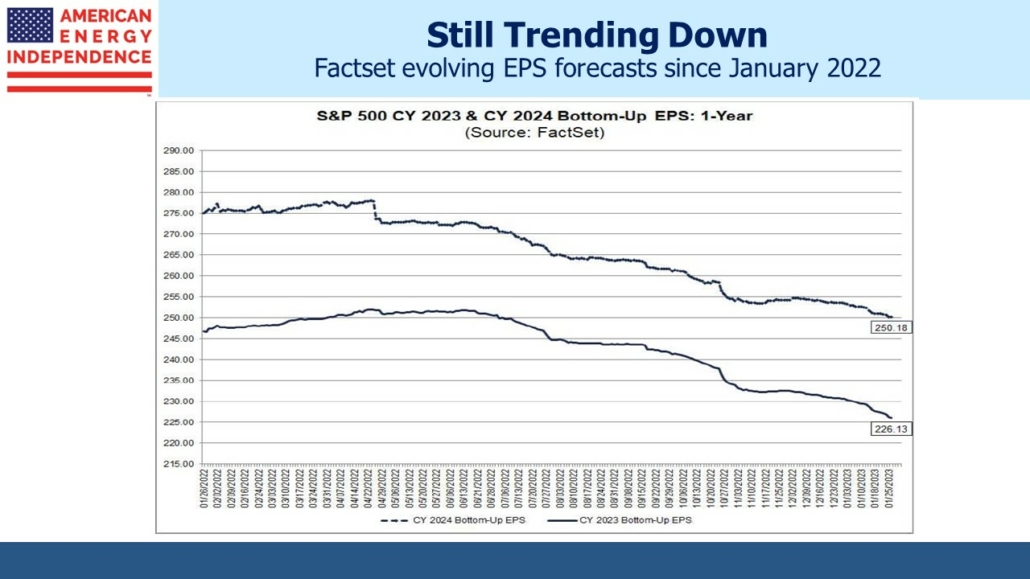

The Fed’s mid-week policy meeting will punctuate a busy earnings week. Sell-side analysts continue to ratchet down earnings forecasts. Factset reports bottom-up 2023 earnings expectations of $226, down over 10% compared with last spring when Fed tightening started to have an impact.

Energy continues to be a bright spot, providing positive surprises in 4Q earnings released so far. Companies continue to return capital to shareholders. Chevron tripled its planned buybacks to $75BN over the next five years, drawing more economically illiterate criticism from the White House for not plowing this money into increased production. Incoherent energy policies and fair-weather friendship aren’t inducing Chevron CEO Mike Wirth and other energy executives to alter their capital allocation.

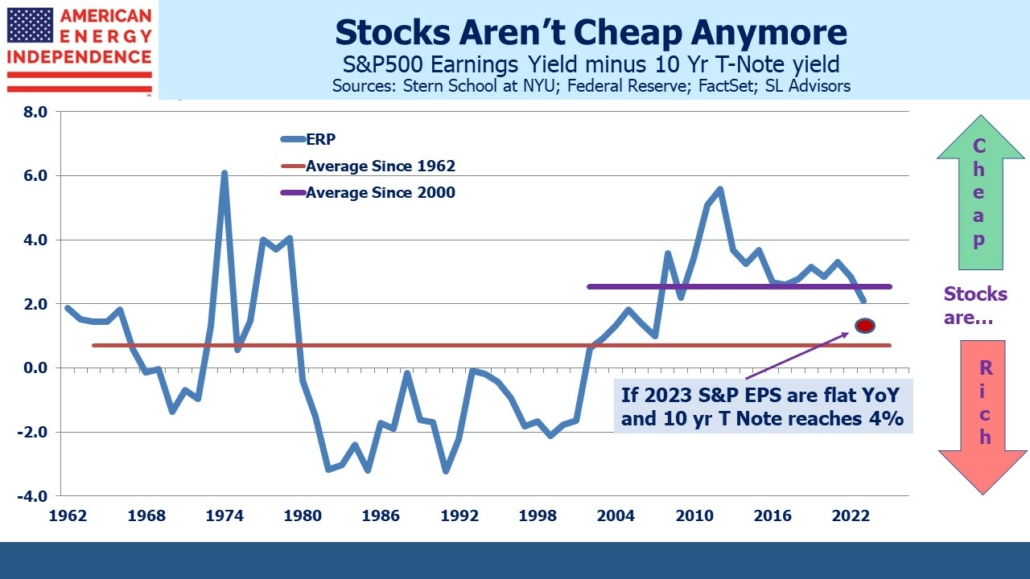

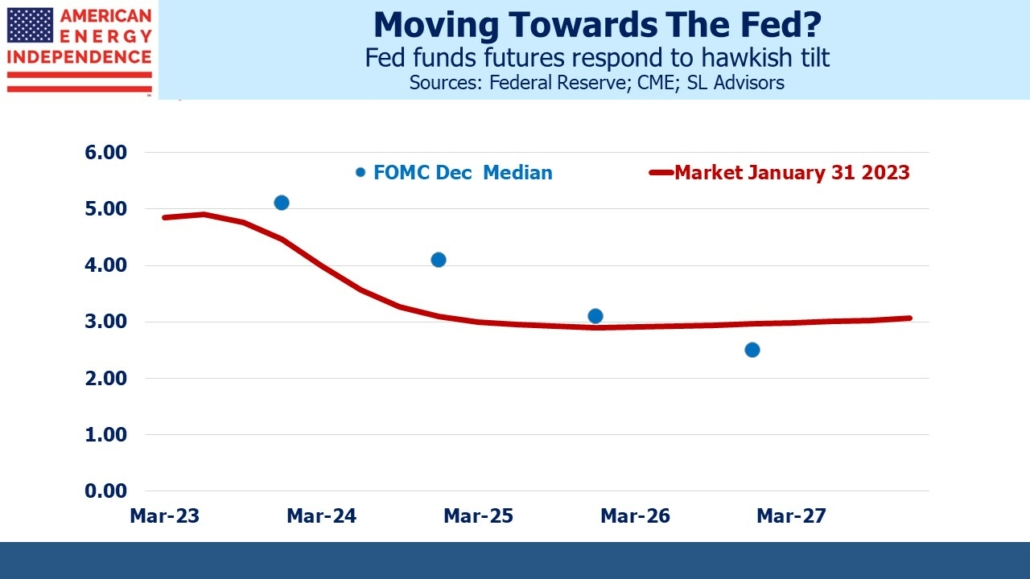

The broad equity market isn’t cheap, based on the Equity Risk Premium (ERP). Stocks are vulnerable to higher interest rates. Fed funds futures project a peak in Fed policy this summer with rates coming down later this year. By contrast, the FOMC Summary of Economic Projections (SEP) released on December 14 pushes that scenario back around a year.

Fed funds futures six to twelve months out differ as much as 1% from the FOMC. Data since the last SEP has been on balance slightly weaker. So a surprising move in futures to more closely align the two would leave the stock market vulnerable, especially given the trend towards weaker earnings forecasts.

Morgan Stanley strategist Michael Wilson is cautious because of the Fed outlook, although Robert Kad, who heads up their MLP and Energy Infrastructure research, is gloriously bullish on his sector.

Midstream energy infrastructure should be resilient to higher rates. Yields of 5-6% are already attractive, but more important is the embedded inflation hedge that is in many pipeline tariffs. Inflation expectations remain low considering recent history. Risk here is also skewed to the upside. Wells Fargo has estimated that half the industry’s EBITDA is linked to inflation protected contracts.

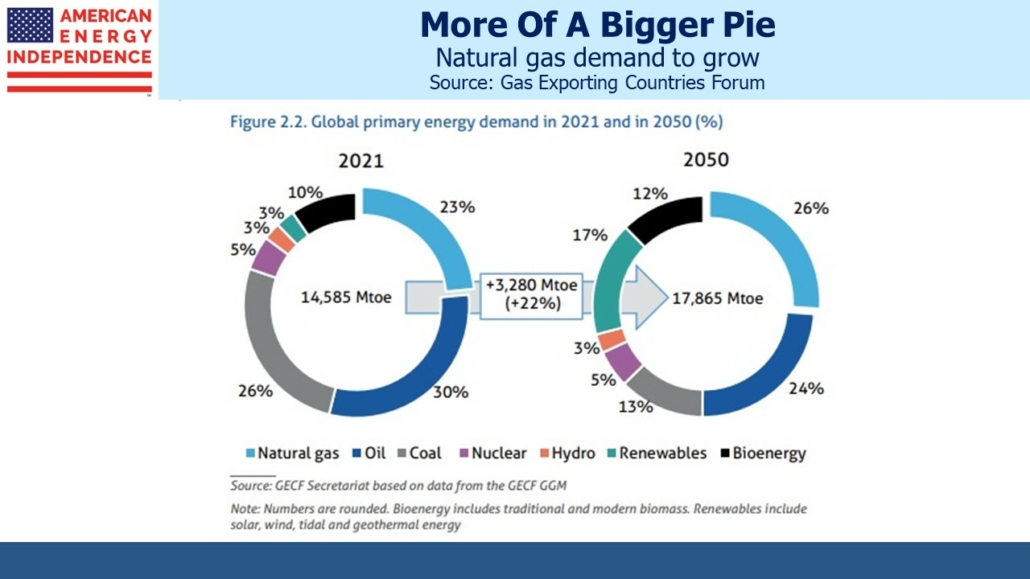

European demand for LNG imports jumped last year, but over the long-term emerging economies are likely to grow consumption. The Gas Exporting Countries Forum expects natural gas to increase market share from 23% to 26% by 2050 while global energy demand increases at 0.7% pa. Thanks to Stephen Stapczynski of Bloomberg for pointing this out.

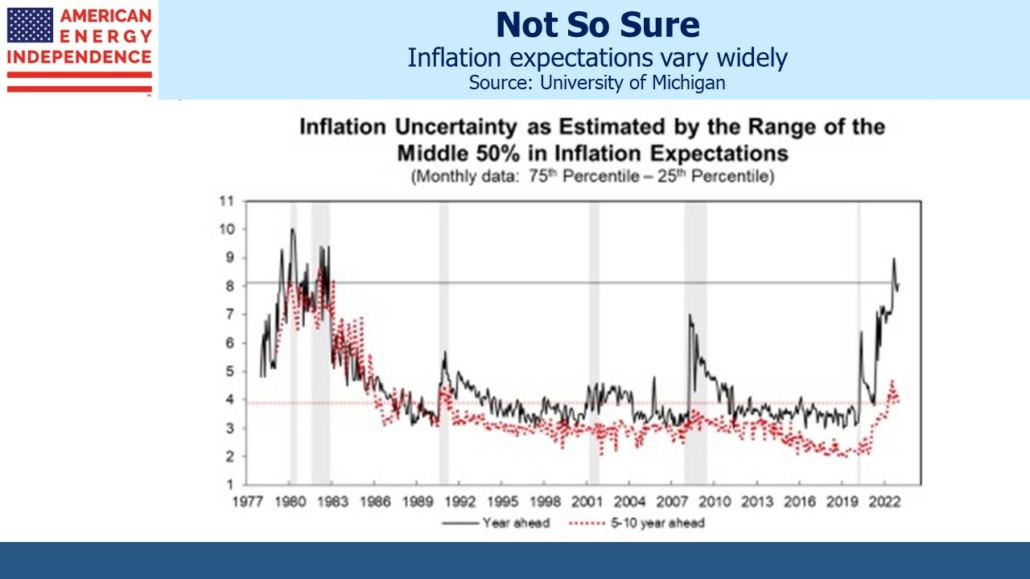

The University of Michigan consumer survey revealed the uncertainty consumers have about the inflation outlook. Although households expect it to return to 2% based upon the average of responses, the range of expectations is the highest it’s been since the 1980s. The difference between the 25th and 75th percentiles for 5-10 year inflation is 4%. Over the next year it’s 8%. There’s not high confidence that it’s returning to 2%.

Benign inflation forecasts, which are similar in the bond market, represent asymmetric risk. Inflation isn’t going to trend below 2%. Retirement planning should be based on 3% and scenarios should be run with higher rates to test how well an investment portfolio will meet one’s spending needs. There are several reasons why conventionally reported inflation figures aren’t a good basis on which to plan growth in living expenses (see Why You Can’t Trust Reported Inflation Numbers). The most obvious is the hedonic quality adjustments that are routinely applied to the CPI to reflect improvements in quality. CPI tries to measure a basket of goods and services of constant utility. Quality improvement at the same price is treated as a price cut.

Hedonic quality adjustments are made to a wide range of products such as clothing, electronic goods and housing. The problem this creates for a consumer is that if a jacket, iPhone or rental property provides better quality at the same price, you don’t have any money left over even though your utility has risen. If you plan on replacing your iPhone regularly in retirement, it’s going to cost you more even though the Bureau of Labor Statistics calculates iPhones are cheaper (because they’re better).

Returning to the ERP – based on the past two decades, the S&P500 is somewhat expensive compared with bonds. Low inflation expectations and optimistic futures create asymmetric upside risk to interest rates, and downside risk to earnings, forecasts for which are trending lower. Both leave stocks vulnerable.

For now, Factset bottom-up earnings for 2023 is for 3% growth over 2022. Flat earnings and ten-year yields back to 4% where they were in November would require a 15% drop in the S&P500 before the ERP was back to its two-decade average. We’re not selling stocks for long-term investors, but the risk asymmetry suggests little need to rush purchases.

—

Originally Posted February 1, 2023 – Confronting Asymmetric Risks

Disclosure: SL Advisors

Please go to following link for important legal disclosures: http://sl-advisors.com/legal-disclosure

SL Advisors is invested in all the components of the American Energy Independence Index via the ETF that seeks to track its performance.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from SL Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or SL Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.