![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-700x394.jpg.webp "[Gamma] Scalping Please")

December is the time of the year to look back and reflect. 2022 has been awful for U.S. bonds and Fixed Income assets generally. When we refer to the fundamental math of bond returns, this would point to 2023 being a better year, without repeating the historical level of losses of 2022.

The fundamentals

To understand the optimism about the asset class, the definition of a bond needs to be reminded: “a bond is a loan an investor makes to a corporation, government, federal agency or other organization in exchange for interest payments over a specified term plus repayment of principal at the bond’s maturity date” (finra.org). The annual interest or coupon is generally paid out semiannually. A bond’s yield is the rate of return the asset generates. A bond’s value is a combination of yield and also price appreciation. There is an inverse relationship between bond value and interest rates: “when interest rates rise, bond prices fall, and vice versa.”

Fundamental bonds returns math

Bonds are generally included in an investors’ portfolios as a source of diversification to help reduce volatility, bring stability and security (bonds are not as risky as equity for example). This has been true these last decades.

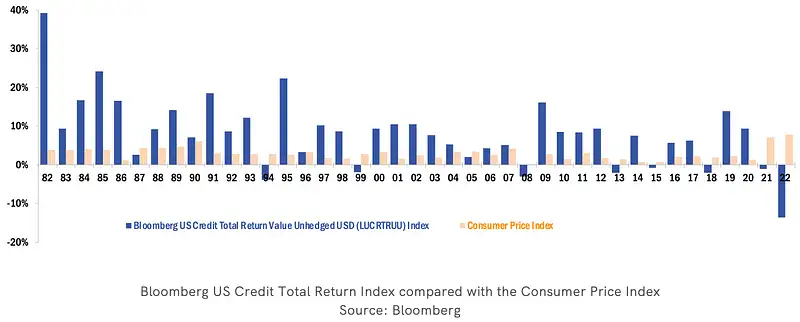

From the above graph, 2022 appears to have been an anomaly. After years of low yields, the rapid monetary policy shift challenged the defensive function of this asset class within a portfolio.

2022 a chaotic year

In March 2022, the Federal Reserve started to significantly raise the Federal fund rates after two years maintaining them near zero per cent. The inflation, announced by the American Central Bank to be transitory, surged during the Summer. The fixed income market saw extensive declines across all segments of this asset class.

In more normal times, the interest income from a bond should have offset declines in its price. In 2022, the unprecedented pace of rate hikes did not allow for this stabilizing effect to take place. After years of low interest rates, the income returns on bonds had become so weak, they were unable to cushion their own price decline.

The situation during the third quarter changed. Having reached high yield returns, these instruments were now providing a greater protection than they had done at the beginning of the year. Furthermore because of the bumpy road in this asset class, many investors had reduced the duration of their portfolios making them less vulnerable to new interest rate increases.

With the bulk of the Federal Reserve’s tightening policy now behind us, only smaller increments of interest rate increases are expected in the coming year. To add to this, economic forecasts are pointing a disinflationary environment which should reduce the need for restrictive monetary policy moving forward. In sum, the outlook for bonds for 2023 looks to be more optimistic.

Seizing the 2023 opportunities

Bond yields are currently the highest levels they have been at in years. The returns are now equivalent or higher than dividend earning stocks. Credit spreads have already widened to price in an expected slowdown in the economy. Fixed income asset class is back to its historical role of bringing in a decent income.

Generally, the economic impact appears six to eighteen months after interest rates have been increased. Some would argue the significant increases of 2022 have already reached very restrictive levels. As such, this should start to filter into slower the economic growth and reduced inflation. This scenario is seen as being the most likely for 2023. This trend should stabilize interest rate levels and may even drive them lower. The part of the interest rate curve most sensitive to this probable outcome would be long-term rates, opening a window for capital gains on longer duration bonds.

Investors are now contemplating adding duration to bond portfolios as an option worth considering. Staying exposed to quality issuers would be preferable if only to avoid the negative outcome of credit defaults linked to weaker credit which would be increasingly probable due to the risk of an upcoming recession.

In 2023, Fixed Income volatility may remain elevated. However, bonds are stepping back into their original role of providing a decent revenue stream as part of a hedge against any economic downturn. Investing in high quality investment grade bonds in 2023 offers the opportunity to take advantage of both worlds, collecting significant income while waiting for potential capital gains from more favorable monetary policy conditions.

—

Originally Posted December 12, 2022 – Back to Basics, Fixed Income Opportunities 2023

ASG Capital is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein.

Disclosure: ASG Capital

ASG Capital is a Registered Investment Advisor. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments or investment strategies. Investment involve risk and unless otherwise stated are not guaranteed. Be sure to first consult with a qualified financial advisor and/or tax professional before implementing any strategy discussed herein.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from ASG Capital and is being posted with its permission. The views expressed in this material are solely those of the author and/or ASG Capital and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.