")

On March 18, the Bank of Japan (BoJ) brought the country out of its eight-year long experiment with negative interest rates by raising borrowing costs for the first time in 17 years. Market reaction was telling. The yen sold off while the Nikkei 225 rallied.

Typically, the reaction to a not-fully-priced rate hike might have been the opposite: the currency strengthens and the equity market sells off. But there is something of a conundrum about negative rates: rather than stimulate growth as envisioned, they instead act as a tax on the banking system. The idea of negative deposit rates is to discourage excess savings and thereby spur spending and investment. Markets, however, seem to think that they have the opposite effect.

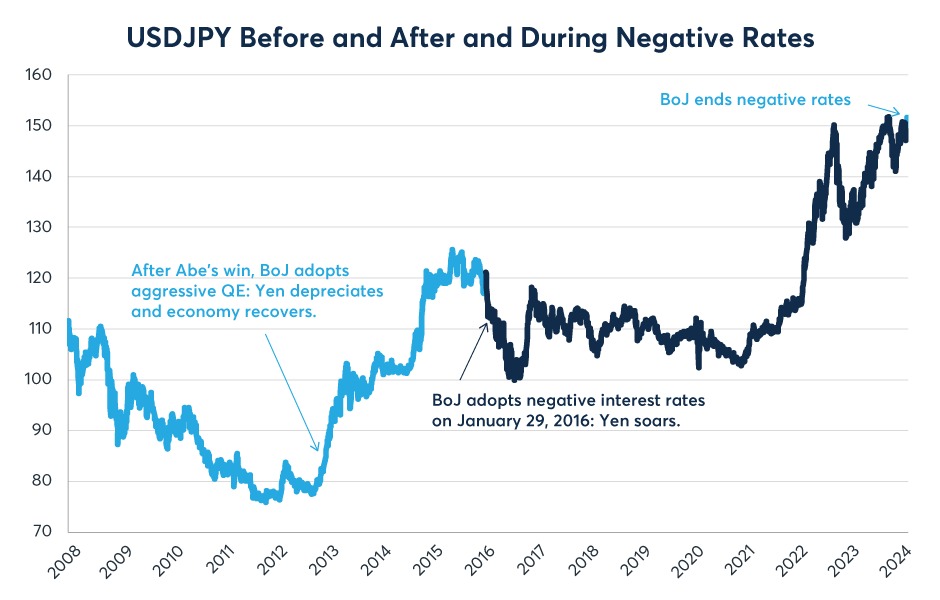

Looking back to January 29, 2016, the day the BoJ first cut rates to below zero, the yen strengthened versus the US dollar (USD). The yen continued to rise for months afterwards, gaining about 10% against USD. By contrast, the yen sank 2% in the week after the BoJ ended negative rates on March 18 (Figure 1).

Figure 1: Negative rates lifted the yen in 2016 while ending them in 2024 sent the currency lower

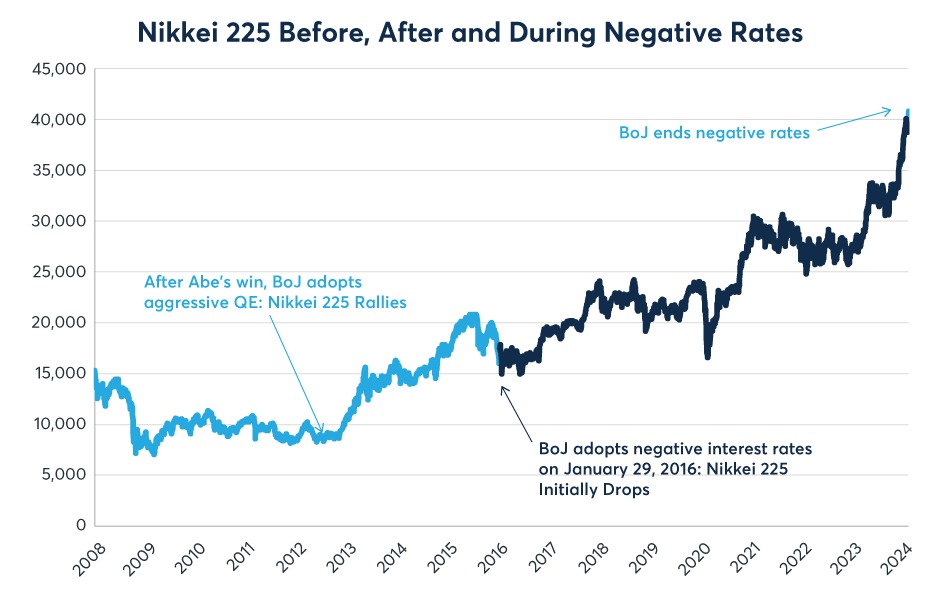

Both times, in 2016 and 2024, the Nikkei 225 had the opposite reaction of the yen. The Nikkei slumped in January and February 2016 when the BoJ initially set rates below zero. By contrast, in March 2024, when the BoJ raised rates, the Nikkei 225 extended its rally (Figure 2).

Figure 2: The Nikkei 225 fell when rates went negative and rallied after rate hike

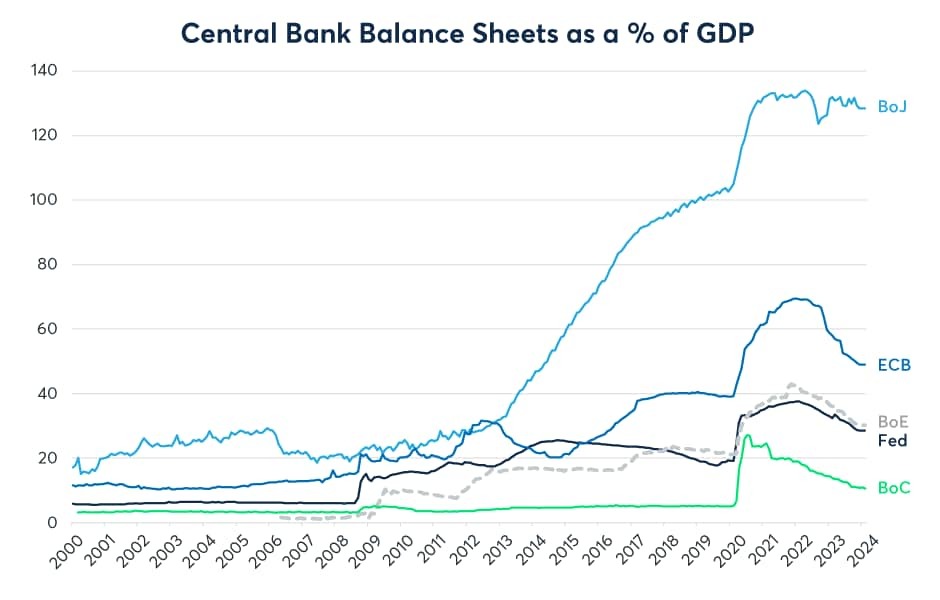

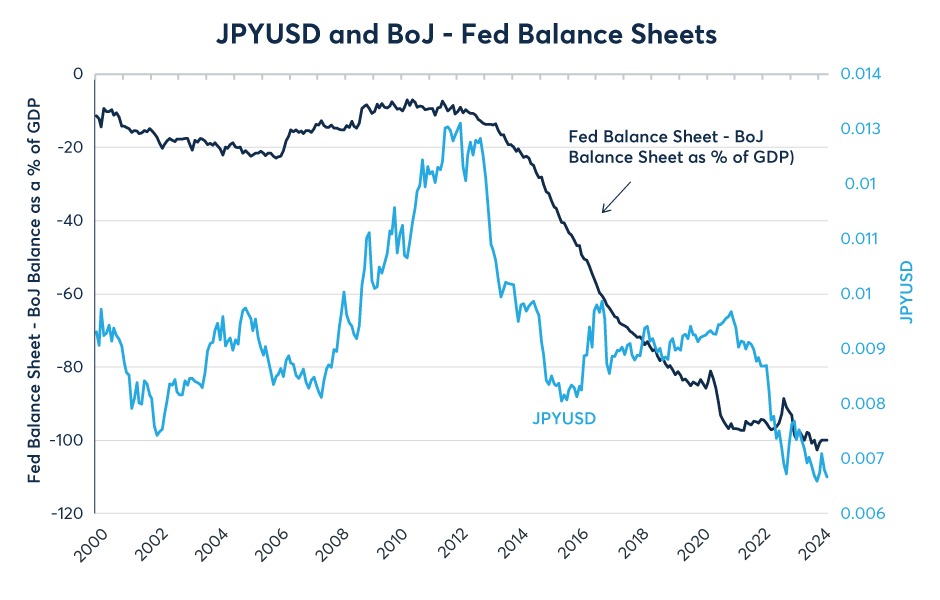

To be fair, the Nikkei didn’t perform badly during the entire period of negative rates. It began a rally in late March 2020 that coincided with the global updraft in asset prices on the heels of massive quantitative easing (QE) by central banks. Notably, BoJ’s QE was much larger relative to GDP and lasted much longer than its peers (Figure 3). The rapid expansion of the BoJ’s balance sheet relative to that of the Fed probably helped to push the yen lower versus USD (Figure 4).

Figure 3: The BoJ’s QE was much bigger than the ECB’s or the Fed’s

Figure 4: The relative expansion of the BoJ’s balance sheet coincided with a weaker yen

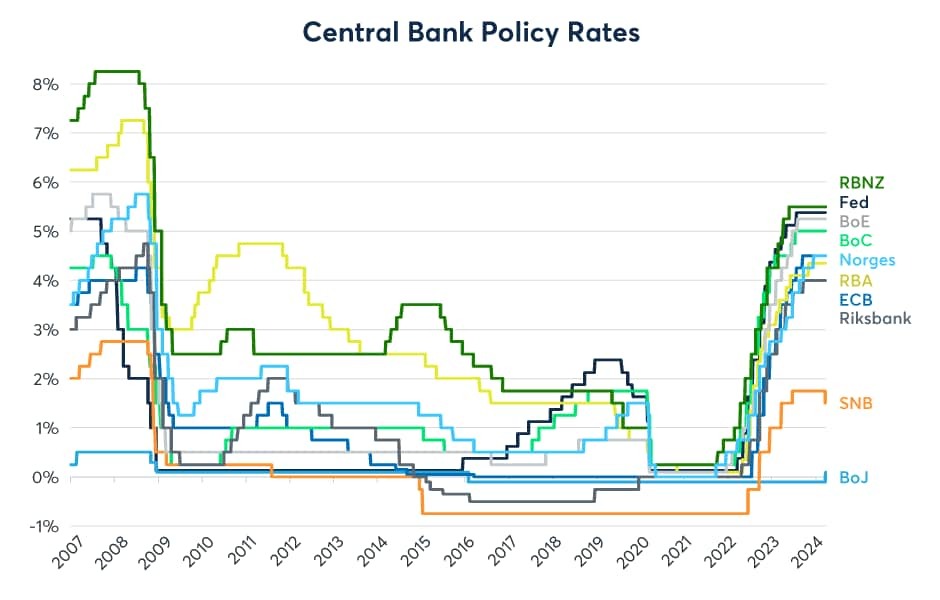

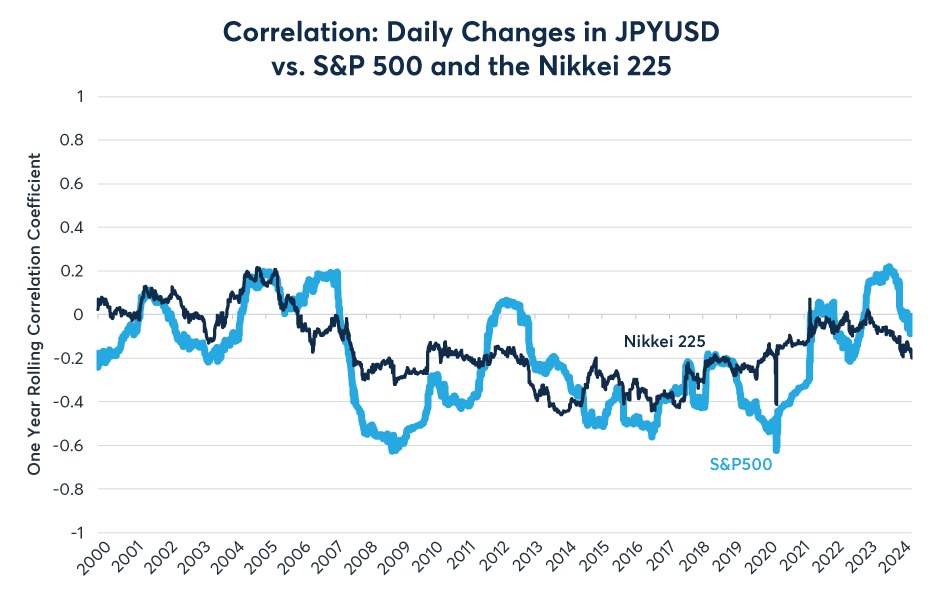

The fact that the BoJ was the last central bank to raise rates (Figure 5) most likely also put downward pressure on the yen, which was probably beneficial to the Nikkei 225. The Nikkei 225 usually had a negative day-to-day corrleation with changes in the value of the yen (Figure 6).

Figure 5: The BoJ is the last central bank to raise rates

Figure 6: The Nikkei 225 usually correlates negatively with JPYUSD

Overall, the BoJ’s first step towards higher rates might have the paradoxical impact of further stimulating economic growth by repealing what amounted to a tax on the banking system. Indeed, even further hikes of up to 0.25% or 0.5% could encourage a more normal functioning of the banking sector. Eventually, higher rates will have the impact of slowing growth as they do elsewhere, but that would likely require rates much higher than the current 0-10 basis-point range. By comparison, rates in the US are ranging from 5.25% to 5.50%.

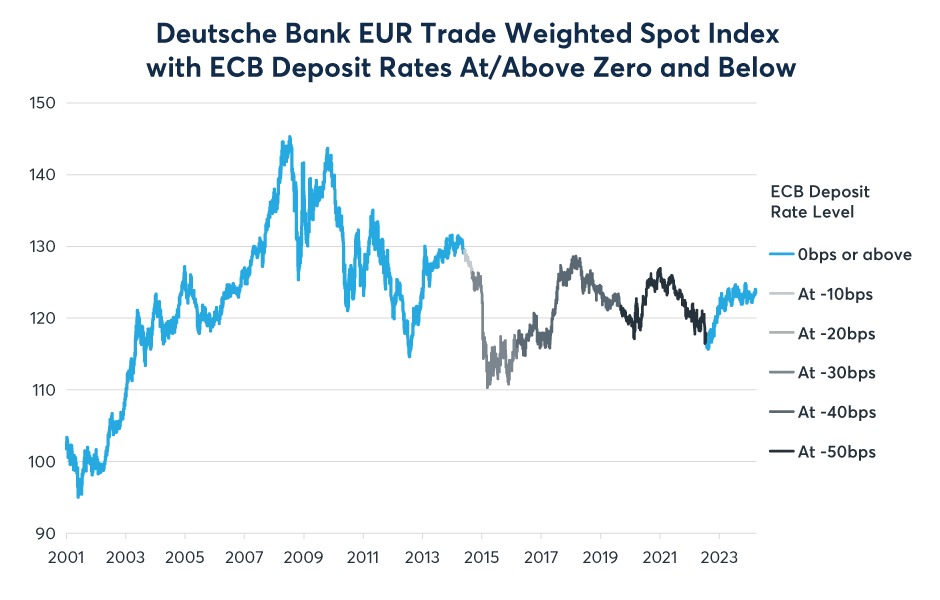

The Eurozone, Sweden and Switzerland also experimented with below-zero deposit rates. Their experiences mirror that of Japan. In the case of the Eurozone, when policy rates were first set to negative, the euro (EUR) fell sharply versus USD, but that was part of a global downdraft of currencies versus USD that coincided with the collapse of oil prices from late 2014-16. In that case, EUR fell alongside the pound, kroner, Australian and Canadian dollars as well as most emerging market currencies. As the European Central Bank (ECB) cut its deposit rate even deeper into negative territory later in the decade, EUR stopped selling off and it actually rebounded versus other currencies (Figure 7).

Figure 7: Negative rates didn’t consistently weaken EUR

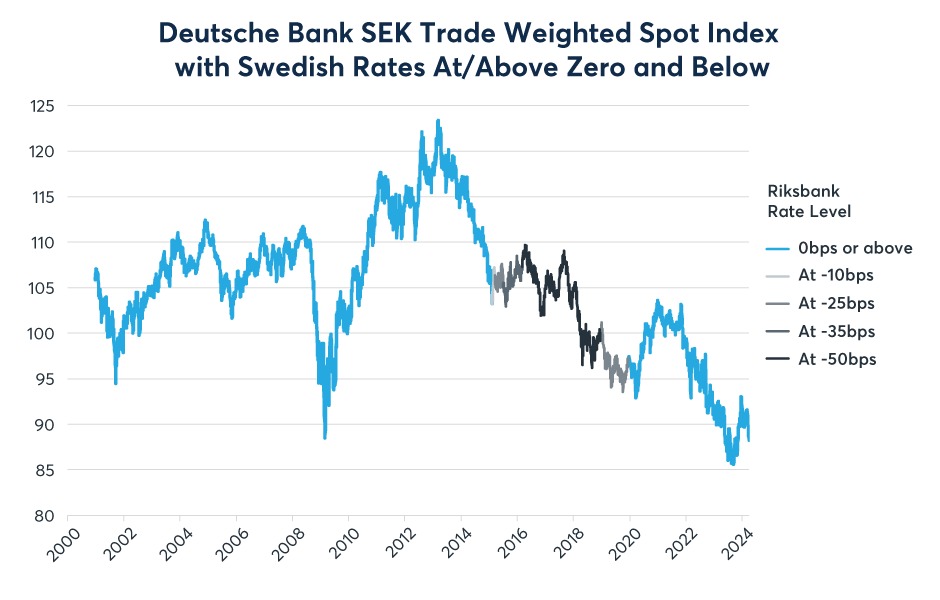

Sweden’s experiment with negative rates seemed to slow the long-term depreciation of the krona (SEK). As Sweden moved from running trade surpluses of close to 12% of GDP to more modest levels closer to 2% of GDP, SEK had been in long-term decline versus most other currencies. What’s curious in Sweden’s case is that the pace of SEK depreciation was faster before and after the negaitve rate period than during it. Also, SEK initially strengthened when negative rates were first implemented and then weakened when the central bank, Riksbank, raised rates back to zero. Both of these moves are in line with the Japanese experience of negative deposit rates (Figure 8).

Figure 8: SEK’s deprecition slowed under the negative rate regime

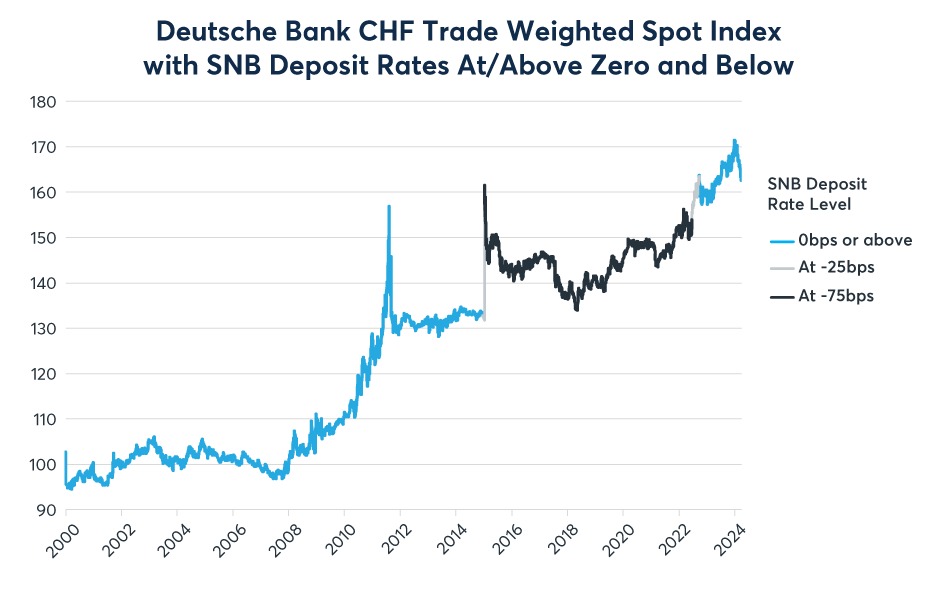

Switzerland provides the most extreme example of negative rates being an unintentional policy tightening. The Swiss franc (CHF) soared when the Swiss National Bank (SNB) first went to negative rates and continued to rise. At the moment the SNB brought rates back to positive levels, CHF sold off and is currently trading near the same level it was at when negative rates ended (Figure 9).

Figure 9: CHF soared when the SNB put rates at negative levels

The experience of negative deposit rates in Europe largely confirm the Japanese experience. Rather than weakening the negative-rate currencies, below zero deposit rates appear to have strengthened them or, in the case of Sweden, perhaps slowed a long-term decline. This suggests that negative rates are seen as restrictive and not expanding money supply growth, and ending them is considered expansionary. Finally, the reaction of the Nikkei 225, a separate asset class, also appears to confirm the reaction of the currency market.

—

Originally Posted April 8, 2024 – Japan Joins the Rate-Hike Club As Rate Cuts Loom

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the author and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Forex

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.