Alphabet’s report of disappointing cloud-computing revenue is causing market sentiment to plunge as investors wait to see if other tech giants have also experienced weakness in their various business areas. At the same time, considerably stronger-than-expected new home sales are pushing bond yields up and increasing worries that higher interest rates will weigh upon tech company valuations.

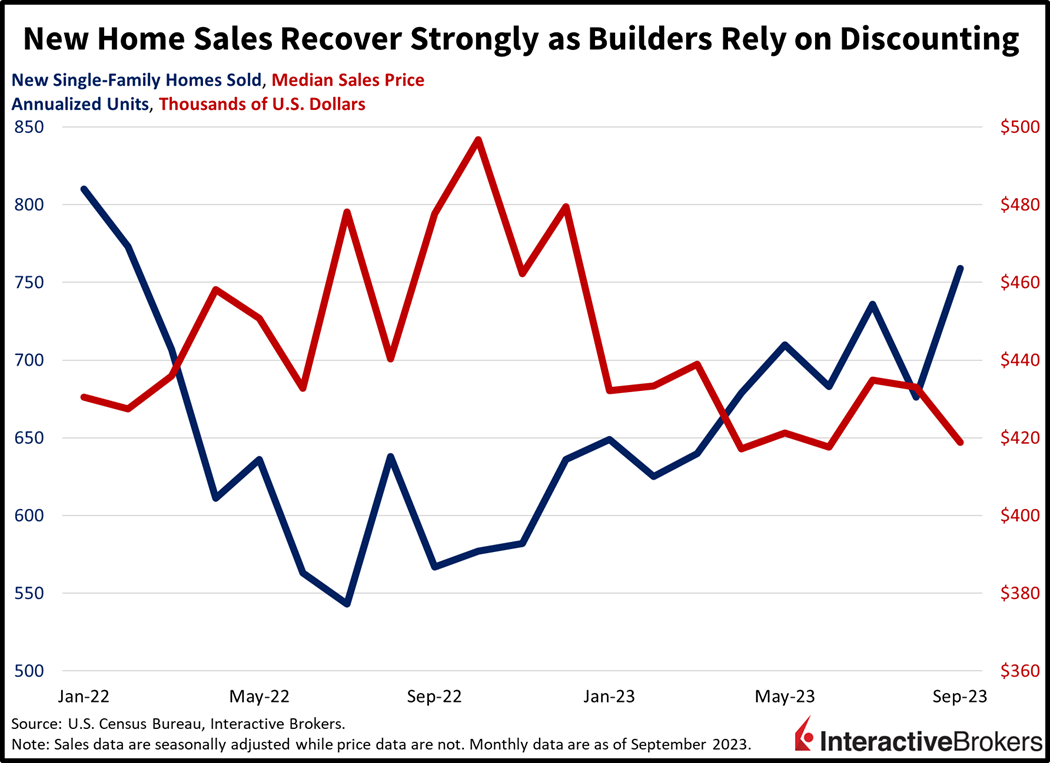

Weak Resale Market Boosts New Home Sales

Depleted existing home inventories led to buyers rushing into the new home market last month, with September New Home Sales coming in hotter-than-expected. The 759,000 seasonally adjusted annualized units outpaced projections of 680,000 and came in better than August’s 676,000. Indeed, new home sales rose at the briskest pace since February 2022. To drive sales, however, builders are offering price concessions, with the median sales price dropping to $418,800 from $433,100 month-over-month (m/m). Furthermore, yesterday evening I was provided with some anecdotal evidence of builders sacrificing margins in an effort to push transactions. While the pace of new home sales rose an impressive 12.3% m/m at the national level, the Northeast and South led with gains of 22.5% and 14.6%. The Western and Midwest regions also contributed to gains at more tempered levels, however, rising 7.5% and 4.7%.

Alphabet’s Pain, Microsoft’s Gain?

Alphabet last night reported generating $8.41 billion in cloud revenue for the most recent quarter, which missed the analyst consensus expectation of $8.64 billion. The revenue miss caused shares of the company to drop approximately 7% in after-hours trading and has sparked a selloff in the tech sector today. The miss occurs as other tech giants such as Amazon.com, which reports earnings tomorrow, are making a big push into off-premises computing. On an encouraging note, Alphabet said a rebound in advertising contributed to overall revenue increasing 17% year over year (y/y). At $76.69 billion, revenue exceeded the consensus estimate of $75.97 billion and contributed to the company’s earnings per share (EPS) reaching $1.55. The EPS exceeded the analyst consensus expectation of $1.45 and climbed from $1.06 y/y.

While the cloud computing results were disappointing, they may not reflect a wider industry trend with Microsoft reporting that its cloud computing and artificial intelligence services generated strong growth in the third quarter. The company’s EPS grew 27% y/y to $2.99 and exceeded the analyst consensus expectation of $2.65. Cost containment measures contributed to profits, but earnings also benefited from the company’s revenue of $56.52 billion growing 13% y/y and exceeding the analyst expectation of $54.50 billion. Revenue for the company’s cloud-computing segment grew 19% and the company’s artificial intelligence customers increased from 11,000 in July to 18,000 as of the end of the quarter. Microsoft Chief Financial Officer Amy Hood said the company anticipates revenue for the current quarter to range from between $60.4 billion and $61.4 billion while the analyst consensus forecasted $60.9 billion in revenue.

While investors appear focused on Alphabet’s cloud-computing results, the growth in advertising earnings could be a positive indicator for Meta, which generates a large portion of its earnings from advertising. Meta is scheduled to release earnings this afternoon.

Pricing Pressures Not Limited to Real Estate

Heineken posted third-quarter results that illustrate the importance of pricing power at a time when increased living expenses, higher financing costs and declining credit availability are squeezing consumer budgets. The company’s beer sales volume dropped 4.2% y/y, in part because it pulled out of the Russian market, but also because consumers pushed back against higher prices. Additionally, for the first nine months of the year, volume fell 5.1%. The company’s results appear to confirm yesterday’s Purchasing Managers’ Index data that showed the U.S. economy is expanding marginally while Europe appears to be in recession. European sales of the company’s beer dropped 8.6% but U.S sales climbed 2.2%. Sales also dropped significantly in Africa, the Middle East & Eastern European regions. Heineken’s higher prices helped offset the impact of declining sales volumes and the company’s revenues climbed 2% to $10.17 billion, but the results narrowly missed the consensus expectation. Other companies are also struggling with passing higher input costs on to customers, with Tesla and many EV manufacturers engaging in a price war while in other industries, Winnebago, Conagra Brands, Darden Restaurants, Shimano and Polaris have all faced sales challenges.

Investors Turn Bearish

Markets are tanking as investors assess the potential impact of earnings, hot economic data and higher interest rates on tech valuations. All major U.S. equity indices are down with technology leading the charge lower. The Nasdaq Composite Index is down 1.4% while the small-cap Russell 2000, S&P 500 and Dow Jones Industrial indices shed 1.3%, 0.8% and 0.1%. Sectoral breadth is poor with a defensive tilt as all sectors are lower minus utilities and consumer staples, which are up 0.4% and 0.2% as market players scoop up equities of companies with stable earnings and dividends. Bond prices are lower across the curve as better-than-expected new home sales boost Fed tightening expectations alongside the inflationary outlook. Yields on the 2- and 10-year Treasury maturities are up 3 and 7 basis points (bps) to 5.1% and 4.91%. The dollar is responding as well, with its index rising 9 bps to 106.33 as the greenback gains relative to the euro, pound sterling, franc, yuan, yen and Aussie and Canadian dollars. Crude oil is down as concerns over a European recession mount while this morning’s data from the U.S. Energy Information Administration pointed to rising U.S. inventories. A softer demand outlook amidst improving supply forecasts are offsetting worries about a wider Middle East conflict potentially disrupting supply conditions. WTI crude is down 0.4% or $0.33 per barrel to $83.30.

Important Days Ahead

Bears seem to be in control lately as they’re pouncing on lackluster earnings and higher yields. Indeed, the 4,200 level appears to be significant for the S&P 500, as I discussed with MarketWatch just last week. A sharp move lower would potentially open the floodgates for the next major level of support which lies at 3,900. For the bulls, however, the upward move in yields may take a break in the beginning of November, as I’m anticipating softer economic data to propel hopes of a lighter Fed. Softer November data alongside a break in yields may lead to a seasonal bull run to end the year around 4,400. A credit event occurring in the interim, however, could lead to the absence of Santa Claus.

Visit Traders’ Academy to Learn More Economic Indicators.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.