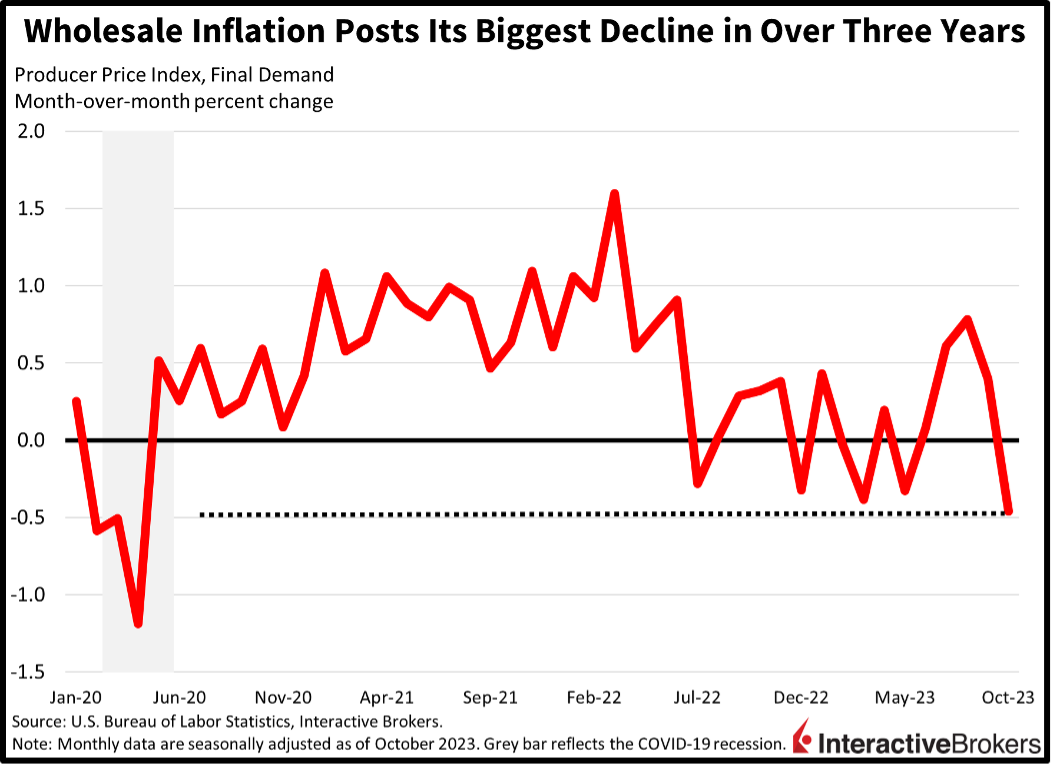

A powerful one-two combination of data pointing to softening inflation is continuing to support investor sentiment and a strong equity rally with Producer Price data this morning showing weaker-than-expected price increases among wholesalers. The data follows yesterday’s release of the Consumer Price Index, which showed no m/m change. Stocks are also gaining additional support from data this morning depicting declining retail sales, which equity players are perceiving as disinflationary rather than contractionary. Markets are bifurcated today, however, with yields and the dollar higher, as bond and currency traders pare back some of yesterday’s bonanza.

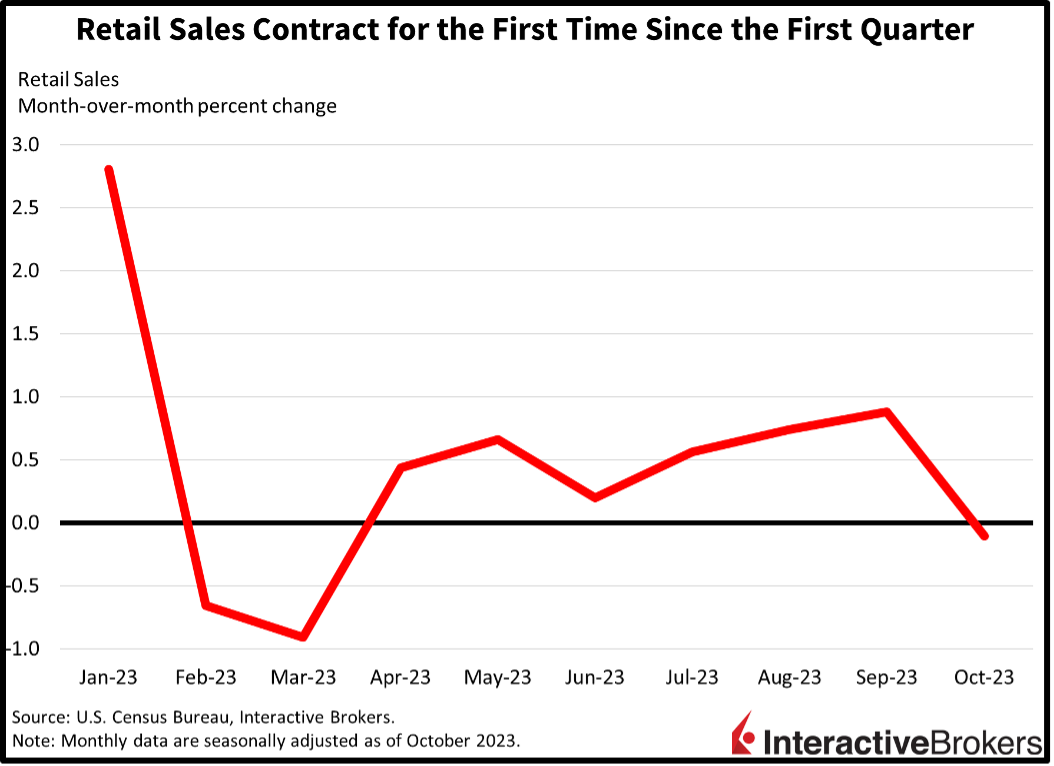

Consumers Rein in Spending

The U.S. Commerce Department reported this morning that retail sales declined sharply in October, as consumer spending slowed from the third quarter’s blistering pace. The resumption of student loan repayments definitely had an adverse impact, as a portion of wages were allocated to debt service rather than consumption. Retail sales declined 0.1% month-over-month (m/m) in October, the first decline since March. October’s figure arrived better than the -0.3% projection, however, while slipping from September’s 0.9% growth rate. Retail sales excluding automobiles and excluding automobiles and gasoline rose 0.1% on both fronts, worse than the 0.8% figures from September.

Sales Contraction is Broad Based

Seven out of thirteen categories contracted during the period, with the following categories experiencing the noted m/m declines:

- Furniture showrooms, 2%

- Miscellaneous stores, 1.7%

- Automobile dealerships, 1%

- Sporting goods retailers, 0.8%

Building materials shops, gasoline stations and general merchandise also had declines but of lesser degrees.

Gains were led by health and personal retailers, with sales increasing 1.1%. Other categories produced the following increases:

- Grocery stores, 0.6%

- Electronics and appliances retailers, 0.6%

- Dining establishments, 0.3%

- Ecommerce, 0.2%

The apparel category was flat.

Wholesalers Hit with Price Declines

Wholesale inflation cratered at its fastest rate since the depths of the pandemic in April 2020. October’s Producer Price Index (PPI) declined 0.5% m/m, less than projections of a 0.1% increase and September’s 0.4% growth rate. Core PPI, which excludes food and energy, was unchanged and weaker than the 0.3% estimated and the previous month’s 0.2%. On a year-over-year (y/y) basis, headline and core producer prices rose 1.3% and 2.4%, compared to the previous period’s 2.2% and 2.7%. Leading the wholesale price decline were a 6.5% drop in energy products, a 0.7% decline in trade services and a 0.2% contraction in food. Transportation and warehousing wholesale prices rose at a sharp 1.5% rate, meanwhile. Services overall came in unchanged m/m while goods excluding food and energy rose 0.1% during the period.

Equities Gain, but Positive Sentiment Eases

Optimism sparked by yesterday’s CPI and this morning’s PPI appears to be easing, with stocks off their highs of the day while yields and the dollar have given back a good chunk of Monday’s gains. Still, all major U.S. equity indices are higher, with the small-cap Russell 2000 leading, having gained 0.8% while the Nasdaq Composite, S&P 500 and Dow Jones Industrial indices are higher by 0.3%, 0.3% and 0.2%. Sectoral breadth remains impressive, with all sectors higher while the defensive health care and utilities sectors are 0.1% and 0.4% lower. Leading the sectors are materials and consumer staples, with each gaining 0.6% as technology looks tired from its recent monster run. Indeed, to secure more gains going forward, the market will need to broaden out and begin to exhibit momentum in cyclical and value stocks. The dollar and yields are higher, with the 2- and 10-year Treasury maturities up 8 and 10 basis points (bps) to 4.92% and 4.55% while the greenback’s index is up 22 bps to 104.30. The dollar is gaining relative to the euro, yen and pound sterling while it loses ground versus the franc, yuan and Aussie and Canadian dollars. Crude oil is down 1.3% or $1.02 to $77.14 per barrel in response to the Energy Information Administration reporting a 17-million-barrel inventory increase in the U.S. over two weeks. Buoyant supply, continued concerns about weakening demand and waning worries over a potential escalation of the Middle East crisis are weighing on the commodity’s price.

Consumers Cut Spending and Seek Bargains

Target’s third-quarter results illustrate how consumers are cutting back on discretionary purchases while results for TJX highlight how consumers are increasingly turning to off-price retailers for low-cost items.

At Target, comparable sales, which is derived from stores operating for 12 months or more and online channels, fell 4.9% during the third quarter. It was the second-consecutive quarter of declining same-store sales. On a y/y basis, the company’s revenues dropped from $26.5 billion to $25.4 billion, a 4.3% contraction. The result, however, exceeded the $24.24 billion anticipated by the analyst consensus. On another positive note, the company’s earnings per share (EPS) of $2.10 exceeded the consensus expectation of $1.48 and increased from $1.54 in the year ago quarter. The quarter was impacted by Target aggressively discounting merchandise as it sought to reduce an inventory glut, a strong trend among retailers. Target also attributed its third-quarter earnings growth to improved sales of “high-frequency items” such as groceries and beauty items, the addition of a new line of trendy kitchenware, and other new items. Target also said it has continued to reduce its inventory which as of the end of the third quarter was down 14% y/y.

TJX, which operates discount retailers T.J. Maxx, HomeGoods and Marshall’s, raised its full-year guidance and said its third-quarter results benefited from capturing market share as its off-price stores attracted cost-conscious consumers. The company expects to generate a full-year EPS of $3.71 to $3.74, up from its earlier guidance of $3.66 to $3.72. TJX expects same store sales to increase 4% to 5%, an increase from its earlier guidance of 3% to 4%. During the third quarter, its sales revenue of $13.27 billion jumped approximately 9% from the $12.17 billion generated by the company in the year-ago period. Analysts expected $13.09 billion. Its overall same-store sales, furthermore, climbed 6%. TJX also posted an EPS of $1.03, which climbed significantly from $0.91 in the year-ago period. The recent quarter EPS exceeded the analyst consensus expectation of $0.99. In addition to benefiting from shoppers seeking bargains, TJX is also benefiting from its suppliers having excess inventory. The company provides discount prices by acquiring surplus items that retailers are removing from their inventories.

Washington Makes Progress of Avoiding Government Shutdown

In Washington, the House of Representatives appears to have avoided a government shutdown by passing a plan that will extend government funding until early next year. The measure is expected to be approved by the Senate and was passed by the lower chamber even though, it delays political battles over spending for border security and the Ukraine-Russia War while failing to make budget cuts in other areas of government spending. The House Freedom Caucus opposed the continuing spending resolution because it doesn’t include budget cuts and address border issues.

The Balancing Act

Today’s weak economic data highlights an important consideration going forward. Is data decelerating slow enough to be supportive of a soft landing, or is activity falling sharply and more consistent with recessionary conditions? The question is of the essence for capital markets as we operate within late-cycle monetary policy tightening, the riskiest juncture. While the former case would be supportive of current earnings estimates, the latter case would certainly point to projections falling from the $240 expected in 2024 for the S&P 500.

Visit Traders’ Academy to Learn More About Retail Sales and Other Economic Indicators.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.

Leave a Reply

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

thanks

Thanks for engaging!