Evaluating the Market Impact of SPX 0DTE Options

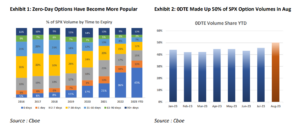

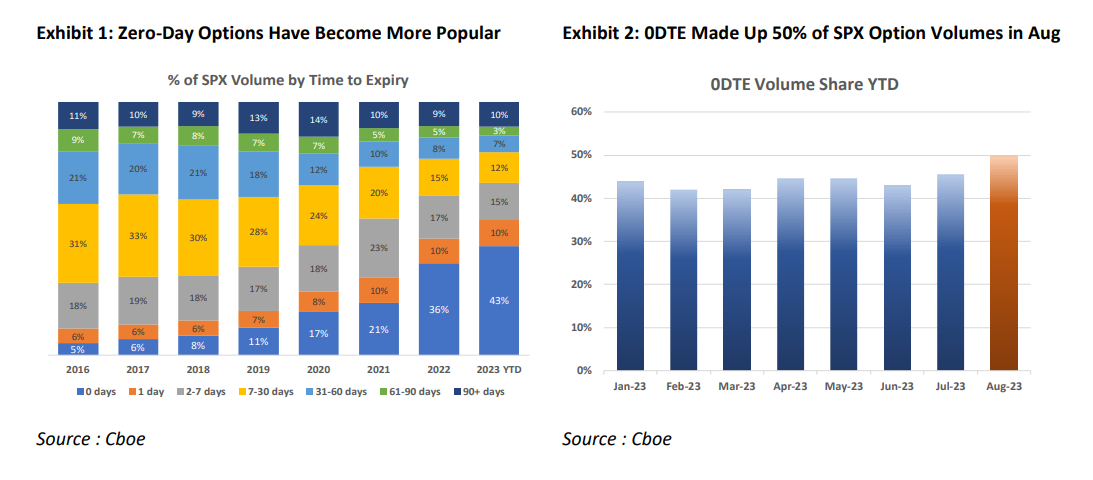

Trading in zero days to expiry options, so called 0DTEs, have exploded in popularity in recent years – rising from 5% of SPX® options volume in 2016 to over 40% since the introduction of Tue/Thu expiries last year (Exhibit 1). In recent weeks, that share has grown even more, averaging 50% in August (Exhibit 2).

As volumes have increased, so have concerns around the market impact of these products. Specifically, the fear is that market makers hedging these options could become outsized relative to the underlying S&P market, and therefore option “gamma hedging” (explained below) may be exerting undue influence on the market. Over the past year, commentators have blamed 0DTEs for everything from exacerbating intraday volatility to suppressing it, with estimates for market maker positioning ranging from “record short” to long $50bn gamma in SPX alone. What’s behind these often contradictory headlines, and crucially, who is right?

What is Gamma Hedging?

To answer that, it’s important to understand what gamma hedging is and why it matters. Gamma refers to the change in the option delta as the underlying asset price changes. In the context of market makers delta-hedging their options positions, gamma is how much they will need to adjust their delta hedge as the underlying moves around. In this case, how much they will have to buy or sell in S&P futures in response to a 1% move in the SPX index.

There are two things to pay attention to when it comes to market maker net gamma positioning. The first is the magnitude – the greater the number, the greater the potential market impact of the option hedging activity. The

second is the sign. Being long gamma means that market makers would be hedging in the opposite direction of the market move – if SPX index rallies, market makers have to sell futures, and if SPX index falls, market makers have to buy – and thus the hedging activity has the potential to dampen market moves. Being short gamma means market makers would be hedging in the same direction of the market move – if SPX index rallies, market makers have to buy more futures, and if it falls, market makers have to sell – and thus have the potential to exacerbate market moves.

High Volume ≠ High Risk

Most of the concern around SPX 0DTE options arise because of their massive volume – averaging over 1.23m contracts ($500bn notional) a day in 2023. While the numbers may sound big, it’s important to emphasize that volume doesn’t equate to risk. High notional doesn’t necessarily mean market makers on the other side of the trade will need to do a lot of hedging. What matters is the balance of the volume between buys vs. sells, not the total size of the volume. To simplify, if 100k contracts trade on a particular strike and 50k was customers buying and the other 50k was customers selling, then despite ~$50bn notional trading on that line, the amount market makers need to buy/sell in S&P futures to hedge is actually…zero. Because the flow is perfectly balanced, market makers are left with net zero gamma risk despite the large volume in the options.

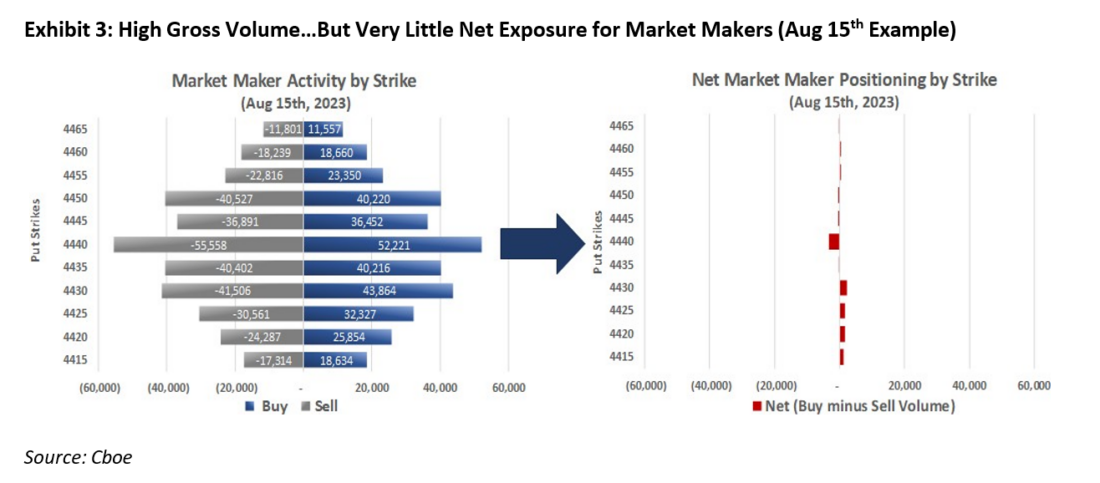

So just how balanced is the customer flow in reality? While many commentators have tried to estimate that (to varying degrees of success), it’s important to point out those are just estimates based on assumptions. Since 98% of the volume in SPX 0DTE options are traded electronically, most outside observers have very little visibility into the exact breakdown of the volume. However, at Cboe®, we do. As the exchange where all SPX options are traded, we can see for every transaction whether it’s customer or market maker, buy or sell, opening or closing. As a result, we are able to get an accurate sense of market maker positioning by tracking their net position (long minus short) at each strike. What we find is that the flow is, in fact, remarkably balanced between buy vs. sell. Take Aug 15th, for example. Much has been written about the 4440-strike put where over 100k contracts traded on that day – yet if you

look at the net positioning, market makers were left short only about 3k contracts (52k buy vs. 55k sell) by the end of the day, or just 3% of the gross volume. See Exhibit 3 above.

Market Maker Gamma Analysis:

Once we have an accurate measure of market maker’s net positioning for each strike, we can calculate an aggregate net gamma number. That number will tell us how much market makers’ delta exposure in 0DTE options will change in response to a 1% move in the SPX index – and as a result, how much potential buying or selling in S&P futures they may need to do in order to stay hedged. The bigger the number, the higher the potential impact.

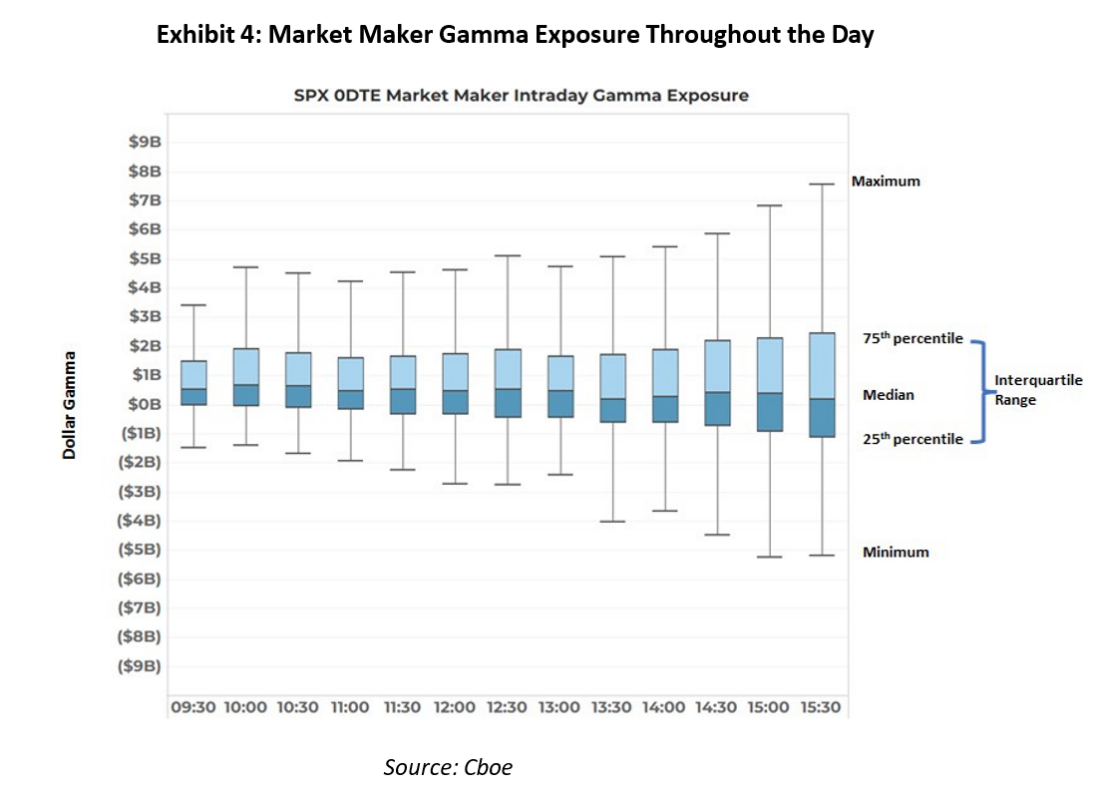

So, just how big do the numbers get? The chart below shows you the range of market maker net gamma positioning throughout the day, taken in 30-min increments over the past year. The boxes tell you the interquartile range from the 25th to 75th percentile of the data (i.e. the middle 50% of the observations over the past year) with the median represented by the horizontal bar in the middle of the box. The “whiskers” extend to the min/max of 1.5x the interquartile range (anything beyond that would be considered outliers).

A few key observations:

- On average, market maker positioning is fairly de minimis, with net gamma exposure ranging from $170mm to

$670mm throughout the day. To put that number in context, S&P futures trade around $400bn a day, so we’re

talking about potential hedging flows that make up between 0.04% to 0.17% of the daily S&P futures liquidity. As we

outlined in our 0DTE white paper, the customer activity in 0DTE options tends to be very balanced because investors use them for a variety of purposes ranging from hedging to yield harvesting, tactical leverage to systematic trading. Unlike the meme stock craze during the pandemic era, we do not see customers trading 0DTE options predominantly for speculative purposes and thus leaving market makers short a lot of gamma. Nor is the product overrun by option sellers as has been suggested. We believe the balanced nature of the flow is a key reason why volumes in 0DTE options have remained robust through different market cycles (SPX index -19% in 2022 vs. +17% this year) as well as different volatility regimes (VIX® index in the 20-30 range last year vs. sub-20 this year).

- While the net gamma range grows wider as the day progresses (which makes sense as gamma increases the closer an option gets to expiry), there is no evidence that market maker positioning grows to be outsized relative to other market participants. The median net gamma at 3:30pm is just +$173mm with the typical range from -$1.1bn to

+$2.4bn (25th to 75th percentile readings). Even if we focus on the “whiskers” on the box plot, the range of -$5bn to

+$7.7bn represents just 1.3% to 1.9% of the S&P futures daily notional volume. Hardly the tail wagging the dog.

It’s worth noting that this analysis is only for market maker positioning in SPX 0DTE options. Market makers may have offsetting positions in other expiries, or other equivalent products (e.g. E-mini or SPY 0DTE options). They may also be hedging their 0DTE positions with other 0DTE options, rather than with linear instruments such as futures.

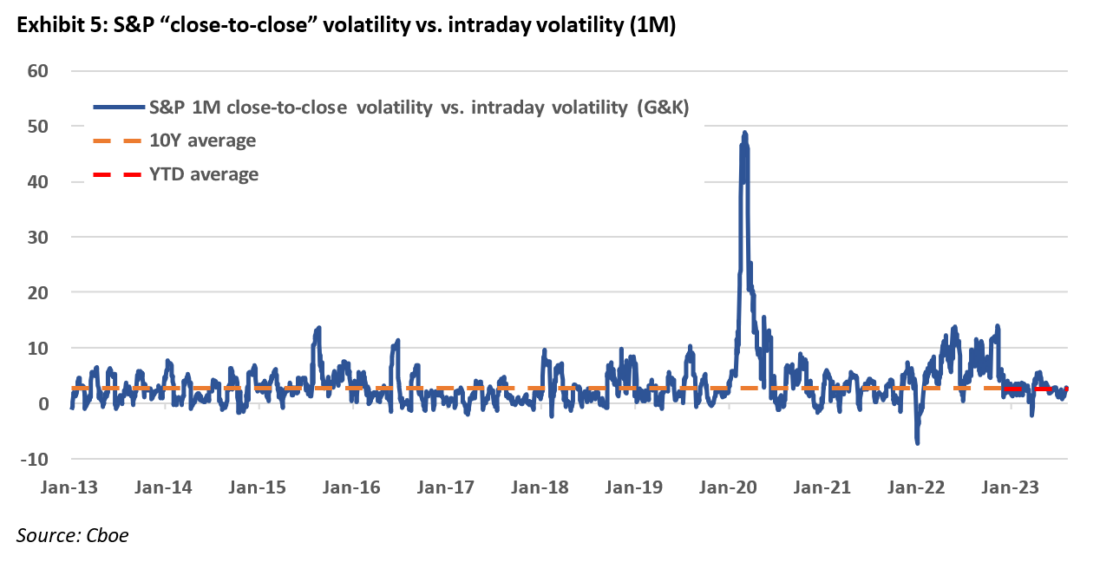

Assessing S&P Intraday Volatility

Last, but not least, another way we can gauge the potential market impact of 0DTE options is to look at the intraday behavior of the SPX index itself, to see if there have been any notable changes in intraday volatility since zero-day options have become more popular.

The conclusion, as you can see in the chart above, is no. The difference between S&P close-to-close realized volatility versus intraday realized volatility is currently right in line with historical averages. The YTD average spread of 2.7 vol pts is exactly the same as the 10-year average (Exhibit 5).

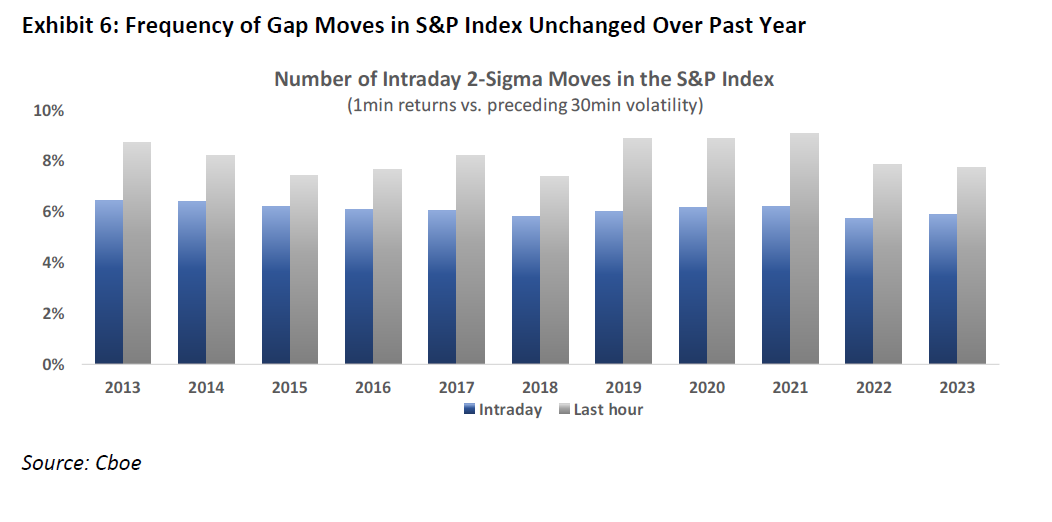

Moreover, if we examine SPX intraday price action for gap moves that could be indicative of large market maker hedging flows, we find no increase in frequency of such gap moves over the past year since the proliferation of 0DTE trading. Specifically, we look at the frequency of 2-sigma moves over a 1min window (i.e. 1min return compared to preceding 30min realized volatility), which will capture sudden jumps in the SPX index. If we’re seeing more “gappy” moves – particularly in the last hour – that could be a sign of option gamma hedging having a disproportionate impact on the market. However, as you can see in the chart below, there has been no uptick in intraday gap moves in the S&P over the past year, either during the trading day or in the last hour going into the close. This is consistent with our market maker positioning analysis above which showed that despite high notional volume in 0DTE options, market maker net exposure is fairly negligible, and hence we’re not seeing any disruptive market impact from the growth in 0DTE trading.

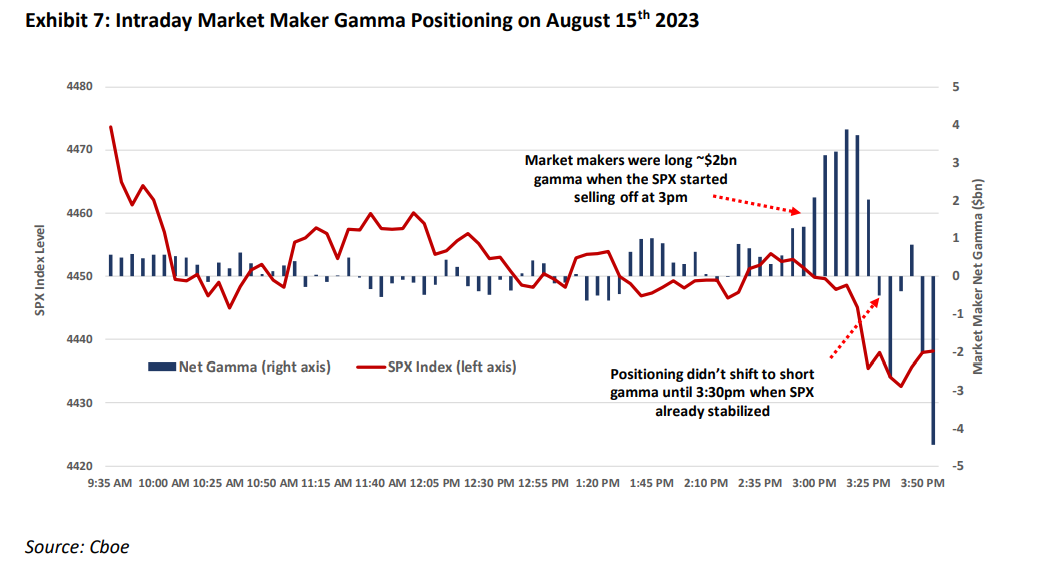

Case Study: August 15th 2023

We conclude by taking a deep dive into one particular trading day that has caught the attention of investors recently: August 15th. Much has been written about the price action on that day, with a focus on the late afternoon sell-off from 3pm to 3:30pm when the SPX index fell 0.4% from 4451 to 4433. Commentators have pointed to the large volume in the 4440-strike put which traded over 100k contracts that day as a potential driver of the sell-off.

However, as we explained above, it’s not the notional volume that matters when it comes to assessing market

impact, rather it’s the balance between buys vs. sells that determines how long or short gamma market makers get. If we look at net gamma exposure across all strikes on Aug. 15, we see that market makers were long about $2bn

gamma at 3pm when the sell-off started – meaning that they would have been hedging in the opposite direction of the market move, potentially dampening rather than exacerbating the sell-off. Market makers didn’t shift to short gamma until 3:30pm when the SPX index had already stabilized and even then it was a very small short exposure of just -$500mm (or 0.13% of S&P futures volume). While the short gamma exposure did increase going into the close, the SPX index actually stabilized during that time, which is the opposite of what you’d expect if 0DTE gamma hedging was a meaningful driver of the index price action.

Conclusion:

In short, it’s clear that despite the huge notional volume that is being traded in SPX 0DTE options on a daily basis, actual net exposure for market makers is fairly minimal, with average net gamma ranging from 0.04% to 0.17% of the daily S&P futures liquidity. There is also no discernible market impact from 0DTE option trading, with SPX index intraday volatility and price patterns in line with historical averages. This is largely due to the balanced nature of 0DTE trading, with both institutional and retail investors finding a diverse range of use cases for the product.

Acknowledgements:

Special thanks to Angie Wang, Jonathan Zaionz, and the Cboe Data and Analytics team for their help in running the analysis behind this report.

—

Originally Published September 7, 2023 – Much Ado About 0DTEs: Separating Fact From Fiction

Disclaimers:

- There are important risks associated with transacting in any of the Cboe Company products or any digital assets discussed here. Before engaging in any transactions in those products or digital assets, it is important for market participants to carefully review the disclosures and disclaimers contained at: https://www.cboe.com/us_disclaimers/

- These products and digital assets are complex and are suitable only for sophisticated market participants.

- These products involve the risk of loss, which can be substantial and, depending on the type of product, can exceed the amount of money deposited in establishing the position.

- Market participants should put at risk only funds that they can afford to lose without affecting their lifestyle.

- © 2023 Cboe Exchange, Inc. All Rights Reserved.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.

Leave a Reply

Disclosure: Cboe Global Markets

Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of Characteristics and Risks of Standardized Options. Copies are available from your broker, or at www.theocc.com. The information in this program is provided solely for general education and information purposes. No statement within the program should be construed as a recommendation to buy or sell a security or to provide investment advice. The opinions expressed in this program are solely the opinions of the participants, and do not necessarily reflect the opinions of Cboe or any of its subsidiaries or affiliates. You agree that under no circumstances will Cboe or its affiliates, or their respective directors, officers, trading permit holders, employees, and agents, be liable for any loss or damage caused by your reliance on information obtained from the program.

Copyright © 2023 Chicago Board Options Exchange, Incorporated. All rights reserved.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Cboe Global Markets and is being posted with its permission. The views expressed in this material are solely those of the author and/or Cboe Global Markets and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. Multiple leg strategies, including spreads, will incur multiple commission charges. For more information read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD) or visit ibkr.com/occ

Great article, very clearly written. Thank you.

It is a highly informative article and a deepening understanding of balancing gamma positionings with timing.

We are happy to hear that you are enjoying our articles!