With yesterday’s flight to safety taking a partial breather – broad equity indices and yesterday’s tech losers opened higher, though regional banks and bond yields continued to decline – it is time to focus once again on impending earnings reports from megacap tech companies. The combination of Apple (AAPL), Amazon (AMZN) and Meta Platforms (META) represents about 12% of the S&P 500 Index (SPX) and 18% of the NASDAQ 100 (NDX). They’re simply too big to ignore.

It appears that yesterday’s reaction to Tuesday’s reports from Microsoft (MSFT) and Alphabet (GOOG, GOOGL) is causing options traders to have a bit more of a healthy respect for risk, at least for one of the names. We noted that skews in near-term options were almost freakishly flattish, so it is encouraging to see that one of the skews for today’s crop of earnings releases are relatively more normal. The other two, not so much…

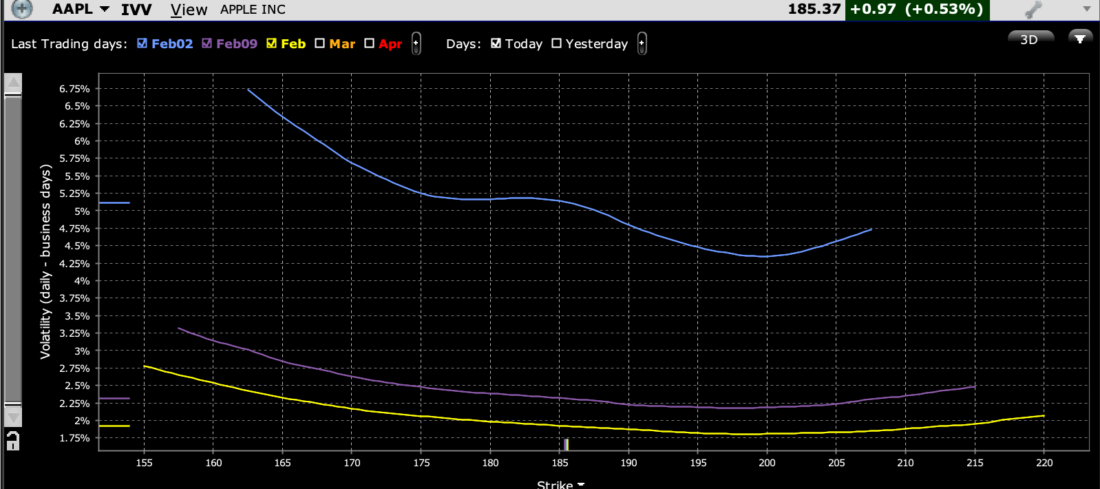

Going in both size and alphabetical order, we see that at-money AAPL options expiring tomorrow are pricing in a daily implied volatility of just over 5%. That is actually a bit above the company’s recent post-earnings history (-0.5%, -4.8%, +4.7%, +2.4%, +7.6%, +3.3%). Consensus estimates are for EPS of $2.11 on revenues of $117.97 billion. That revenue result would be +0.7% higher than it’s year-ago quarter, which would break a streak of four successive quarters of year-over-year revenue declines. EPS would be 12% above last year’s $1.88, so the company is still delivering on the bottom line, if not the top.

While there is a modest implied volatility plateau involving at-money options, we see that there is a pronounced, steep downside skew in the front expiration, and more subtle, but still typically risk-averse skews in the following two weeks:

AAPL Implied Volatilities by Strike for Options Expiring February 2nd (dark blue), February 9th (purple), February 16th (yellow)

Source: Interactive Brokers

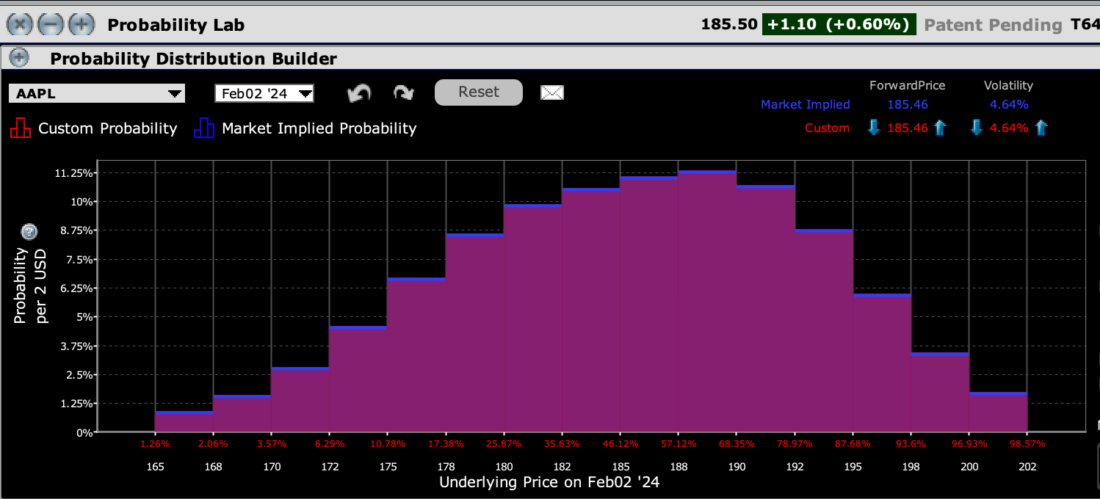

Yet front-week AAPL options display a peak probability for a slight upward move to $187.5-190. The risk aversion only goes so far.

IBKR Probability Lab for AAPL Options Expiring February 2nd

Source: Interactive Brokers

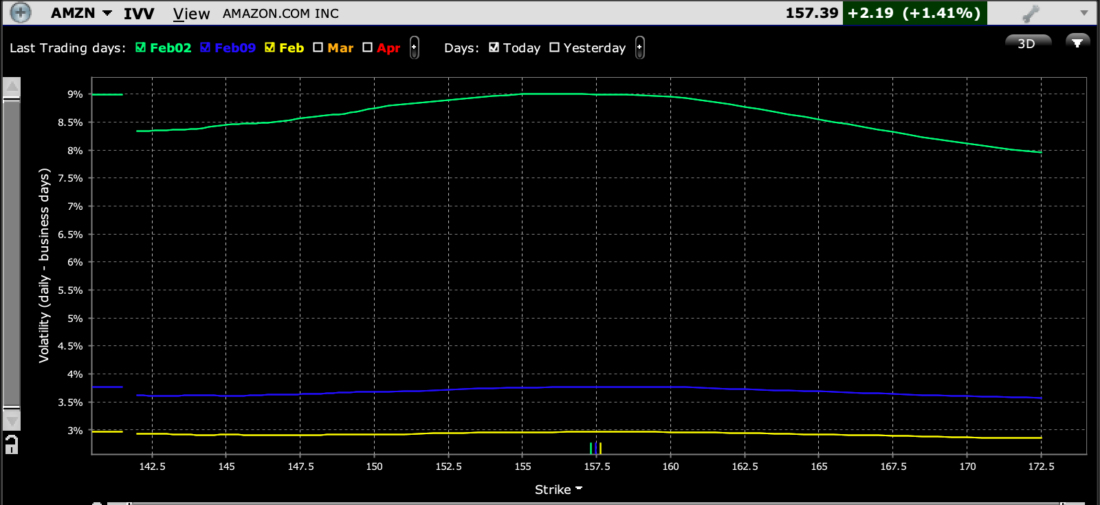

Moving onto AMZN, we see that options are clearly pricing in the likelihood for a significant post-earnings move, but with an inverted skew in near-term options. The 9% implied volatility on at-money options expiring tomorrow reflects AMZN’s history of major moves after reporting results (+6.8%, + 8.3%, -4%, -8.4%, -6.8%, +10.4%), but traders appear to believe that an upside move is as likely as a downward – if not more so. Consensus estimates are indeed optimistic, with expected EPS of $0.80 on revenues of $166.21 billion. Both are well above last year’s $0.03 and $149.2 billion.

AMZN Implied Volatilities by Strike for Options Expiring February 2nd (dark blue), February 9th (purple), February 16th (yellow)

Source: Interactive Brokers

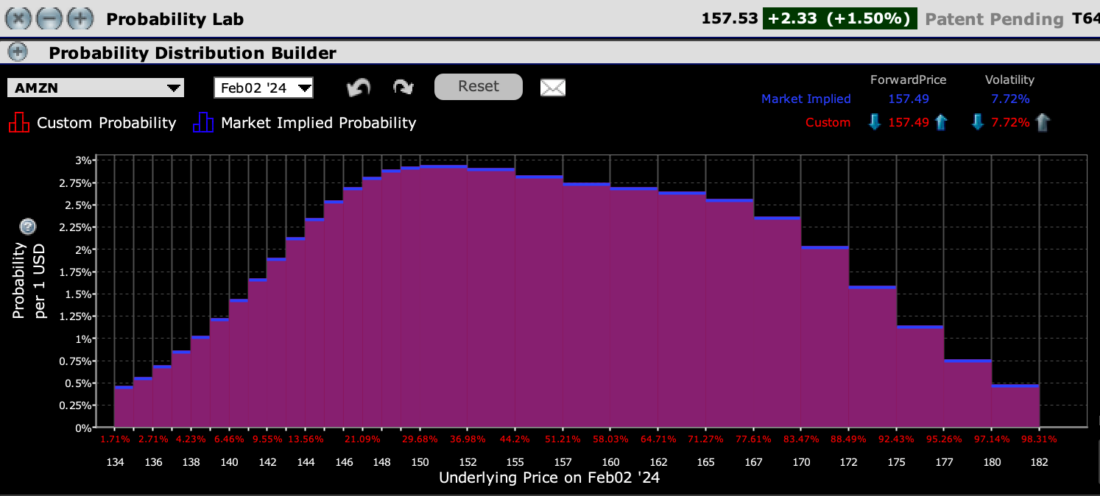

The sanguine mood, if not outright enthusiasm, is reflected in the IBKR Probability Lab for options expiring tomorrow. The peak outcome is indeed in the $150-152 range, below the current $157 level, but cumulative probability (area under the curve) is clearly biased to the upside. It’s as though traders are saying, “it’s going up, we just don’t know how far…”

IBKR Probability Lab for AMZN Options Expiring February 2nd

Source: Interactive Brokers

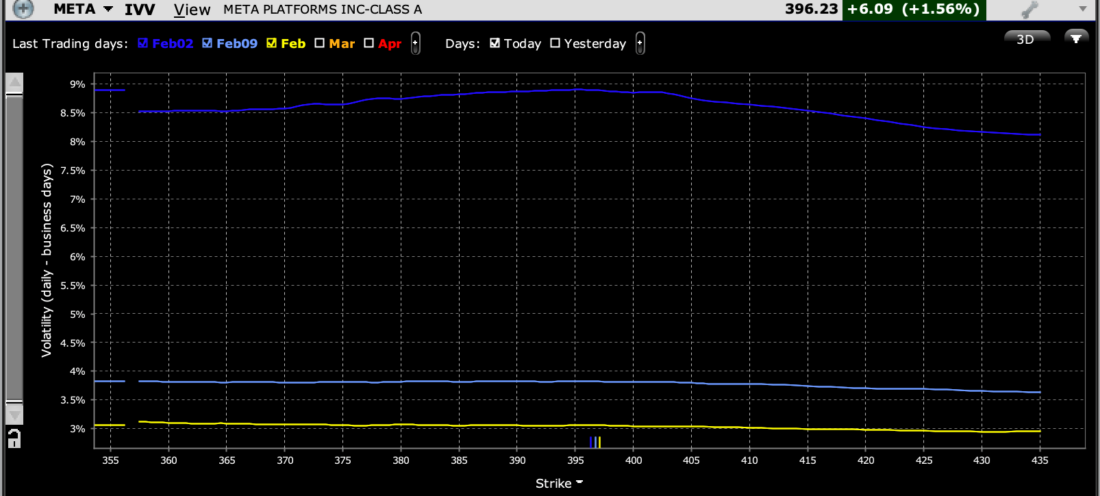

The patterns for META are quite similar to those of AMZN. Frankly, I needed to double check to make sure that I indeed put the correct graphs with the correct company (despite the remarkable similarities of the lines and the Y-axes, the X-axes are indeed quite different) As with AMZN, META’s at-money, front-week options have an implied volatility of about 9%. Considering the last six post-earnings moves were -3.7%, +4.4%, +13.9%, +23.3%, -24.6% and -5.2%, a high level of implied vol seems quite appropriate. Consensus estimates are for EPS of $5.04 on revenues of $39.01, both well above last year’s $4.06 and $32.17 billion. But as with AMZN, the near-term skews are modestly inverted:

META Implied Volatilities by Strike for Options Expiring February 2nd (dark blue), February 9th (purple), February 16th (yellow)

Source: Interactive Brokers

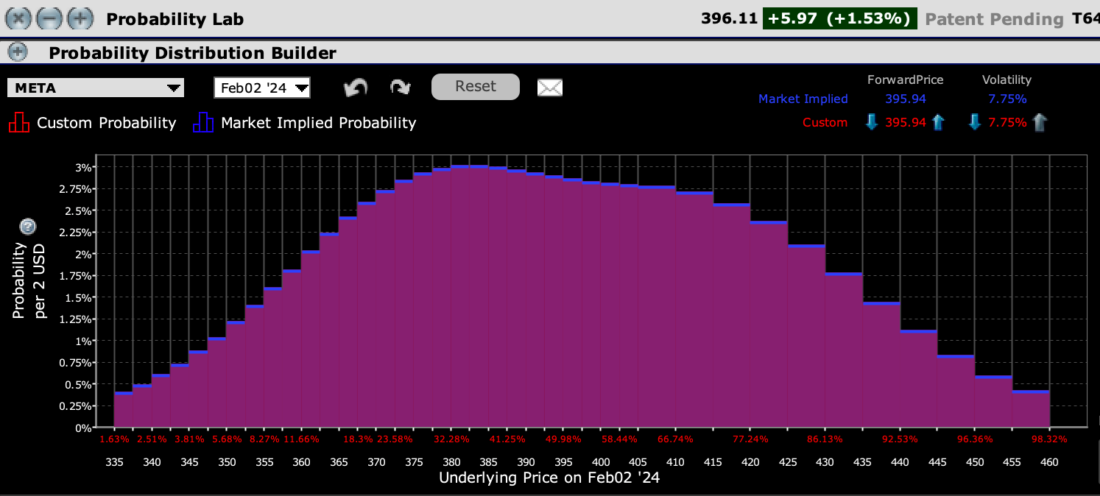

And as with AMZN, the peak probability is for a slight downward move – in this case, to $380-$385 – the cumulative probabilities greatly lean toward upside outcomes:

IBKR Probability Lab for META Options Expiring February 2nd

Source: Interactive Brokers

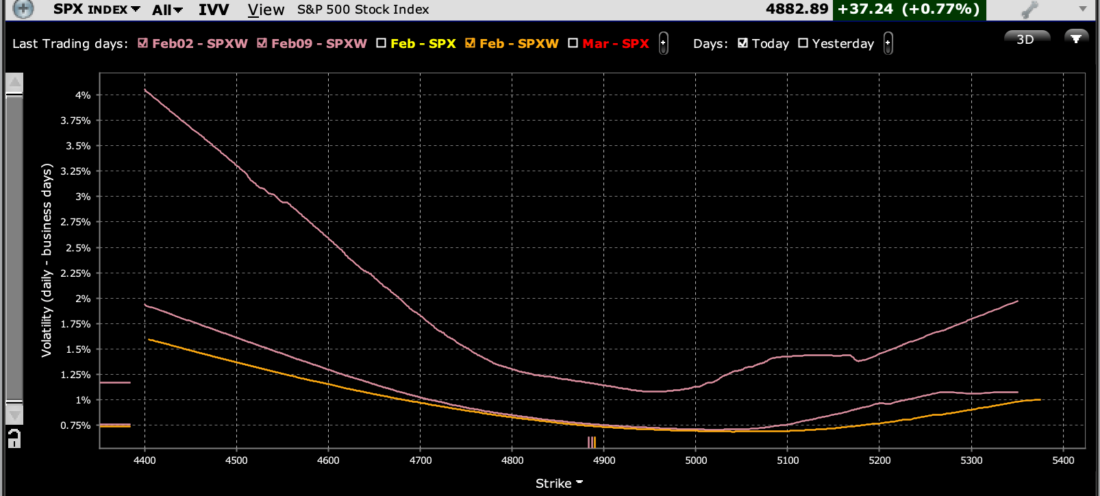

By the way, we would be remiss if we did not take a quick look at SPX. Besides the key earnings results that we just discussed, tomorrow morning brings us the monthly employment data. That’s an awful lot for the market to digest. Nonfarm Payrolls are expected to rise by 185,000 vs. last month’s 216k, the Unemployment Rate is expected to rise by 0.1% to 3.8%, and the monthly growth in Average Hourly Earnings is expected to dip by -0.1 to 0.3%. SPX options expiring tomorrow show a considerable amount of risk aversion, showing at-money implied volatility of about 1.2% and a steep skew:

SPX Implied Volatilities by Strike for Options Expiring February 2nd (lilac, top), February 9th (lilac, middle), February 16th (orange)

Source: Interactive Brokers

Tomorrow has the potential to be a highly consequential day in equity markets. Three of the Magnificent 7 options along with an Employment report can do that. The different factors can of course cancel each other out, but if we see a similar type of sentiment to what we saw yesterday, with good results still not being good enough, then investors have reason to be wary.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Probability Lab

The projections or other information generated by the Probability Lab tool regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. Please note that results may vary with use of the tool over time.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. Multiple leg strategies, including spreads, will incur multiple commission charges. For more information read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD) or visit ibkr.com/occ

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.