The excitement about the promise of artificial intelligence (AI) is shifting to how well the technology will drive increased revenues for tech and the broader economy. To sustain spending on high-end chips, companies must see a payoff.

ChatGPT’s release in November 2022 was a blockbuster, with 100 million users signed up in two months. Even though Meta Platform’s Threads achieved this same milestone in five days, ChatGPT’s achievement is seen as more consequential.1

ChatGPT brought AI and large language models into the mainstream.

While nearly anyone can utilize ChatGPT, the world’s largest tech companies are the ones creating, training and running it. And thus far, a relatively narrow range of stocks is benefiting.

Microsoft, Alphabet and Meta are the companies perceived to be the furthest along in deploying large language models and they have been central to the performance of U.S. equity benchmarks.

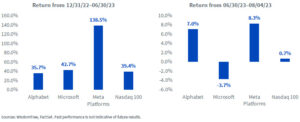

Figure 1: 2023 H1 vs. H2 performance

For definitions of terms in the charts above, please visit the glossary.

The bottom line, as we see it, is that if U.S. equity markets are going to keep trading on AI in the second half of 2023, it will remain largely a game of assessing possibilities and potential, as true transformative adoption is still some time away.

Microsoft—Possibly the Best Story?

CEO Satya Nadella was successful in convincing investors that Microsoft’s Bing search engine, powered by a large language model from Open AI, had a chance to offer Google’s search engine true competition. We see this as a public relations masterstroke, as Google’s 90%-plus market share looks fairly stable.2 However, markets trade not on the reality but on the potential and the story.

In Microsoft’s most recent earnings call, Nadella was at it again, noting3:

…the way I think about it is we still are, whatever, inning two or inning three of even the cloud migration, especially if you view it, right, whether by industry moves to the cloud, segment move to the cloud as well as country adoption of the cloud. There’s still early innings of the cloud migration itself. There’s a lot there still. And then on top of that, there is this completely new world of AI driving a set of new workloads.

Microsoft’s Azure cloud platform has emerged as a major growth engine for the company, currently achieving something roughly equal to a $60 billion per year revenue run rate. There are few lines of business that can continue to grow in a range of 20%–30% per year once hitting those levels, but this is what’s needed to support Microsoft’s roughly $2 trillion market capitalization. Generative AI is clearly viewed as further fuel—so much so that it’s possible that Microsoft will spend $50 billion on capital investment during the current fiscal year.4

One of the most interesting announcements Microsoft made was not during the earnings call but the week prior, when it announced Co-Pilot would be accessible across Microsoft Office 365 for $30 per month per user. Few software packages have the reach of Office 365, and once this is available it will give investors a very direct, clear view of true AI adoption, as well as how quickly it is occurring.5

Alphabet—Possibly the Best Potential?

Throughout all of the hype, we have never forgotten that the generative pre-trained transformer was initially referenced in a paper by researchers at Alphabet.6 Alphabet has enormous research capabilities, but its Google search engine is so dominant that the company is often faced with a version of the so-called “Innovator’s Dilemma.” While Microsoft can take risks and deploy new versions of its Bing search engine, Google must be far more pragmatic.

Alphabet commented that 70% of generative AI unicorns are using Google Cloud.7 Models trained on massive datasets are usually most efficiently stored in the cloud, where computational workloads can be dialed up or dialed down when needed. If the generative AI reality is driven by the large public cloud providers, perhaps this will be a catalyst for Google Cloud to gain market share against Microsoft and Amazon.com.

So far, there is nothing quite as concrete as Microsoft’s pricing of Co-Pilot within Office 365, but it is widely expected that Google will feature new applications of its Gemini model in the second half of 2023. Google has its own enormous base of users in its Android smartphone ecosystem, as well as among users of Gmail. We’ll have to see if there are any direct monetization stories that emerge, as opposed to AI simply helping the company’s existing business lines perform more strongly.

Meta Platforms—An Open Source Model but a Stronger Core Business

Microsoft’s approach is useful for analysis, in that it creates decisions that customers can make—things they can opt to pay for—and then we can all measure this across time. However, it’s not the only way.

Meta has garnered a lot of attention for releasing its LLAMA model as open source, allowing developers to work with it more directly. Of course, “open source” means that Meta is not directly monetizing this access.

The biggest use so far of AI computing power has been various forms of content recommendation. Meta has an ideal business for this, and the most recent quarter’s results had the impact of AI sprinkled throughout. One that caught our attention was that Reels has reached over 200 billion views per day, and its monetization is now at a roughly $10 billion annual run rate.8 Few platforms have the scale that we see with Meta, which includes Facebook, Instagram and WhatsApp.

Enough of an Engine for Growth Leadership to Continue?

At WisdomTree, a primary question we continue to monitor regards value or growth as the investment style set to drive equities forward. From the global financial crisis of 2008/09 until 2022, it was largely all about growth. Last year was the year of value. The first half of 2023 saw the pendulum swing back to growth.

And here we sit, roughly one and half months into the second half of 2023.

If growth continues to lead, it is likely big tech will be central and that AI in some form will continue to be the catalyst. One thing in particular we are looking forward to is the details Nvidia brings forth in its next earnings report and whether it is enough to surprise markets higher again, like it did in May 2023. We also continue to expect further announcements from the largest companies regarding their AI efforts.

1 Source: Hasan Chowdhury, “Threads Beat ChatGPT to 100 Million Users but the AI App Is Way More Consequential,” Business Insider, 7/10/23.

2 Source: “Is Google’s 20-Year Dominance of Search in Peril?” Economist, 2/8/23.

3 Source: https://view.officeapps.live.com/op/view.aspx?src=https://c.s-microsoft.com/en-us/CMSFiles/TranscriptFY23Q4.docx?version=f64b33fa-1c41-799b-70cf-cc2cd098555b

4 Source: Weiss et al., “4Q23 Results—Good Things Come to Those Who Wait,” Morgan Stanley Research, 7/26/23.

5 Source: Weiss et al., “Inspire-d By an Even Larger Microsoft 365 Copilot Opportunity,” Morgan Stanley Research, 7/19/23.

6 Source: Vaswani et al., “Attention Is All You Need,” ARXIV, 6/12/17.

7 Source: Nowak et al., “Across-the-Board Beat, AI Leadership and Opex Discipline Still at 17x ’24 EPS; Remain OW,” Morgan Stanley Research, 7/26/23.

8 Source: Nowak et al, “AI Glory Days; Raise PT to $375,” Morgan Stanley Research, 7/27/23.

—

Originally Posted August 16, 2023 – Will Big Tech Have Fuel for an H2 2023 Rally?

Important Risks Related to this Article:

For current Fund holdings, please click on the respective tickers: QGRW, WTAI . Holdings are subject to risk and change.

QGRW: There are risks associated with investing, including the possible loss of principal. Growth stocks, as a group, may be out of favor with the market and underperform value stocks or the overall equity market. Growth stocks are generally more sensitive to market movements than other types of stocks. The Fund is non-diversified and, as a result, changes in the market value of a single security could cause greater fluctuations in the value of Fund shares than would occur in a diversified fund. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index or take defensive positions in declining markets and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

WTAI: There are risks associated with investing, including the possible loss of principal. The Fund invests in companies primarily involved in the investment theme of artificial intelligence (AI) and innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Disclosure: WisdomTree U.S.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Funds before investing. U.S. investors only: To obtain a prospectus containing this and other important information, please call 866.909.WISE (9473) or click here to view or download a prospectus online. Read the prospectus carefully before you invest. There are risks involved with investing, including the possible loss of principal. Past performance does not guarantee future results.

You cannot invest directly in an index.

Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, real estate, currency, fixed income and alternative investments include additional risks. Due to the investment strategy of certain Funds, they may make higher capital gain distributions than other ETFs. Please see prospectus for discussion of risks.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

Interactive Advisors offers two portfolios powered by WisdomTree: the WisdomTree Aggressive and WisdomTree Moderately Aggressive with Alts portfolios.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree U.S. and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree U.S. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

")

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.