This post shows how to apply the Particle Swarm Optimization (PSO) to estimate the Nelson-Siegel parameters using pso R package.

Particle Swarm Optimization (PSO)

PSO is a population-based optimization algorithm that mimics the collective behavior of birds or fish. It operates with a group of particles, each representing a possible solution to an optimization problem. These particles move through a solution space, continuously adjusting their positions and velocities. Each particle keeps track of its personal best solution and learns from the global best solution found by any particle in the population.

By balancing personal experience and global knowledge, PSO efficiently explores the solution space, gradually converging towards an optimal solution. The algorithm’s performance relies on relevant parameters like the number of particles, maximum velocity, and learning factors.

As with most topics, there is a wealth of extensive and valuable information about PSO available on Google, and this post does not duplicate it. Instead, I focus on applying the psoptim() function from the R package pso to solve practical problems.

R code

The following R code estimates the Nelson-Siegel parameters by using the PSO.

#========================================================#

# Quantitative Financial Econometrics & Derivatives

# ML/DL using R, Python, Tensorflow by Sang-Heon Lee

#

# https://shleeai.blogspot.com

#--------------------------------------------------------#

# Estimating the Nelson-Siegel model

# using Particle Swarm Optimizer (PSO)

#========================================================#

graphics.off(); rm(list = ls())

library(pso) # psoptim

#-----------------------------------------------

# Objective function

#-----------------------------------------------

objfunc <- function(para, y, m) {

beta <- para[1:3]; la <- para[4]

C <- cbind(rep(1,length(m)),

(1-exp(-la*m))/(la*m),

(1-exp(-la*m))/(la*m)-exp(-la*m))

return(sum((y - C%*%beta)^2))

}

#=======================================================

# 1. Read data

#=======================================================

# b1, b2, b3, lambda for comparisons

ns_reg_para_rmse1 <- c(

4.26219396, -4.08609206, -4.90893865,

0.02722607, 0.04883786)

ns_reg_para_rmse2 <- c(

4.97628654, -4.75365297, -6.40263059,

0.05046789, 0.04157326)

str.zero <- "

mat rate1 rate2

3 0.0781 0.0591

6 0.1192 0.0931

9 0.1579 0.1270

12 0.1893 0.1654

24 0.2669 0.3919

36 0.3831 0.8192

48 0.5489 1.3242

60 0.7371 1.7623

72 0.9523 2.1495

84 1.1936 2.4994

96 1.4275 2.7740

108 1.6424 2.9798

120 1.8326 3.1662

144 2.1715 3.4829

180 2.5489 3.7827

240 2.8093 3.9696"

df <- read.table(text = str.zero, header=TRUE)

m <- df$mat

y1 <- df$rate1; y2 <- df$rate2

#==============================================================

# 2. Particle Swarm Optimizer

# : PSO Optimization with constraints

#==============================================================

# NS estimation with 1st data

y <- y1

x_init <- c(y[16], y[1]-y[16],

2*y[6]-y[1]-y[16], 0.0609)

set.seed(90)

psopt<-psoptim(x_init, fn = objfunc,

lower = c(0, -20, -20, 0.015),

upper = c(20, 20, 20, 0.075),

y = y, m = m)

nsptim_out1 <- c(psopt$par, sqrt(psopt$value/length(m)))

# NS estimation with 2nd data

y <- y2

x_init <- c(y[16], y[1]-y[16],

2*y[6]-y[1]-y[16], 0.0609)

set.seed(90)

psopt <- psoptim(x_init, fn = objfunc, y = y, m = m,

lower = c(0, -20, -20, 0.015),

upper = c(20, 20, 20, 0.075),

control = list(trace=1, REPORT=50,

reltol=1e-4, abstol=1e-8,

hybrid=TRUE, hybrid.control=list(maxit=10)))

nsptim_out2 <- c(psopt$par, sqrt(psopt$value/length(m)))

#=======================================================

# 3. Results and Comparisons

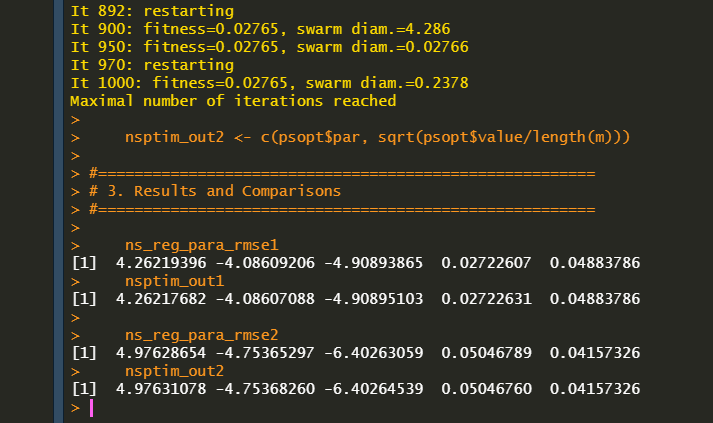

#=======================================================

ns_reg_para_rmse1

nsptim_out1

ns_reg_para_rmse2

nsptim_out2

As can be seen in the following results, these simple examples yield the same outcomes with the given estimates.

Some research has applied hybrid particle swarm optimization and achieved promising results in financial applications such as asset allocation and yield curve fitting, among others, indicating the need for further exploration and investigation. Therefore, this post serves as a small step and starting point for guiding its usage.

Originally posted on SHLee AI Financial Model blog.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from SHLee AI Financial Model and is being posted with its permission. The views expressed in this material are solely those of the author and/or SHLee AI Financial Model and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.