Key News

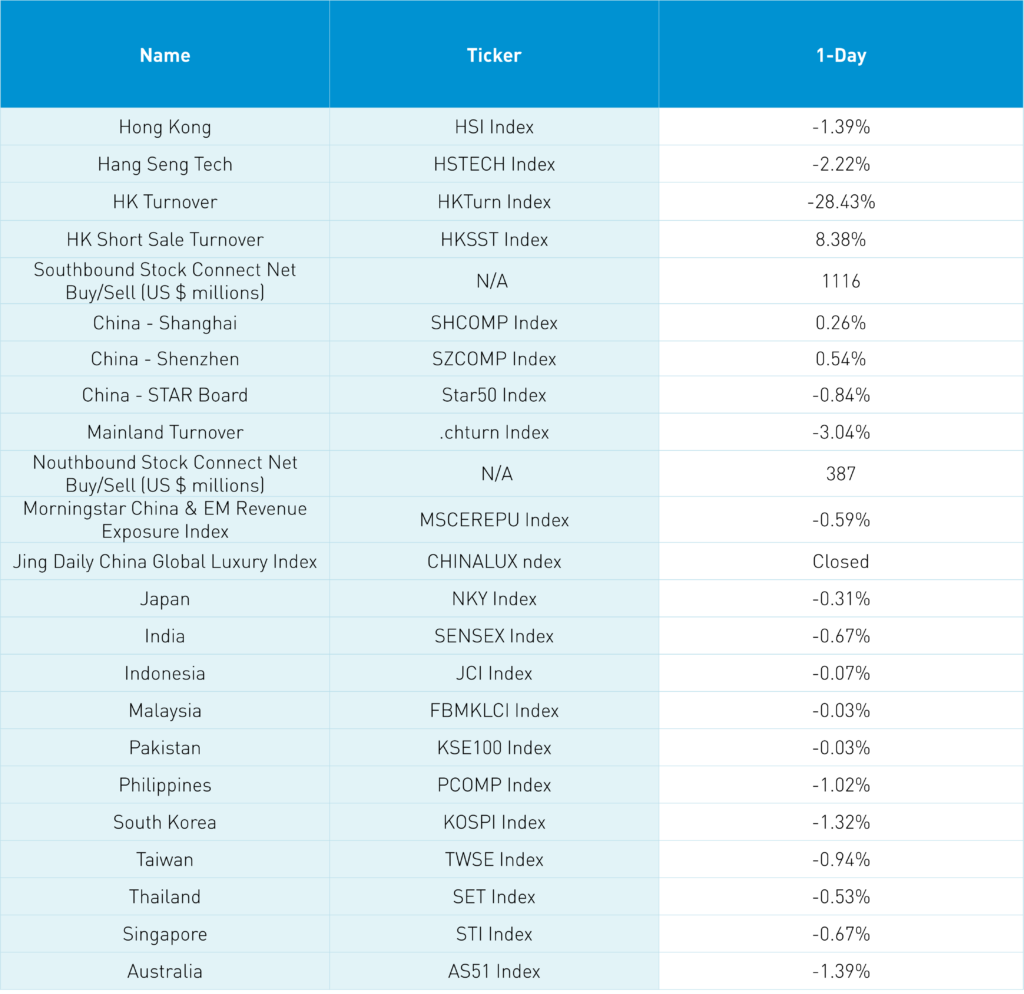

Asian equities had a rough start to the week except for Mainland China, which outperformed the region while Japan was closed for the “Respect for the Aged Day” holiday.

Multiple central banks will meet this week as investors look for interest rate hike guidance. US and China diplomatic relations continued to stabilize as National Security Advisor Jake Sullivan and Foreign Minister Wang met in Malta as steps are taken to arrange for a Biden-Xi meeting at the APEC conference in San Francisco in November.

Today is a good example of our onshore China (predominantly owned by investors in China) versus offshore China (predominantly owned by foreign investors) thesis as both markets traded in opposite directions overnight. Today’s market action in Hong Kong is somewhat surprising as early figures on domestic travel before China’s weeklong holiday appear strong. Meanwhile, there are signs that the economy has stabilized, if not bottomed out, as policy reforms start to take effect.

Western media headlines point to poor real estate news as Evergrande’s wealth unit employees were apparently arrested, a story that came out overnight alongside multiple front page headline on China’s distressed real estate developers. I am still looking for more details on the circumstances surrounding this action.

Western media is rooting for a real estate collapse, though, remarkably, China has not had a recession in decades. So, why did Mainland real estate fall -0.68% while Hong Kong real estate fell -2.40%? Simply put, foreign investors “freaked out” while Mainland investors shrugged their shoulders. The issue for Hong Kong is simply a lack of buyers, which allows short sellers to press their bets with 23% of Main Board turnover being short turnover. Mainland regulators have limited supply (IPOs and insider sales) while trying to increase demand (encourage dividends and buybacks). Hong Kong should do the same, though I would recommend they look at short selling volumes, which are abnormally high.

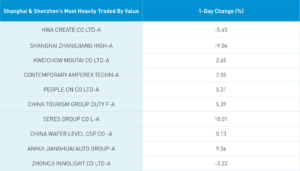

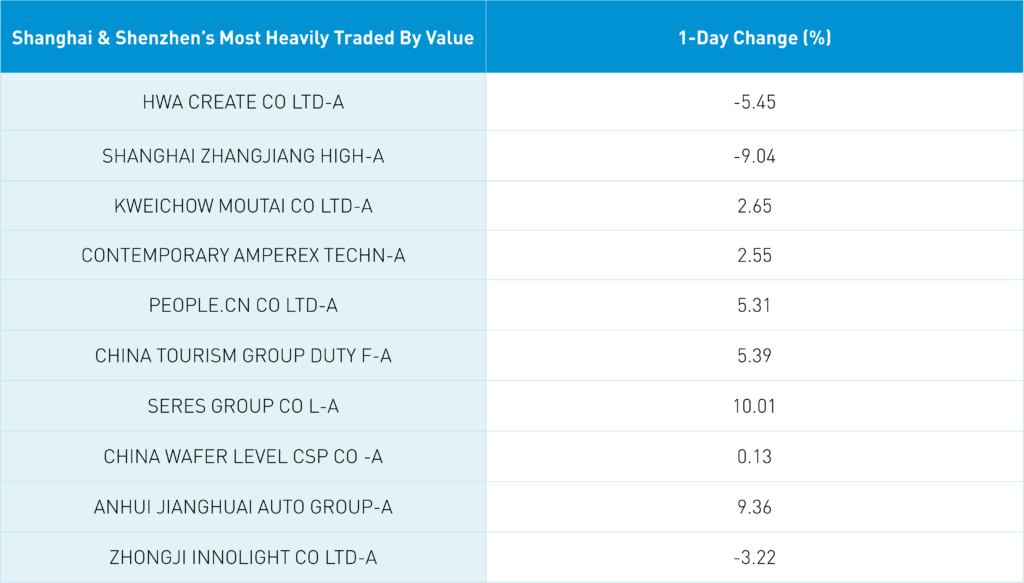

Kweichow Moutai gained +2.64% to become the largest holding in MSCI China A indices, following its recent Moutai-infused coffee collaboration. The premium baijiu liquor company also rolled out a Moutai-infused chocolate bar in partnership with Dove Chocolate. It is somewhat ironic that foreign investors have been net sellers of Kweichow Moutai over the past month.

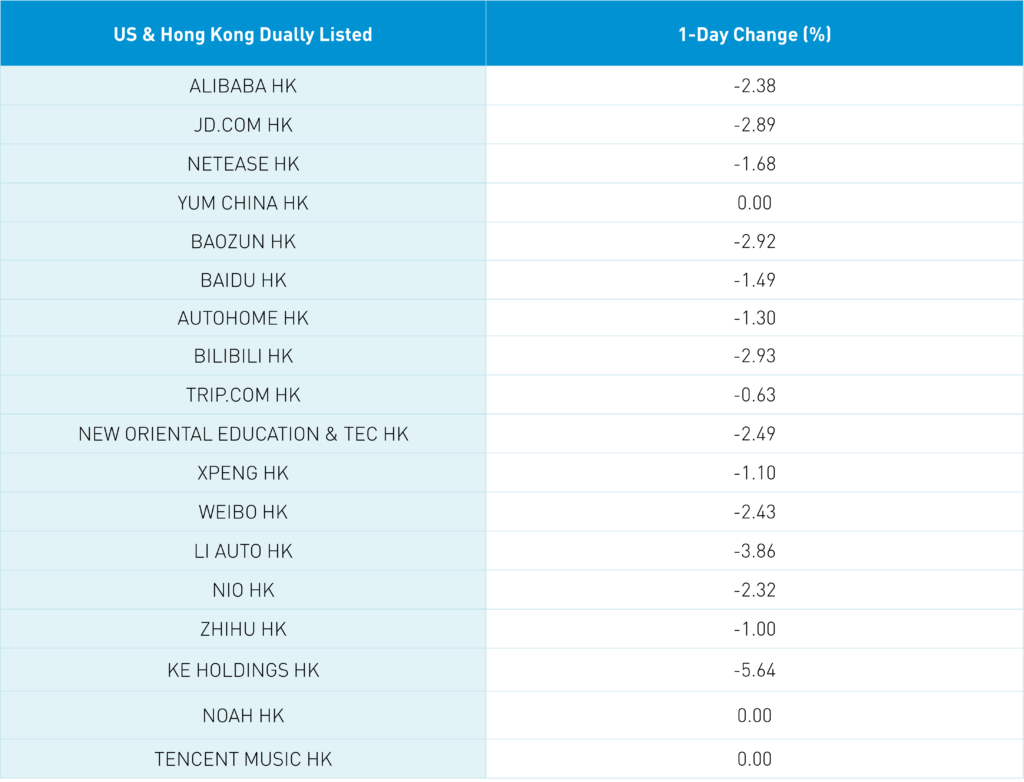

Hong Kong-listed internet stocks were off despite Tencent’s continued stock buyback. Alibaba was off in Hong Kong despite growing their Turkey business and Ant Group taking a stake in South Korean mobile payment provider Toss Payments.

Mainland investors bought a healthy $1.13 billion worth of Hong Kong stocks. The HK Tracker ETF saw a very strong net inflow as somebody is buying the offshore dip.

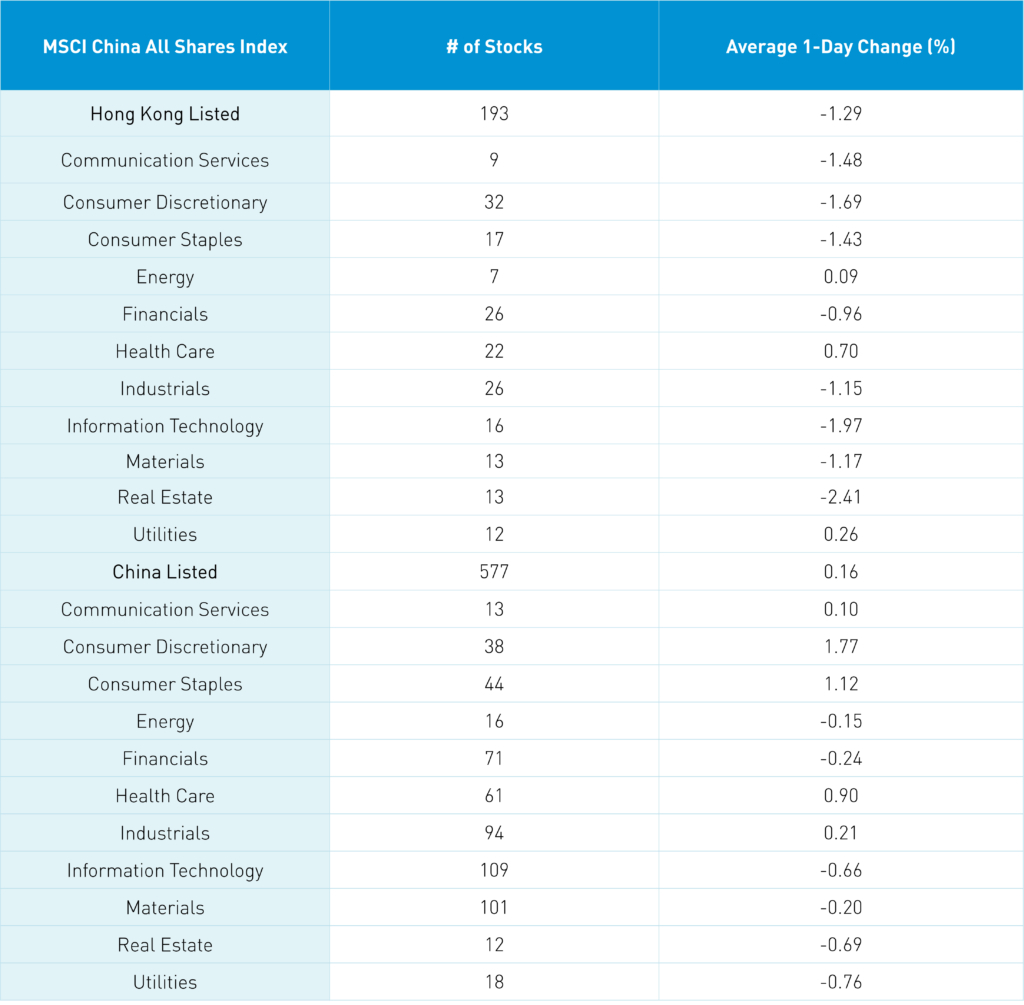

It is remarkable to me how little is written about the MSCI All Country World ex-US’ return of only +228% and the MSCI Emerging Market’s return of +204% since the Global Financial Crisis (GFC) low (all returns in US dollars). Sector weights, and, more to the point, the lack of growth sectors and overweight of value sectors, has created a large disparity between the US market and non-US markets. For instance, the Euro Stoxx 50 Index has returned only +249% since the GFC low. But, do we read about Europe being un-investable? Not really. Maybe the issue is the benchmark, which has only four tech stocks and only one communication stock! As we’ve written in the past, both MSCI Emerging Markets and MSCI China had only 11% and 2%, respectively, in the tech sector ten years ago. Energy and financials accounted for more than 50% of the indices, which weighed on the performance. Bad sector composition could be the root of all evil!

The Hang Seng and Hang Seng Tech indexes fell -1.39% and -2.22%, respectively, on volume that decreased -28.43% from Friday, which is 73.9% of the 1-year average. 157 stocks advanced while 319 declined. Main Board short turnover increased +8.38% from Friday, which is 103% of the 1-year average, as 23% of turnover was short turnover. The growth factor “outperformed” (ie. fell less than) the value factor as large caps outpaced small caps. The top-performing sectors were healthcare, which gained +0.7%, utilities, which gained +0.27%, and energy, which gained +0.10%. Meanwhile, Real Estate fell -2.4%, technology fell -1.97%, and consumer discretionary fell -1.68%. Top sub-sectors were healthcare equipment, pharma and business services while semis, food and retailing were the worst. Southbound Stock Connect volumes were moderate as mainland investors buying $1.113B of HK listed ETFs and stocks with the HK Tracker ETF seeing a very large net buy, China Mobile, Innovent and SMIC small net buys.

Shanghai, Shenzhen and STAR Board closed +0.26%, +0.54% and -0.84% on volume -3.04% from Friday which is 80% of the 1-year average. 3,233 stocks advanced while 1,458 declined. The growth factor outperformed the value factor as small caps outpaced large caps. The top-performing sectors were Consumer Discretionary, which gained +1.77%, Consumer Staples, which gained +1.12%, and Healthcare, which gained +0.91%. Meanwhile, Utilities fell -0.75%, Real Estate fell -0.68%, and Technology fell -0.66%. The top-performing subsectors were restaurants, auto parts, and the auto industry. Meanwhile, telecom, trade industry, and energy equipment were among the worst-performing. Northbound Stock Connect volumes were moderate/light as foreign investors bought a net $387 million worth of Mainland stocks as CTG Duty Free, BYD, and Kweichow Moutai were all small/moderate net buys, while CATL, Wuxi AppTec, and Citic were small net sells. CNY and the Asia dollar index fell versus the US dollar. Treasury bonds sold off.

Last Night’s Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.30 versus 7.28 Friday

- CNY per EUR 7.78 versus 7.76 Friday

- Yield on 1-Day Government Bond 1.60% versus 1.45% Friday

- Yield on 10-Year Government Bond 2.65% versus 2.64% Friday

- Yield on 10-Year China Development Bank Bond 2.76% versus 2.76% Friday

- Copper Price -0.42%

- Steel Price +0.10%

—

Originally Posted September 18, 2023 – Mainland Markets Rise As Hong Kong Shorts Press Their Bets

Author Positions as of 9/18/23 are KLIP, KBA, KALL, KCNY, KFYP, KCNY, KEMQ, BZUN, HSBC, KWEB, KHYB, LI US

Charts Source: KraneShares

Disclosure: KraneShares

Content on China Last Night is for informational purposes only and should not be construed as investment advice. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results; material is as of the dates noted and is subject to change without notice. This information should not be relied upon by the reader as research or investment advice regarding the funds or any security in particular.

This material may not be suitable for all investors and is not intended to be an offer, or the solicitation of any offer, to buy or sell any securities. Investing involves risk, including possible loss of principal.

This material contains general information only and does not take into account an individual’s financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial advisor before making an investment decision.

Forward-looking statements (including Krane’s opinions, expectations, beliefs, plans, objectives, assumptions, or projections regarding future events or future results) contained in this presentation are based on a variety of estimates and assumptions by Krane. These statements generally are identified by words such as “believes,” “expects,” “predicts,” “intends,” “projects,” “plans,” “estimates,” “aims,” “foresees,” “anticipates,” “targets,” “should,” “likely,” and similar expressions. These also include statements about the future, including what “will” happen, which reflect Krane’s current beliefs. These estimates and assumptions are inherently uncertain and are subject to numerous business, industry, market, regulatory, geo-political, competitive, and financial risks that are outside of Krane’s control. The inclusion of forward-looking statements herein should not be regarded as an indication that Krane considers forward-looking statements to be a reliable prediction of future events and forward-looking statements should not be relied upon as such. Neither Krane nor any of its representatives has made or makes any representation to any person regarding forward-looking statements and neither of them intends to update or otherwise revise such forward-looking statements to reflect circumstances existing after the date when made or to reflect the occurrence of future events, even in the event that any or all of the assumptions underlying such forward-looking statements are later shown to be in error. Any investment strategies discussed herein are as of the date of the writing of this presentation and may be changed, modified, or exited at any time without notice.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from KraneShares and is being posted with its permission. The views expressed in this material are solely those of the author and/or KraneShares and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Forex

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

")

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.