")

For better or worse, since publishing “Meme Stocks: The Sequel”, I’ve spent a copious amount of time discussing the various nuances of the last round of meme-stock mania. While the recent Reddit (RDDT) IPO was a popular topic, thanks to its overlap between politics and business, Trump Media & Technology Group (DJT) attracted the bulk of the questions.

A popular question involves the viability of using puts to express a negative view on a stock as a way to avoid incurring the high cost of borrowing shares. As with many options-related questions there is a short answer that requires a detailed explanation. Bottom line, the puts on a hard-to-borrow (HTB) underlying shares implicitly reflect those costs. Here’s why:

Political considerations aside, any fast-moving, highly valued stock with minimal revenues and profits relative to its market capitalization will attract attention from short sellers. That’s a consistent feature of markets, not a referendum on a specific stock or its owners.

As with any market price, the cost to borrow a stock reflects the relative balance of supply and demand. The vast majority of stocks have a plentiful supply of borrowable shares relative to the demand for shorting them. Those are called “general collateral”, meaning that they can be borrowed and lent at rates roughly approximating the prevailing Fed Funds rate. When the demand begins to outpace the supply, the cost to borrow the shares increases, sometimes precipitously.

Stock loan rates for HTB shares are typically expressed as negative numbers. Normally when one lends shares, they borrow money in return. As noted above, in the case of general collateral, that is approximately the prevailing Fed Funds rates. But when demand outstrips supply, the borrower instead pays a fee to the lender. Since that is the inverse of the typical relationship, the interest rates are expressed as negative numbers.

As with many things, DJT represents an extreme case. Passions are high on both sides of the trade, with fervent admirers bidding up the shares to levels that attract sellers who believe the valuation is outlandish. That alone would create negative rates, but in this case, insiders own the majority of the shares, meaning they are not available to borrow. Last week, as the newly de-SPAC’d company experienced a meteoric rise, borrow rates jumped to an annualized -150%. During yesterday’s 20% plunge, those rates spiked to over -800%. (A recent check showed rates around -700% today.). No matter which rate, shorting is then very expensive.

Bearing in mind that the maximum profit on a short sale is 100% – the stock can’t fall below zero – it is much more helpful to consider how those annualized rates translate into daily rates. Yesterday, when the cost to borrow was -800%, that implied a daily rate of about 2.2%. With DJT stock around $50, that meant that it cost borrowers about $1.10 per day to maintain their short positions. It also meant that if one shorted the stock and held the position through the end of the week, the stock would need to fall more than $5 just to cover the costs.

With that in mind, it is obvious that traders would look for a way to avoid that sort of constant cash outlay. Put options, which allow traders to speculate that the price of a stock will fall, require only a fixed cash outlay when the trade is entered. That is obviously appealing – but remember that there is no free lunch. Presumably, whomever sells those puts would want to hedge their short puts by selling stock short. That will cost them money, and price sensitive market makers will account for those costs in the price of the puts.

This is where it is important to remember the put/call parity equation. The equation states:

Call Price + Strike Price = Forward value of Stock Price + Put Price

It is important to use the forward value of the stock, which is adjusted for interest rates and dividends, rather than strictly the current price of the stock. We can calculate the forward value this way:

Forward value = (Current value) x (1 + interest rate * days until expiration/365) – dividends

This is where the negative interest rates on HTB stocks come into play. The forward value of the stock will be meaningfully less than that of the current price. In practice, that means that the “at-money” strike for the puts will be below the price where the stock is currently trading, and the further the expiration, the lower the forward value.

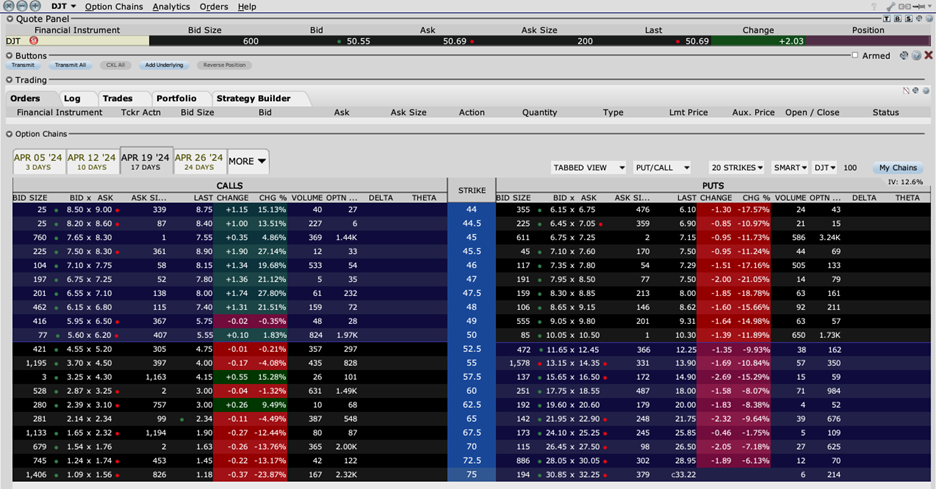

Fortunately, there is a shortcut for figuring out what that implied forward value might be. It’s the strike where the put and call prices are roughly equal. Using the Option Trader function on the classic IBKR TWS, we can see that for options expiring on April 19th, the closest strike is $46, even as the last sale on DJT was $50.69. That is roughly a 10% haircut on options with 17 days until expiration.

We can very roughly impute a borrow rate from that that calculation. In this case, it’s a bit over 200%:

($50.69 – $46) / $46 = 10.2% ; 10.2% * 365/17 = 219%

As noted above, the current borrow rate is about -700%, so -219% seems like a bargain. Maybe, but not definitely. First of all, the calculation was admittedly a very rough one. Secondly, stock loan rates are volatile (they went from -150% to -800% to -700% in three trading days), so the market might believe that -220% is a reasonable expectation for the average rate over the time until expiration. Finally, the implied volatilities are also quite high – around 12.4% daily or 200% annualized. That’s a lot of decay to contend with.

In short, put options can offer a way to speculate against a hard-to-borrow stocks without the daily costs of financing the position. But there is no free lunch, since the borrow costs are implicitly priced in, and because the types of stocks that attract heavy short interest also sport high implied volatilities. Trade accordingly.

Source: Interactive Brokers

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. Multiple leg strategies, including spreads, will incur multiple commission charges. For more information read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD) or visit ibkr.com/occ

Disclosure: Options (with multiple legs)

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by clicking the link below. Multiple leg strategies, including spreads, will incur multiple transaction costs. "Characteristics and Risks of Standardized Options"

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.