")

The recent earnings announcement from Nvidia was, well, historic. It’s not often that any firm shifts revenue guidance for an upcoming quarter from something around $7 billion to something around $11 billion. Nvidia’s total market capitalization touched the vaunted $1-trillion level, something very few companies ever achieve.1

Did You Miss It?

Professor Aswath Damodaran of New York University,2 well known for his work on valuation, put forward a case as to why, even though he appreciates Nvidia as a company, he cannot rationalize a $1-trillion valuation.

Professor Damodaran estimates Nvidia has a roughly 80% share of the AI semiconductor market, which is worth around $25 billion today. Using bullish assumptions, which may not prove accurate, he expects to see growth in the AI semiconductor market reach $350 billion within a decade. If Nvidia captured 100% of future market share—a bold assumption—Damodaran’s valuation is still about 20% below current prices.

Nvidia is essentially a hardware company. One can see them try to ramp up software, but that is not their main driver. Other companies that have achieved the $1 trillion market capitalization level have software companies with network effects drawing vast numbers of end users into ecosystems. These software businesses have many ways to earn revenue from new products and services.

Professor Damodaran’s valuations do not necessarily lead to immediate declines in share prices—but it may be difficult to keep the return momentum going with the same fervor.

Nvidia’s Products Do Not Operate in a Vacuum

WisdomTree spends a lot of time focusing on the AI megatrend. Nvidia’s products do not exist in a ‘standalone’ fashion, as they are plugged into cabinets containing other hardware functioning in concert. If the AI semiconductor market grows as many now expect, a lot of companies will benefit.

Nvidia cannot, by itself, manufacture its semiconductors end-to-end. Taiwan Semiconductor Manufacturing Co. (TSMC) is responsible for this part of the puzzle. There is a whole semiconductor value chain—all necessary—and each link is capturing a different-sized slice of the pie of economic value.

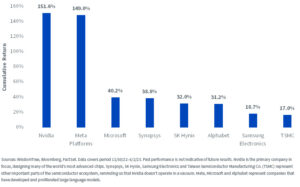

In figure 1, we show a range of companies associated with generative AI over the period since the release of ChatGPT.

- Alphabet, Meta and Microsoft represent companies developing large language models (LLMs) to allow users to directly access generative AI. Meta was beaten down in 2022, due to disappointment with the firm’s metaverse efforts, but AI and cost cutting is helping the company in 2023. Alphabet and Microsoft are in the center of the generative AI battleground. Microsoft, so far, is winning on the cloud computing battle front with its Azure platform, whereas Alphabet’s Google is going to be very difficult to defeat in the internet search space.

- It’s interesting to compare Nvidia to Samsung and SK Hynix. Running AI models, especially large AI models, requires memory, and Samsung and SK Hynix are in the memory chip space. Excitement, at least in recent years, fluctuated in the broad semiconductor market. Right now, during the explosion of generative AI, graphics processing units (GPUs), where Nvidia is the leader, are all the rage.

- Synopsys and TSMC represent notable and necessary value-chain plays on semiconductors. Nvidia chips cannot be created in a vacuum. Synopsys provides necessary electronic design automation capabilities, whereas TSMC is among the few companies with a manufacturing process advanced enough to fabricate Nvidia’s most advanced chips.

Figure 1: Returns across the AI Ecosystem Have Varied since ChatGPT’s Release

AI Covers Many Different Things—and those Things Have Been Exciting at Different Times

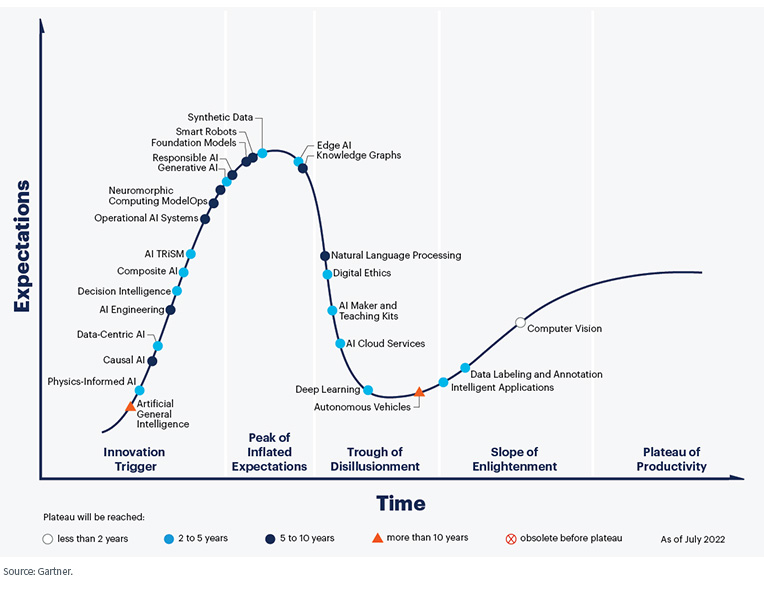

Is AI over-hyped? The Gartner hype cycle characterizes one way to view new technologies. In the short term, excitement leads to money flows. Share prices and valuations benefit. At a certain point, a realization sets in that true success, growth and adoption take time, so at this point there is usually a lot of selling and a tougher return environment.

Finally, there is recognition that pessimism is also not quite appropriate as the technology is still important and still being used, so growth rates and returns tend to become more reasonable.

We reference a plot of the hype cycle for AI in figure 2.

AI is not any one single thing. Today we think of it as ChatGPT, LLMs or generative AI, but other disciplines and functionalities are still there—they just aren’t grabbing headlines in same way.

- Generative AI and foundation models might be nearing a peak of inflated expectations.

- Have you been excited about self-driving vehicles recently? No? Well, that could be part of the reason why autonomous vehicles may be near the trough of disillusionment.

- Computer vision—which has been around for quite some time—is making its way up the ‘slope of enlightenment.’

The hype cycle is not an exact science. Any discipline on this graph could generate any sort of return, positive or negative, going forward. It’s really just a tool that helps us place all these different topics on a broader continuum. The only thing we seem to know for sure is that none of the topics generate the same level of excitement or pessimism all the time.

Figure 2: Hype Cycle for Artificial Intelligence, 2022

Conclusion: It’s Possible to Mitigate Single Company Risk by Looking across the AI Ecosystem

The hype cycle illustration points out the various applications of AI are at different points of adoption, excitement and development. No one knows the future with certainty, but we believe there is growth occurring in all these disciplines. The world is enthralled with generative AI now, but the world was similarly excited about autonomous vehicles a few years ago. Progress is occurring even if we are not seeing it reflected in every headline.

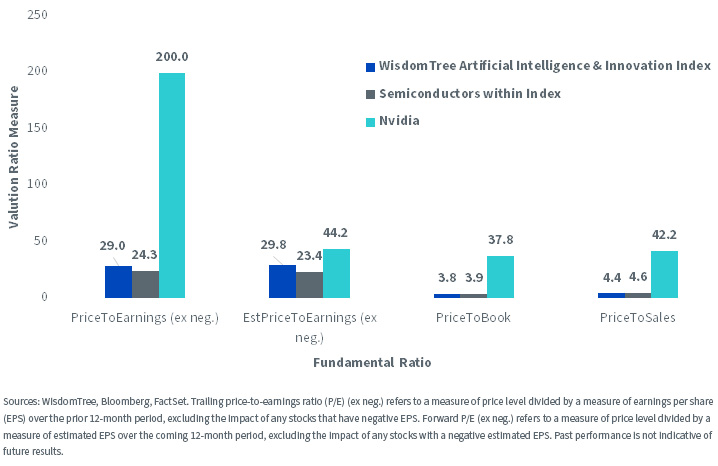

WisdomTree has a broad-based AI Index to capture these trends. While Nvidia’s valuation is getting stretched, according to Professor Damodaran, WisdomTree’s AI Index did not change much following the Nvidia surge. The entire ecosystem of AI defined by WisdomTree is not as beholden to the moves of any single company.

Figure 3: How a Broad-Based Approach to Artificial Intelligence Companies Is Less Influenced by the High Current Valuation of Nvidia (as of 6/5/23)

AI has the potential to impact every industry. This is why WisdomTree built a broad-based, ecosystem-oriented approach as opposed to concentrating on any single stock.

—

Originally Posted June 13, 2023 – Is the Momentum Running Out of AI-Focused Stocks?

Important Disclosures and Risks Related to this Article

Click here for a full list of Fund holdings. Holdings are subject to change.

The WisdomTree Artificial Intelligence & Innovation Index is designed to measure the performance of companies primarily involved in artificial intelligence and innovation.

There are risks associated with investing, including the possible loss of principal. The Fund invests in companies primarily involved in the investment theme of artificial intelligence (AI) and innovation. Companies engaged in AI typically face intense competition and potentially rapid product obsolescence. These companies are also heavily dependent on intellectual property rights and may be adversely affected by loss or impairment of those rights. Additionally, AI companies typically invest significant amounts of spending on research and development, and there is no guarantee that the products or services produced by these companies will be successful. Companies that are capitalizing on innovation and developing technologies to displace older technologies or create new markets may not be successful. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is governed by an Index Committee and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Disclosure: WisdomTree U.S.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Funds before investing. U.S. investors only: To obtain a prospectus containing this and other important information, please call 866.909.WISE (9473) or click here to view or download a prospectus online. Read the prospectus carefully before you invest. There are risks involved with investing, including the possible loss of principal. Past performance does not guarantee future results.

You cannot invest directly in an index.

Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, real estate, currency, fixed income and alternative investments include additional risks. Due to the investment strategy of certain Funds, they may make higher capital gain distributions than other ETFs. Please see prospectus for discussion of risks.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

Interactive Advisors offers two portfolios powered by WisdomTree: the WisdomTree Aggressive and WisdomTree Moderately Aggressive with Alts portfolios.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree U.S. and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree U.S. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.